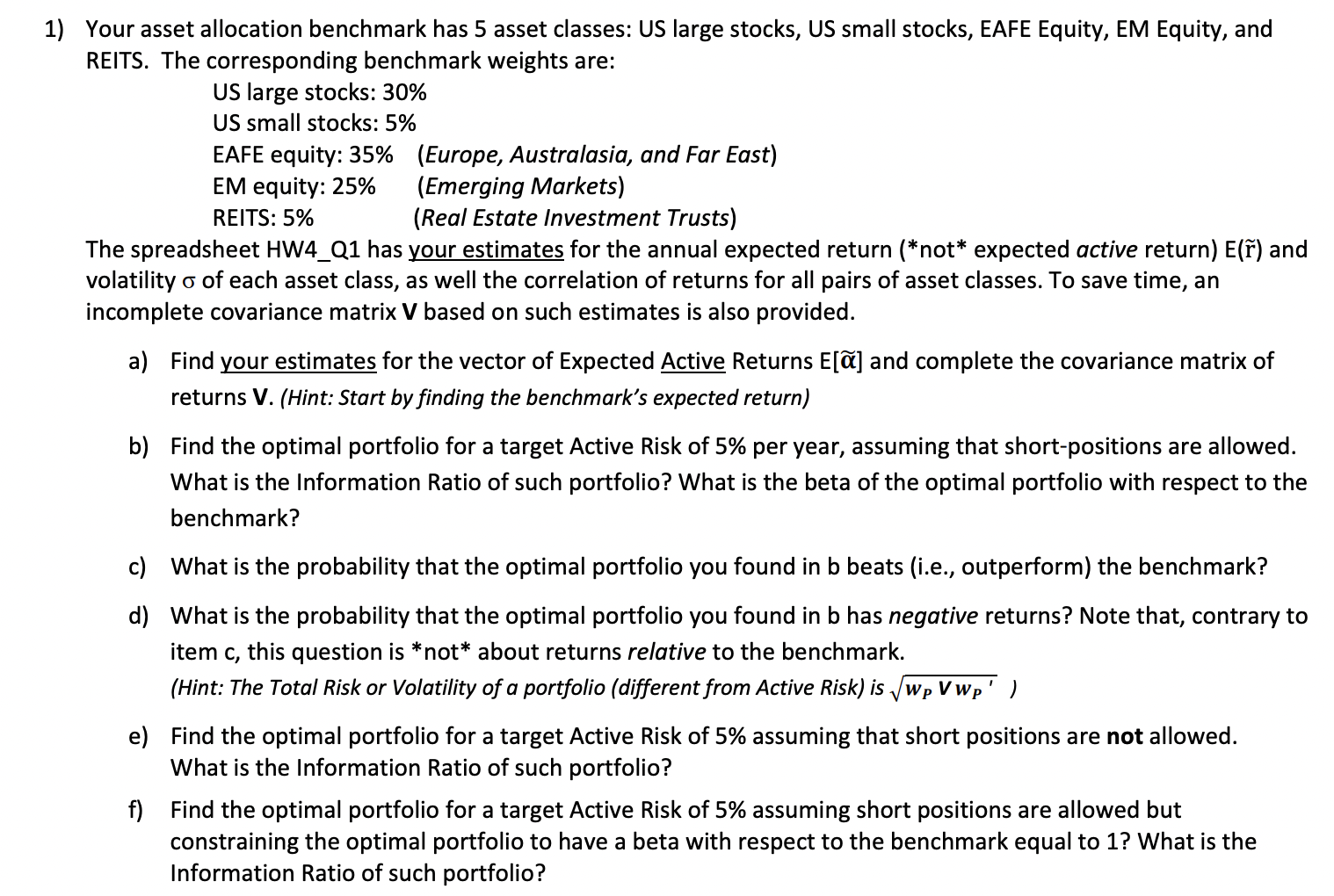

1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

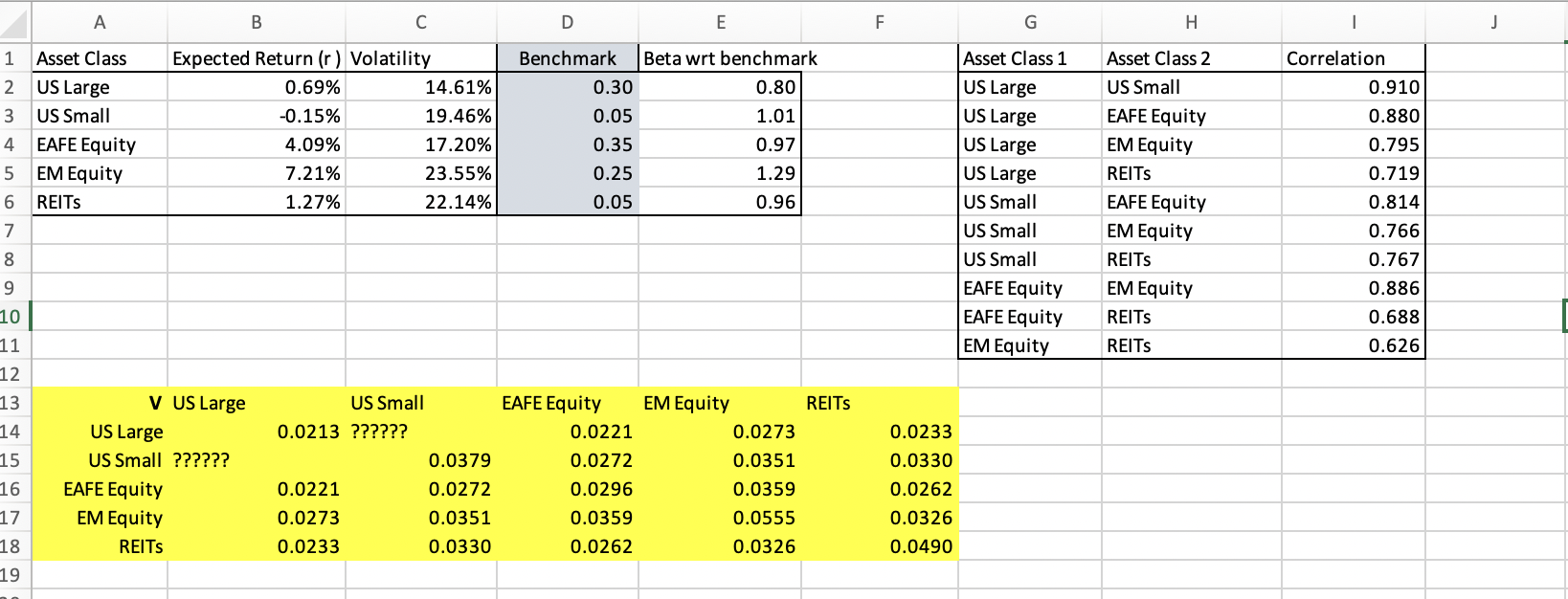

1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE Equity, EM Equity, and REITS. The corresponding benchmark weights are: US large stocks: 30% US small stocks: 5% EAFE equity: 35% EM equity: 25% REITS: 5% (Europe, Australasia, and Far East) (Emerging Markets) (Real Estate Investment Trusts) The spreadsheet HW4_Q1 has your estimates for the annual expected return (*not* expected active return) E(r) and volatility o of each asset class, as well the correlation of returns for all pairs of asset classes. To save time, an incomplete covariance matrix V based on such estimates is also provided. a) Find your estimates for the vector of Expected Active Returns E[a] and complete the covariance matrix of returns V. (Hint: Start by finding the benchmark's expected return) b) Find the optimal portfolio for a target Active Risk of 5% per year, assuming that short-positions are allowed. What is the Information Ratio of such portfolio? What is the beta of the optimal portfolio with respect to the benchmark? c) What is the probability that the optimal portfolio you found in b beats (i.e., outperform) the benchmark? d) What is the probability that the optimal portfolio you found in b has negative returns? Note that, contrary to item c, this question is *not* about returns relative to the benchmark. (Hint: The Total Risk or Volatility of a portfolio (different from Active Risk) is √wp VWp' ) e) Find the optimal portfolio for a target Active Risk of 5% assuming that short positions are not allowed. What is the Information Ratio of such portfolio? f) Find the optimal portfolio for a target Active Risk of 5% assuming short positions are allowed but constraining the optimal portfolio to have a beta with respect to the benchmark equal to 1? What is the Information Ratio of such portfolio? A 1 Asset Class 2 US Large 3 US Small EAFE Equity 4 5 EM Equity 6 REITS 7 8 9 10 11 12 13 14 15 16 17 18 19 V US Large US Large US Small ?????? EAFE Equity EM Equity REITS B Expected Return (r) Volatility 0.69% -0.15% 4.09% 7.21% 1.27% C 0.0213 ?????? 