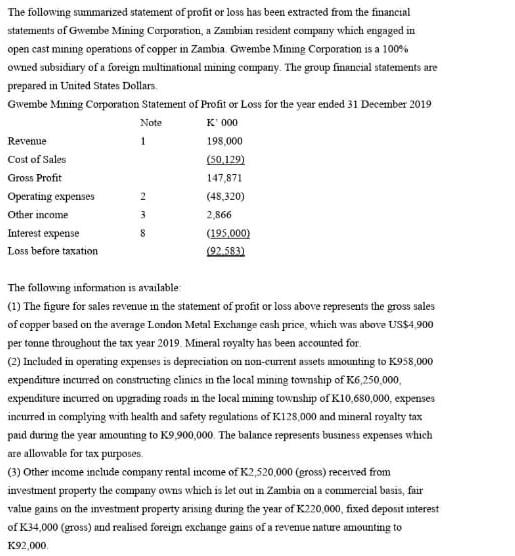

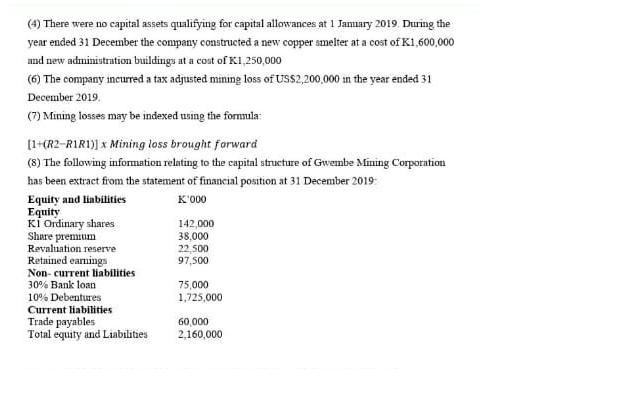

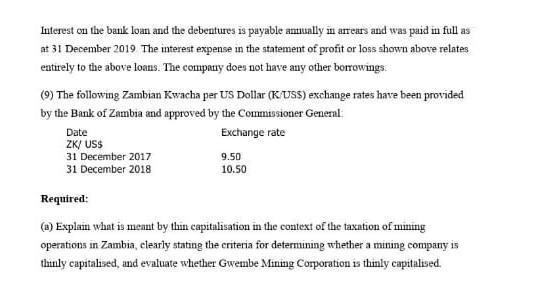

The following summarized statement of profit or loss has been extracted from the financial statements of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following summarized statement of profit or loss has been extracted from the financial statements of Gwembe Mining Corporation, a Zambian resident company which engaged in open cast mining operations of copper in Zambia Gwembe Mining Corporation is a 100% owned subsidiary of a foreign multinational mining company. The group financial statements are prepared in United States Dollars. Gwembe Mining Corporation Statement of Profit or Loss for the year ended 31 December 2019 Note K' 000 1 Revenue Cost of Sales Gross Profit Operating expenses Other income Interest expense Loss before taxation 2 3 198,000 (50,129) 147,871 (48,320) 2,866 (195,000) (92.583) The following information is available (1) The figure for sales revenue in the statement of profit or loss above represents the gross sales of copper based on the average London Metal Exchange cash price, which was above US$4.900 per tonne throughout the tax year 2019. Mineral royalty has been accounted for. (2) Included in operating expenses is depreciation on non-current assets amounting to K958,000 expenditure incurred on constructing clinics in the local mining township of K6,250,000, expenditure incurred on upgrading roads in the local mining township of K10,680,000, expenses incurred in complying with health and safety regulations of K128,000 and mineral royalty tax paid during the year amounting to K9,900,000. The balance represents business expenses which are allowable for tax purposes. (3) Other income include company rental income of K2,520,000 (gross) received from investment property the company owns which is let out in Zambia on a commercial basis, fair valne gains on the investment property arising during the year of K220,000, fixed deposit interest of K34,000 (gross) and realised foreign exchange gains of a revenue nature amounting to K92,000 (4) There were no capital assets qualifying for capital allowances at 1 January 2019. During the year ended 31 December the company constructed a new copper smelter at a cost of K1,600,000 and new administration buildings at a cost of K1,250,000 (6) The company incurred a tax adjusted mining loss of US$2,200,000 in the year ended 31 December 2019. (7) Mining losses may be indexed using the formula: [1+(R2-R1R1)] x Mining loss brought forward (8) The following information relating to the capital structure of Gwembe Mining Corporation has been extract from the statement of financial position at 31 December 2019 K'000 Equity and liabilities Equity KI Ordinary shares Share premium Revaluation reserve Retained earnings Non-current liabilities 30% Bank loan 10% Debentures Current liabilities Trade payables Total equity and Liabilities 142,000 38,000 22,500 97,500 75,000 1,725,000 60,000 2,160,000 Interest on the bank loan and the debentures is payable annually in arrears and was paid in full as at 31 December 2019 The interest expense in the statement of profit or loss shown above relates entirely to the above loans. The company does not have any other borrowings (9) The following Zambian Kwacha per US Dollar (K/USS) exchange rates have been provided by the Bank of Zambia and approved by the Commissioner General: Exchange rate Date ZK/ US$ 31 December 2017 31 December 2018 9.50 10.50 Required: (a) Explain what is meant by thin capitalisation in the context of the taxation of mining operations in Zambia, clearly stating the criteria for determining whether a mining company is thinly capitalised, and evaluate whether Gwembe Mining Corporation is thinly capitalised. (b) Compute the taxable business profits