1. Tell me about the company's current weighted average cost of capital (WACC). Isn't it obvious...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

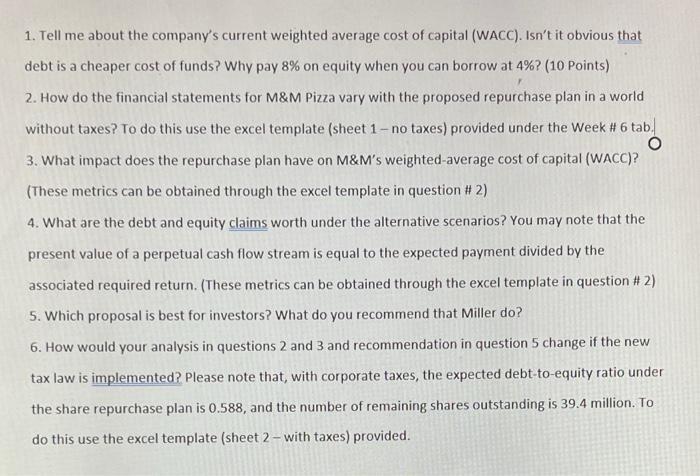

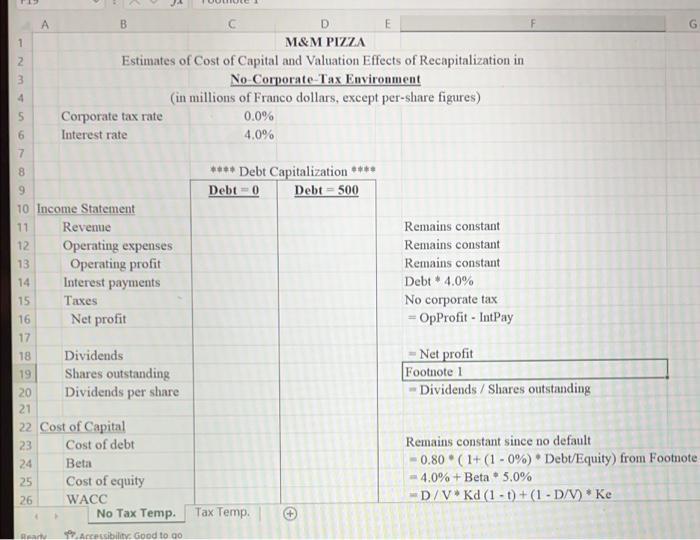

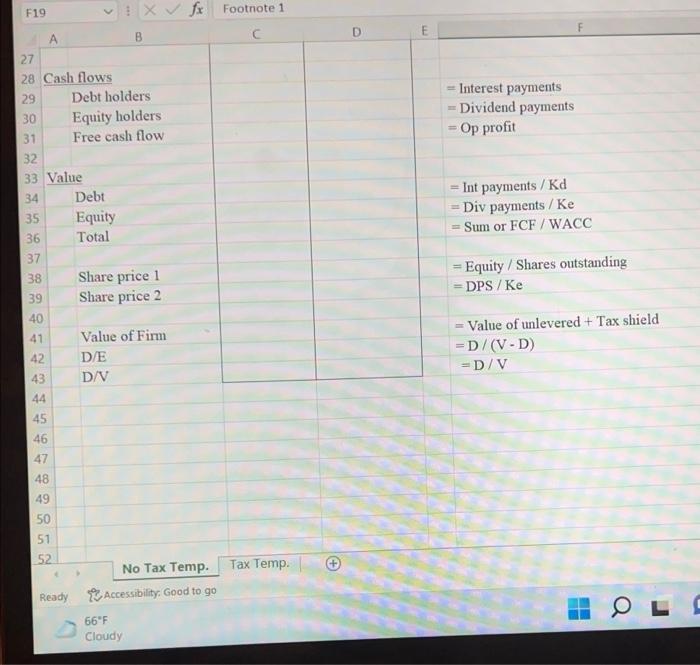

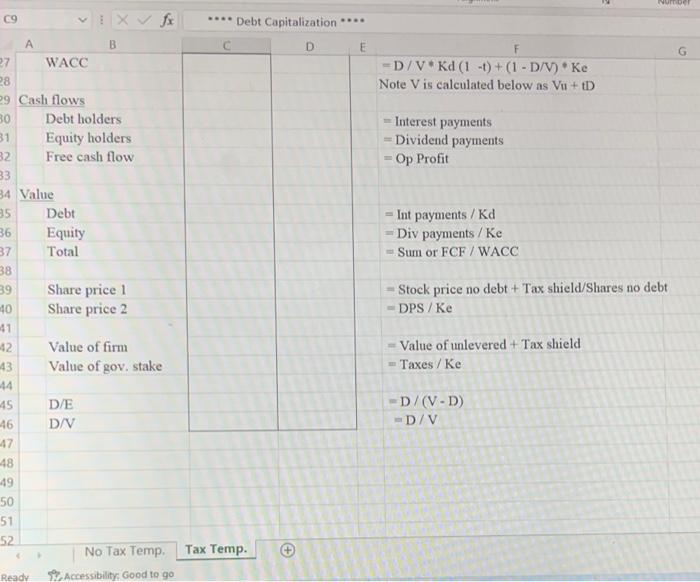

1. Tell me about the company's current weighted average cost of capital (WACC). Isn't it obvious that debt is a cheaper cost of funds? Why pay 8% on equity when you can borrow at 4% ? (10 Points) 2. How do the financial statements for M&M Pizza vary with the proposed repurchase plan in a world without taxes? To do this use the excel template (sheet 1-no taxes) provided under the Week # 6 tab. 3. What impact does the repurchase plan have on M&M's weighted-average cost of capital (WACC)? (These metrics can be obtained through the excel template in question # 2) 4. What are the debt and equity claims worth under the alternative scenarios? You may note that the present value of a perpetual cash flow stream is equal to the expected payment divided by the associated required return. (These metrics can be obtained through the excel template in question # 2) 5. Which proposal is best for investors? What do you recommend that Miller do? 6. How would your analysis in questions 2 and 3 and recommendation in question 5 change if the new tax law is implemented? Please note that, with corporate taxes, the expected debt-to-equity ratio under the share repurchase plan is 0.588, and the number of remaining shares outstanding is 39.4 million. To do this use the excel template (sheet 2 - with taxes) provided. 1 2 3 4 5 6 7 8 A 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 B 9 10 Income Statement Ready Corporate tax rate Interest rate M&M PIZZA Estimates of Cost of Capital and Valuation Effects of Recapitalization in No-Corporate-Tax Environment (in millions of Franco dollars, except per-share figures) Revenue Operating expenses Operating profit Interest payments Taxes Net profit Dividends Shares outstanding Dividends per share Cost of Capital Cost of debt Beta Cost of equity WACC C Accessibility: Good to go 0.0% 4.0% **** Debt Capitalization **** Debt-0 Debt-500 No Tax Temp. Tax Temp. E + Remains constant Remains constant Remains constant Debt * 4.0% No corporate tax = OpProfit - IntPay -Net profit Footnote 1 Dividends / Shares outstanding G Remains constant since no default 0.80 (1+ (1 - 0 %) * Debt/Equity) from Footnote -4.0%+ Beta 5.0% D/V* Kd (1 t) + (1 - D/V) * Ke F19 27 28 Cash flows 29 30 31 34 35 36 37 A 32 33 Value 38 39 40 41 42 43 44 45 46 47 48 49 552 50 51 52 Ready Debt holders Equity holders Free cash flow Debt Equity Total X✓ fx B Share price 1 Share price 2 Value of Firm D/E D/V 66°F Cloudy No Tax Temp. Tax Temp. Accessibility: Good to go Footnote 1 C O E - Interest payments - Dividend payments Op profit H = Int payments/Kd Div payments / Ke Sum or FCF/WACC = Equity / Shares outstanding - DPS / Ke - Value of unlevered + Tax shield = D/(V-D) = D/V OLO C9 8 9 10 14 15 16 17 A 11 Income Statement 12 13 225 26 B Ready M&M PIZZA Estimates of Cost of Capital and Valuation Effects of Recapitalization in Corporate tax rate Interest rate 18 19 20 21 22 23 Cost of Capital 24 Cost of debt fx **** Debt Capitalization **** E (in millions Revenue Operating expenses Operating profit Interest payments Taxes Net profit Dividends Shares outstanding Dividends per share Beta Cost of equity No Tax Temp. Accessibility: Good to go Corporate Tax Environment of Franco dollars, except per-share figures) 20.0% 4.0% **** Debt Capitalization **** Debt-500 Debt 0 Tax Temp. Q Remains constant Remains constant Remains constant Debt 4.0% -20% (OpProf - IntPay) OpProfit - IntPay - Taxes -Net Profit Via Case - Dividends/Shares outstanding Remains constant since no default -0.80 (1+(1-20%) * Debt/Equity) from Footnote 2 4.0%+Beta 5.0% 9 G C9 39 40 41 27 28 29 Cash flows 30 31 32 33 34 Value 35 36 37 38 42 43 44 45 46 -48 49 50 A 51 52 WACC Ready Debt holders Equity holders. Free cash flow Debt Equity Total B Share price 1 Share price 2 D/E D/V fx Value of firm Value of gov. stake No Tax Temp. Accessibility: Good to go **** Debt Capitalization**** C D Tax Temp. E F -D/V Kd (1 t) + (1 - D/V) * Ke Note V is calculated below as Vu+tD M Interest payments Dividend payments Op Profit Int payments/Kd - Div payments / Ke -Sum or FCF/ WACC - Stock price no debt + Tax shield/Shares no debt - DPS / Ke Value of unlevered + Tax shield Taxes / Ke Number -D/(V-D) -D/V G 1. Tell me about the company's current weighted average cost of capital (WACC). Isn't it obvious that debt is a cheaper cost of funds? Why pay 8% on equity when you can borrow at 4% ? (10 Points) 2. How do the financial statements for M&M Pizza vary with the proposed repurchase plan in a world without taxes? To do this use the excel template (sheet 1-no taxes) provided under the Week # 6 tab. 3. What impact does the repurchase plan have on M&M's weighted-average cost of capital (WACC)? (These metrics can be obtained through the excel template in question # 2) 4. What are the debt and equity claims worth under the alternative scenarios? You may note that the present value of a perpetual cash flow stream is equal to the expected payment divided by the associated required return. (These metrics can be obtained through the excel template in question # 2) 5. Which proposal is best for investors? What do you recommend that Miller do? 6. How would your analysis in questions 2 and 3 and recommendation in question 5 change if the new tax law is implemented? Please note that, with corporate taxes, the expected debt-to-equity ratio under the share repurchase plan is 0.588, and the number of remaining shares outstanding is 39.4 million. To do this use the excel template (sheet 2 - with taxes) provided. 