0.0221 0.0273 0.0233 14.61% 19.46% 17.20% 23.55% 22.14% US Small 0.0379 0.0272 0.0351 0.0330 D Benchmark 0.30 0.05 0.35 0.25 0.05 EAFE Equity 0.0221 0.0272 0.0296 0.0359 0.0262 E Beta wrt benchmark 0.80 1.01 0.97 1.29 0.96 EM Equity 0.0273 0.0351 0.0359 0.0555 0.0326 REITS F 0.0233 0.0330 0.0262 0.0326 0.0490 G Asset Class 1 US Large US Large US Large US Large US Small US Small US Small EAFE Equity EAFE Equity EM Equity H Asset Class 2 US Small EAFE Equity EM Equity REITS EAFE Equity EM Equity REITS EM Equity REITS REITS I Correlation 0.910 0.880 0.795 0.719 0.814 0.766 0.767 0.886 0.688 0.626 J 1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE Equity, EM Equity, and REITS. The corresponding benchmark weights are: US large stocks: 30% US small stocks: 5% EAFE equity: 35% EM equity: 25% REITS: 5% (Europe, Australasia, and Far East) (Emerging Markets) (Real Estate Investment Trusts) The spreadsheet HW4_Q1 has your estimates for the annual expected return (*not* expected active return) E(r) and volatility o of each asset class, as well the correlation of returns for all pairs of asset classes. To save time, an incomplete covariance matrix V based on such estimates is also provided. a) Find your estimates for the vector of Expected Active Returns E[a] and complete the covariance matrix of returns V. (Hint: Start by finding the benchmark's expected return) b) Find the optimal portfolio for a target Active Risk of 5% per year, assuming that short-positions are allowed. What is the Information Ratio of such portfolio? What is the beta of the optimal portfolio with respect to the benchmark? c) What is the probability that the optimal portfolio you found in b beats (i.e., outperform) the benchmark? d) What is the probability that the optimal portfolio you found in b has negative returns? Note that, contrary to item c, this question