for the year ended 31 December 2019. (15 Marks) (e) Calculate the total amount of tax payable by the company for the tax year 2019 (4 Marks) The following summarized statement of profit or loss has been extracted from the financial statements of Gwembe Mining Corporation, a Zambian resident company which engaged in open cast mining operations of copper in Zambia Gwembe Mining Corporation is a 100% owned subsidiary of a foreign multinational mining company. The group financial statements are prepared in United States Dollars. Gwembe Mining Corporation Statement of Profit or Loss for the year ended 31 December 2019 Note K' 000 1 Revenue Cost of Sales Gross Profit Operating expenses Other income Interest expense Loss before taxation 2 3 198,000 (50,129) 147,871 (48,320) 2,866 (195,000) (92.583) The following information is available (1) The figure for sales revenue in the statement of profit or loss above represents the gross sales of copper based on the average London Metal Exchange cash price, which was above US$4.900 per tonne throughout the tax year 2019. Mineral royalty has been accounted for. (2) Included in operating expenses is depreciation on non-current assets amounting to K958,000 expenditure incurred on constructing clinics in the local mining township of K6,250,000, expenditure incurred on upgrading roads in the local mining township of K10,680,000, expenses incurred in complying with health and safety regulations of K128,000 and mineral royalty tax paid during the year amounting to K9,900,000. The balance represents business expenses which are allowable for tax purposes. (3) Other income include company rental income of K2,520,000 (gross) received from investment property the company owns which is let out in Zambia on a commercial basis, fair valne gains on the investment property arising during the year of K220,000, fixed deposit interest of K34,000 (gross) and realised foreign exchange gains of a revenue nature amounting to K92,000 (4) There were no capital assets qualifying for capital allowances at 1 January 2019. During the year ended 31 December the company constructed a new copper smelter at a cost of K1,600,000 and new administration buildings at a cost of K1,250,000 (6) The company incurred a tax adjusted mining loss of US$2,200,000 in the year ended 31 December 2019. (7) Mining losses may be indexed using the formula: [1+(R2-R1R1)] x Mining loss brought forward (8) The following information relating to the capital structure of Gwembe Mining Corporation has been extract from the statement of financial position at 31 December 2019 K'000 Equity and liabilities Equity KI Ordinary shares Share premium Revaluation reserve Retained earnings Non-current liabilities 30% Bank loan 10% Debentures Current liabilities Trade payables Total equity and Liabilities 142,000 38,000 22,500 97,500 75,000 1,725,000 60,000 2,160,000 Interest on the bank loan and the debentures is payable annually in arrears and was paid in full as at 31 December 2019 The interest expense in the statement of profit or loss shown above relates entirely to the above loans. The company does not have any other borrowings (9) The following Zambian Kwacha per US Dollar (K/USS) exchange rates have been provided by the Bank of Zambia and approved by the Commissioner General: Exchange rate Date ZK/ US$ 31 December 2017 31 December 2018 9.50 10.50 Required: (a) Explain what is meant by thin capitalisation in the context of the taxation of mining operations in Zambia, clearly stating the criteria for determining whether a mining company is thinly capitalised, and evaluate whether Gwembe Mining Corporation is thinly capitalised. (b) Compute the taxable business profits for the year ended 31 December 2019. (15 Marks) (e) Calculate the total amount of tax payable by the company for the tax year 2019 (4 Marks)