1 2 3 4 5 6 7 8 A 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 B 9 10 Income Statement Ready Corporate tax rate Interest rate M&M PIZZA Estimates of Cost of Capital and Valuation Effects of Recapitalization in No-Corporate-Tax Environment (in millions of Franco dollars, except per-share figures) Revenue Operating expenses Operating profit Interest payments Taxes Net profit Dividends Shares outstanding Dividends per share Cost of Capital Cost of debt Beta Cost of equity WACC C Accessibility: Good to go 0.0% 4.0% **** Debt Capitalization **** Debt-0 Debt-500 No Tax Temp. Tax Temp. E + Remains constant Remains constant Remains constant Debt * 4.0% No corporate tax = OpProfit - IntPay -Net profit Footnote 1 Dividends / Shares outstanding G Remains constant since no default 0.80 (1+ (1 - 0 %) * Debt/Equity) from Footnote -4.0%+ Beta 5.0% D/V* Kd (1 t) + (1 - D/V) * Ke F19 27 28 Cash flows 29 30 31 34 35 36 37 A 32 33 Value 38 39 40 41 42 43 44 45 46 47 48 49 552 50 51 52 Ready Debt holders Equity holders Free cash flow Debt Equity Total X✓ fx B Share price 1 Share price 2 Value of Firm D/E D/V 66°F Cloudy No Tax Temp. Tax Temp. Accessibility: Good to go Footnote 1 C O E - Interest payments - Dividend payments Op profit H = Int payments/Kd Div payments / Ke Sum or FCF/WACC = Equity / Shares outstanding - DPS / Ke - Value of unlevered + Tax shield = D/(V-D) = D/V OLO C9 8 9 10 14 15 16 17 A 11 Income Statement 12 13 225 26 B Ready M&M PIZZA Estimates of Cost of Capital and Valuation Effects of Recapitalization in Corporate tax rate Interest rate 18 19 20 21 22 23 Cost of Capital 24 Cost of debt fx **** Debt Capitalization **** E (in millions Revenue Operating expenses Operating profit Interest payments Taxes Net profit Dividends Shares outstanding Dividends per share Beta Cost of equity No Tax Temp. Accessibility: Good to go Corporate Tax Environment of Franco dollars, except per-share figures) 20.0% 4.0% **** Debt Capitalization **** Debt-500 Debt 0 Tax Temp. Q Remains constant Remains constant Remains constant Debt 4.0% -20% (OpProf - IntPay) OpProfit - IntPay - Taxes -Net Profit Via Case - Dividends/Shares outstanding Remains constant since no default -0.80 (1+(1-20%) * Debt/Equity) from Footnote 2 4.0%+Beta 5.0% 9 G C9 39 40 41 27 28 29 Cash flows 30 31 32 33 34 Value 35 36 37 38 42 43 44 45 46 -48 49 50 A 51 52 WACC Ready Debt holders Equity holders. Free cash flow Debt Equity Total B Share price 1 Share price 2 D/E D/V fx Value of firm Value of gov. stake No Tax Temp. Accessibility: Good to go **** Debt Capitalization**** C D Tax Temp. E F -D/V Kd (1 t) + (1 - D/V) * Ke Note V is calculated below as Vu+tD M Interest payments Dividend payments Op Profit Int payments/Kd - Div payments / Ke -Sum or FCF/ WACC - Stock price no debt + Tax shield/Shares no debt - DPS / Ke Value of unlevered + Tax shield Taxes / Ke Number -D/(V-D) -D/V G