is *not* about returns relative to the benchmark. (Hint: The Total Risk or Volatility of a portfolio (different from Active Risk) is √wp VWp' ) e) Find the optimal portfolio for a target Active Risk of 5% assuming that short positions are not allowed. What is the Information Ratio of such portfolio? f) Find the optimal portfolio for a target Active Risk of 5% assuming short positions are allowed but constraining the optimal portfolio to have a beta with respect to the benchmark equal to 1? What is the Information Ratio of such portfolio? 1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE Equity, EM Equity, and REITS. The corresponding benchmark weights are: US large stocks: 30% US small stocks: 5% EAFE equity: 35% EM equity: 25% REITS: 5% (Europe, Australasia, and Far East) (Emerging Markets) (Real Estate Investment Trusts) The spreadsheet HW4_Q1 has your estimates for the annual expected return (*not* expected active return) E(r) and volatility o of each asset class, as well the correlation of returns for all pairs of asset classes. To save time, an incomplete covariance matrix V based on such estimates is also provided. a) Find your estimates for the vector of Expected Active Returns E[a] and complete the covariance matrix of returns V. (Hint: Start by finding the benchmark's expected return) b) Find the optimal portfolio for a target Active Risk of 5% per year, assuming that short-positions are allowed. What is the Information Ratio of such portfolio? What is the beta of the optimal portfolio with respect to the benchmark? c) What is the probability that the optimal portfolio you found in b beats (i.e., outperform) the benchmark? d) What is the probability that the optimal portfolio you found in b has negative returns? Note that, contrary to item c, this question is *not* about returns relative to the benchmark. (Hint: The Total Risk or Volatility of a portfolio (different from Active Risk) is √wp VWp' ) e) Find the optimal portfolio for a target Active Risk of 5% assuming that short