Expert Answer:

Answer rating: 100% (QA)

a Thin capitalization is a situation where a company is excessively financed by debt It is a tax avo... View the full answer

Related Book For

Financial Reporting and Analysis

ISBN: 978-0078025679

6th edition

Authors: Flawrence Revsine, Daniel Collins, Bruce, Mittelstaedt, Leon

Posted Date:

Students also viewed these accounting questions

-

Recently, the Department of Environmental in the Ministry of Energy, Science, Technology, Environment and Climate Change has revised the Environmental Quality (Clean Air) Regulations. The Regulations...

-

(Q3-A) Choose the correct answer for eight only 1-Two hollow balls made of (a- Steel and b- Aluminum) both have the same dimension and were floating in water, the buoyancy force was A) Greater in the...

-

Imagine a two-state world with a financial market. In the market, there is a stock with current price 100. In the next period, the stock either rises to 110 with a 60% probability or declines to 90...

-

Which of the following in not a function of DBA? A. Network Maintenance B. Routine Maintenance C. Schema Definition D. Authorization for data access

-

Explain why we do not add the denominators of two fractions when we add the fractions.

-

Make a substitution to express the integrand as a rational function and then evaluate the integral. e* ,2x - dx (e* 2)(e2* + 1) (e*

-

At the end of the accounting period, a journal entry is made to close variance accounts to_or________________________,and________________________,.

-

Andretti Company has a single product called a Dak. The company normally produces and sells 60.000 Daks each year at a selling price of $32 per unit. The companys unit costs at this level of activity...

-

VI. In 2 years, it is expected there will be a large equity raise. In this event, the debenture (principal and accrued interest) will be converted into equity at a 15% discount to the price of the...

-

Wayland Custom Woodworking is a firm that manufactures custom cabinets and woodwork for business and residential customers. Students will have the opportunity to establish payroll records and to...

-

. Sheridan Company sells goods on credit that cost $299,000 to Steven Company for $404,000 on January 2, 2025. The sales price includes an installation fee, which has a standalone selling price of...

-

Why is the subject of obsolete inventory discussed with top management and included in the management representation letter?

-

Which of the following is the most effective internal control structure procedure to detect vouchers that were prepared for the payment of goods that were not received? a. Count goods upon receipt in...

-

Give three objections to the practice of recording a tax loss carryforward prior to realization.

-

What background knowledge must an auditor possess to effectively audit income tax liability and expense?

-

A company did not recognize the benefit of a tax loss carryforward in the year of the loss. Two years later, the balance of probability shifts, and it appears that the loss will likely be used in the...

-

Henrich is a single taxpayer. In 2022, his taxable income is$483,000. What are his income tax and net investment income taxliability in each of the following alternative scenarios? Use TaxRate Sche 2...

-

Explain the buyers position in a typical negotiation for a business. Explain the sellers position. What tips would you offer a buyer about to begin negotiating the purchase of a business?

-

Tail O the Dog operates a chain of seven gourmet hot dog stands in southern California. The firms first stand, built in 1948, was shaped like (what else?) a giant hot dog, in a giant hot dog bun, and...

-

Whole Foods Markets Compensation Committee determines a portion of executive bonuses qualitatively. For the quantitative portion, the Committee selects from 13 performance metrics. For the fiscal...

-

1. Which of the following qualifies as a hedged item? a. A companys work-in-process inventory of unfinished washers, dryers, and refrigerators. b. Credit card receivables at JCPenney. c. Bushels of...

-

Discuss ways in which securities issued by state and local governments are similar to corporate bonds.

-

What are reasons investors buy bonds?

-

You have decided to diversify your investment portfolio. To research, compare a type of corporate bond with a type of government security.

Study smarter with the SolutionInn App