Expert Answer:

Related Book For

Statistics Principles And Methods

ISBN: 978-1119497110

8th Edition

Authors: Richard A. Johnson, Gouri K. Bhattacharyya

Posted Date:

Students also viewed these finance questions

-

Use 10% as the company's weighted average cost of capital and the estimates shown below to calculate the following values for a manufacturing plant: 1. The yearly present values 2. The cumulative net...

-

Why does the weighted average cost of capital affect investment capability and risk tolerance?

-

What is meant by the weighted average cost of capital (WACC)?

-

Discuss the ways that managed care organizations can infl uence the adoption of new technologies.

-

Contrast management and financial accounting with respect to the following: Overall purpose Type of financial reports used (i.e., external, internal, or both) Users of the information Also, in...

-

The number of bacteria in a colony increases at a rate proportional to the number present. If the number of bacteria doubles in 10 hours, how long will it take for the colony to triple in size?

-

You invest $1,000 at the beginning of the year. How much will be accumulated in five years if you earn 10% interest compounded annually?

-

The information that follows is from Matts Hardware Companys April 30, 2014, post-closing trial balance. Required 1. Prepare a classified balance sheet for Matts Hardware. 2. Compute Matts Hardwares...

-

Required information [ The following information applies to the questions displayed below. ] The following selected transactions occurred for Corner Corporation: Prepare journal entries for each of...

-

Surkis Company acquires equipment at a cost of $42,000 on January 3, 2017. Management estimates the equipment will have a residual value of $6,000 at the end of its four-year useful life. Assume the...

-

Problem 4-13 (Algo) Comprehensive Problem; Second Production Department-Weighted-Average Method [LO4-2, LO4-3, LO4-4, LO4-5] Old Country Links, Incorporated, produces sausages in three production...

-

Known liabilities of uncertain amounts should be a. estimated and accrued when they occur. b. ignored; record them when they are paid. C. reported on the income statement. d. described in the notes...

-

The NFL has known for some time that serious brain damage could be caused by the head trauma that is part of a normal football game. The sudden serious jarring of a football players head in normal...

-

What condition must be met to use the test for homogeneity?

-

How are tests of independence similar to tests for homogeneity?

-

Which interest rate on a bond determines the amount of the semiannual interest payment? a. Market rate b. Effective rate c. Stated rate d. None of the above

-

A fence is to have 3 1/2 wide boards between two posts that are 94 1/4 apart so that the space between each board is the same. Calculate the number of boards and the spacing so that the spacing...

-

Integration is a vital concept when applied in one?s life. Integrating your life means making ideal choices. Perfect choices on the other go in line with quality decisions. Quality decisions lead to...

-

Express the following statements in the notations of the event operations. (a) A occurs and B does not. (b) Neither A nor B occurs. (c) Exactly one of the events A and B occurs.

-

Refer to Exercise 9 .10, where a zoologist collected 20 wild lizards in the southwestern United States. Do these data substantiate a claim that the mean length is greater than 128 mm? Test with a =...

-

A group of eight students want to compare the quality of food at 4 campus area restaurants. The two students randomly assigned to a site, dine on different nights. Each student rates the quality of...

-

compare the interrelationships and conflicts among individuals, groups, and organizations that result in emotions and stress;

-

Prepare budgeted income statement (Learning Objective 2) Representatives of the various departments of Go Sports have assembled the following data. As the business manager, you must prepare the...

-

discuss burnout and ways to avoid it; and

Study smarter with the SolutionInn App