I thought lean production was supposed to make us more efficient commented Ben Carrick, manufacturing vice president

Question:

“I thought lean production was supposed to make us more efficient” commented Ben Carrick, manufacturing vice president of Vorelli Industries. “But just look at June’s manufacturing variances for Zets. The labor efficiency variance was $240,000 unfavorable—four times higher than it’s ever been before. If you add on the $102,000 unfavorable materials price variance, that’s $342,000 down the drain in a single month on just one product.”

“Now take it easy, Ben,” replied Sandi Shipp, the company’s purchasing manager. “We knew the switch to lean production was going to increase our material costs. But now we’re partnering with top-notch suppliers who deliver raw materials to our plant three times a day. In a few months, we’ll be able to offset most of our higher purchasing costs by vacating three rented warehouses.”

“And I know our labor efficiency variance looks bad,” responded Raul Duvall, the company’s production manager, “but it doesn’t tell the whole story. The just-in-time flow in our production lines has made our plant more efficient than ever before. Plus our investment in automation is reducing our materials waste each month.”

“How can you say you’re being more efficient when you took 90,000 direct labor-hours to produce just 30,000 Zets last month?” asked Ben Carrick. “That’s an average of 3 hours per unit, whereas the Zets’ standard cost card only allows 2.5 hours per unit.”

Raul explained that “part of our lean transformation requires cutting back production to reduce excess finished goods inventories. In a few months our finished goods inventories will be depleted and we’ll be able to match production with demand. In the meantime, don’t forget that our line people aren’t just standing around when their machines are idle. Under the lean approach, they’re doing their own inspections and equipment maintenance.”

Ben replied, “We can’t let this go on a few more months . . . at least not if you want to earn a bonus this year. I’ve been looking at these reports for 30 years, and I know inefficiency when I see it. Let’s get things back under control.”

After leaving Ben’s office, Raul asked for your help in developing some performance measures that will highlight the benefits of the company’s lean transformation. Working with Raul, you gathered the following information:

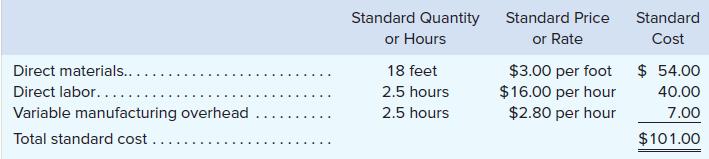

a. A standard cost card for Zets (one of the company’s many products) is given below:

b. During June the company purchased 510,000 feet of material for production of Zets at a cost of $3.20 per foot. All of this material was used to make 30,000 units during the month.

c. The company maintains a stable workforce to produce Zets. Employees who previously performed inspections and maintenance have been reassigned as direct labor workers. During June, direct laborers worked 90,000 hours on the Zets production lines at an average pay rate of $15.85 per hour.

d. Variable manufacturing overhead cost is allocated to products based on direct labor-hours. During June, the company incurred $207,000 in variable manufacturing overhead costs associated with the manufacture of Zets.

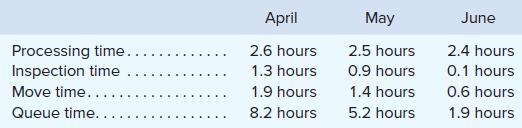

e. As workers have become more familiar with lean production methods, the following trends (per unit) have emerged over the last three months:

Required:

1. For direct materials:

a. Compute the price and quantity variances.

b. Is the decrease in waste that was mentioned by Raul apparent from your variance calculations? Explain.

c. What standard price per foot should the company use going forward to compute the materials price variance? Why?

2. For direct labor:

a. Compute the rate and efficiency variances.

b. Is the company’s labor efficiency variance a useful performance measure in its lean environment? Why?

3. For variable manufacturing overhead:

a. Compute the rate and efficiency variances.

b. Is direct labor-hours an appropriate cost driver for variable manufacturing overhead in the company’s lean environment? Explain.

4. Compute the following for April, May, and June:

a. The throughput time per unit.

b. The manufacturing cycle efficiency (MCE).

5. Which performance measures do you think are more appropriate in the company’s lean environment—the labor efficiency variance or throughput time per unit and manufacturing cycle efficiency?

Step by Step Answer:

1 a 2 30000 units 18 feet per unit 540000 feet Alternative Solution Materials price variance AQ AP SP 510000 feet 320 per foot 300 per foot 102000 U Materials quantity variance SP AQ SQ 3 per foot 510...View the full answer

Managerial Accounting

ISBN: 9781260247787

17th Edition

Authors: Ray Garrison, Eric Noreen, Peter Brewer