positions are not allowed. What is the Information Ratio of such portfolio? f) Find the optimal portfolio for a target Active Risk of 5% assuming short positions are allowed but constraining the optimal portfolio to have a beta with respect to the benchmark equal to 1? What is the Information Ratio of such portfolio? A 1 Asset Class 2 US Large 3 US Small EAFE Equity 4 5 EM Equity 6 REITS 7 8 9 10 11 12 13 14 15 16 17 18 19 V US Large US Large US Small ?????? EAFE Equity EM Equity REITS B Expected Return (r) Volatility 0.69% -0.15% 4.09% 7.21% 1.27% C 0.0213 ?????? 0.0221 0.0273 0.0233 14.61% 19.46% 17.20% 23.55% 22.14% US Small 0.0379 0.0272 0.0351 0.0330 D Benchmark 0.30 0.05 0.35 0.25 0.05 EAFE Equity 0.0221 0.0272 0.0296 0.0359 0.0262 E Beta wrt benchmark 0.80 1.01 0.97 1.29 0.96 EM Equity 0.0273 0.0351 0.0359 0.0555 0.0326 REITS F 0.0233 0.0330 0.0262 0.0326 0.0490 G Asset Class 1 US Large US Large US Large US Large US Small US Small US Small EAFE Equity EAFE Equity EM Equity H Asset Class 2 US Small EAFE Equity EM Equity REITS EAFE Equity EM Equity REITS EM Equity REITS REITS I Correlation 0.910 0.880 0.795 0.719 0.814 0.766 0.767 0.886 0.688 0.626 J A 1 Asset Class 2 US Large 3 US Small EAFE Equity 4 5 EM Equity 6 REITS 7 8 9 10 11 12 13 14 15 16 17 18 19 V US Large US Large US Small ?????? EAFE Equity EM Equity REITS B Expected Return (r) Volatility 0.69% -0.15% 4.09% 7.21% 1.27% C 0.0213 ?????? 0.0221 0.0273 0.0233 14.61% 19.46% 17.20% 23.55% 22.14% US Small 0.0379 0.0272 0.0351 0.0330 D Benchmark 0.30 0.05 0.35 0.25 0.05 EAFE Equity 0.0221 0.0272 0.0296 0.0359 0.0262 E Beta wrt benchmark 0.80 1.01 0.97 1.29 0.96 EM Equity 0.0273 0.0351 0.0359 0.0555 0.0326 REITS F 0.0233 0.0330 0.0262 0.0326 0.0490 G Asset Class 1 US Large US Large US Large US Large US Small US Small US Small EAFE Equity EAFE Equity EM Equity H Asset Class 2 US Small EAFE Equity EM Equity REITS EAFE Equity EM Equity REITS EM Equity REITS REITS I Correlation 0.910 0.880 0.795 0.719 0.814 0.766 0.767 0.886 0.688 0.626 J

Expert Answer:

Answer rating: 100% (QA)

Here are the steps to solve this multipart question a Benchmark expected return 30 Er US ... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Problem 3. The American Association of Advertising Agencies records data on length of nonprogramming time on half hour prime time television shows. Representative data in minutes for a sample of 20...

-

A. Name the variables used in this analysis and whether they are categorical or continuous. B. State a research question, null hypothesis, and alternate hypothesis for the independent samples t-test....

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

You have recently been hired as a fund manager in the portfolio management team of a bank. Your Director, John Tan has arranged a meeting next week to present an investment proposal to a prospective...

-

Let B, C, and V be bases for a finite-dimensional vector space V. Prove that PDC PCB = PDB

-

At the beginning of 2016, AB Corporation (a calendar-year corporation) owned the following assets: On February 1, 2016, AB sold its office furniture. On March 15, 2016, AB sold its computer...

-

Southwest Airlines Co. is one of the most successful airlines in the United States. Its annual report contains this statement: We are a company of People, not Planes. That is what distinguishes us...

-

The balance sheet of Roop Industries is shown below. The 12/31/2010 value of operations is $651 million, and there are 10 million shares of common equity. What is the intrinsic price per share?...

-

For a given level of profitability as measured by profit margin, the firm's return on equity will: a. Increase as its debt to assets ratio decreases b. Decrease as its current ratio increases c....

-

A receiver for base band digital data has a threshold set at instead of zero. Rederive (9.8), (9.9), and (9.11) taking this into account. If P(+A) = P(-A) = 1/2, find E b / N 0 in decibels as a...

-

6 a) Consider the following dataset representing the values of a variable: [1.2,2.4,2.5,3.1,3.5,4.2,4.8,5.3,5.5,6.1]. Using the histogram method, estimate the probability density function p(x) for a...

-

The prompt reporting of communicable diseases is necessary in order for states to protect citizens health by invoking the power to quarantine.

-

Timely reporting of drug interactions is necessary to help prevent harmful occurrences by those dispensing, prescribing, and taking the medication reported.

-

Match the following terms to their definitions: 1. Tells whether a company can pay all its current liabilities if they become due immediately 2. Measures a company's success in using assets to earn...

-

Senior abuse is less likely to be reported than child abuse, and proving senior abuse charges is often difficult. Types of senior abuse include abandonment, emotional or psychological abuse, physical...

-

In 2010, common stockholders received \($2\) per share in annual dividends. The market price per share for common stock was \($12.\) Compute the dividend yield for common stock.

-

XYZ manufactures a line of high-end exercise equipment of commercial quality. Assume that the chief accountant has proposed changing from a traditional costing system to an activity-based costing...

-

The power company must generate 100 kW in order to supply an industrial load with 94 kW through a transmission line with 0.09 resistance. If the load power factor is 0.83 lagging, find the...

-

What is the advantage of using a relative rather than an absolute scale to construct graphs of security prices?

-

You buy 100 shares in a no-load mutual fund at its net asset value of $10. During the year, the mutual fund distributes $0.75 in dividends. You redeem the shares for their net asset value of $12.03,...

-

What is a beta coefficient? What do beta coefficients of 0.5, 1.0, and 1.5 mean?

-

Outsourcing decision given alternative use of capacity (Learning Objective 6) X-Perience manufactures snowboards. Its cost of making 1,800 bindings is: Suppose OBrien will sell bindings to X-Perience...

-

Sell or process further decisions (Learning Objective 7) Vision Chemical has spent $240,000 to refine 72,000 gallons of acetone, which can be sold for $2.16 a gallon. Alternatively, Vision Chemical...

-

Pricing of facial tissues (Learning Objective 3) Softies produces facial tissues. Softies has $50 million in assets. Its yearly fixed costs are $12 million, and the variable cost of producing and...

Study smarter with the SolutionInn App