A costing system is designed to monitor the costs incurred in a production system. The system...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

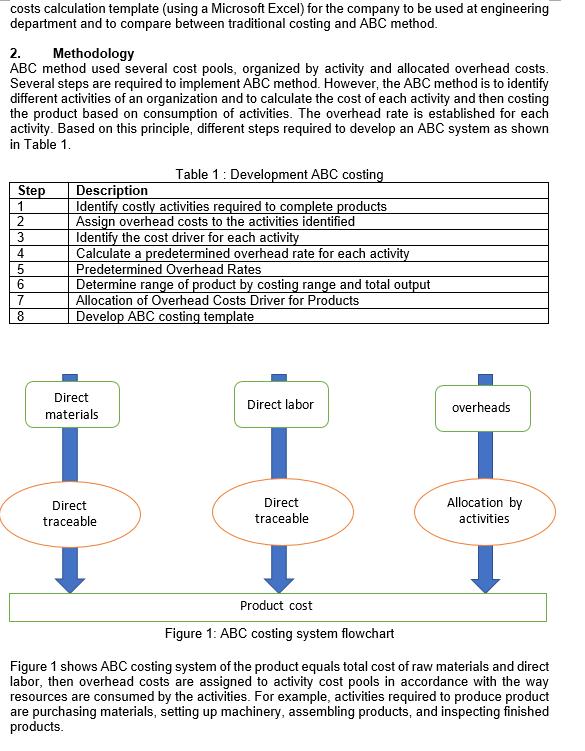

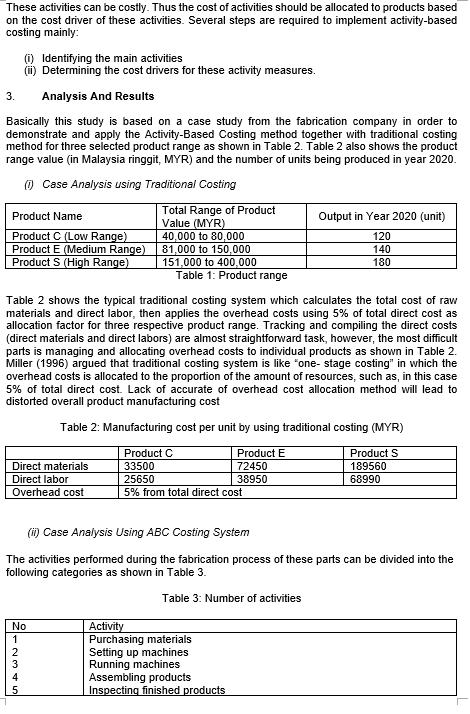

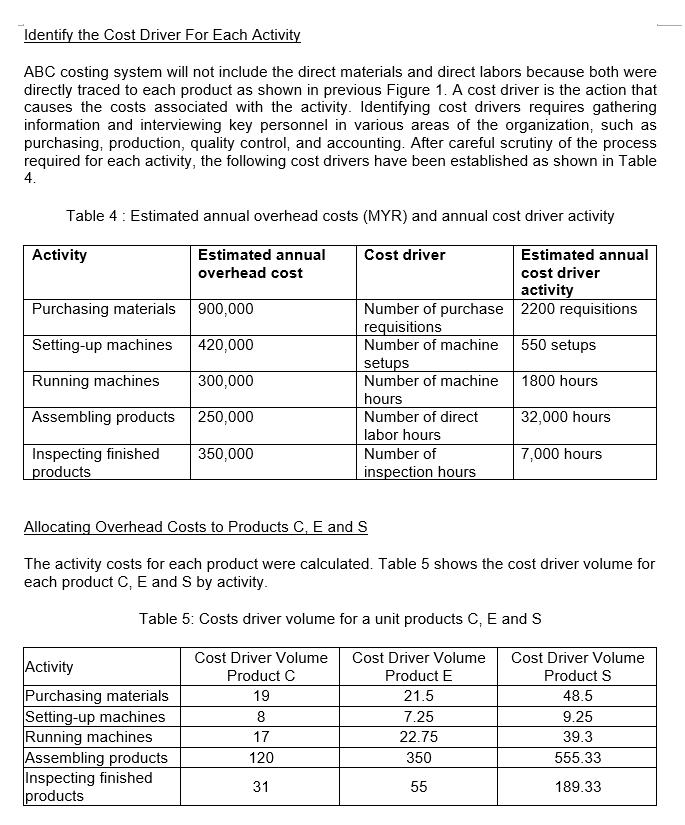

A costing system is designed to monitor the costs incurred in a production system. The system comprises of a set of forms, processes, controls, and reports that are designed to aggregate and report to management about revenues, costs, and profitability. Most manufacturing businesses around the world initially develop their costing system prior placing their products in the market. There are basically two types of costing system that the businesses are currently follows: Traditional costing method and activity based costing method. On the one hand, traditional costing system calculates the total cost of raw material and direct labor, then allocates the overhead costs using arbitrary allocation factors such as direct labor hours (Rezaie et al., 2008). On the other hand, ABC is being developed by Cooper and Kaplan (1991) as an alternative to solve the arbitrary overhead allocation problems. ABC attributes variable, fixed and overhead directly to each product by using the activities require to produce the product in accordance with the way resources are consumed by the activities (Cooper, 1990; Cokins, 1996) An example in manufacturing industries such as, forging industry (Rezaie et al., 2008), rebar fabrication (Young Woo et al., 2011), machine assembly (Gunasekaran, 1999) and others (Alnestig and Segerstedt, 1996; Baxendale, 2001) do have teams to come out with costing calculation on each product. In this study, the real life example of case study company was chosen to demonstrate the calculation of manufacturing costs between traditional costing and ABC method. Manufacturing costs is defined as those costs that are directly involved in manufacturing of product which consists of direct material, direct labor and manufacturing overhead (Horngren et al., 1999). The main business of this selected company is to fabricate special vehicles components such as petrol tankers, diesel tankers, vacuum tankers, aircraft refuelers and others. Currently, the company is using traditional costing system to calculate its product manufacturing costs. The purpose of the study is to develop a ABC manufacturing costs calculation template (using a Microsoft Excel) for the company to be used at engineering department and to compare between traditional costing and ABC method. 2. Methodology ABC method used several cost pools, organized by activity and allocated overhead costs. Several steps are required to implement ABC method. However, the ABC method is to identify different activities of an organization and to calculate the cost of each activity and then costing the product based on consumption of activities. The overhead rate is established for each activity. Based on this principle, different steps required to develop an ABC system as shown in Table 1. Step 1 انه ای ماساه اباده 2 3 4 5 6 7 8 Table 1: Development ABC costing Description Identify costly activities required to complete products Assign overhead costs to the activities identified Identify the cost driver for each activity Calculate a predetermined overhead rate for each activity Predetermined Overhead Rates Determine range of product by costing range and total output Allocation of Overhead Costs Driver for Products Develop ABC costing template Direct materials Direct traceable Direct labor Direct traceable overheads Allocation by activities Product cost Figure 1: ABC costing system flowchart Figure 1 shows ABC costing system of the product equals total cost of raw materials and direct labor, then overhead costs are assigned to activity cost pools in accordance with the way resources are consumed by the activities. For example, activities required to produce product are purchasing materials, setting up machinery, assembling products, and inspecting finished products. These activities can be costly. Thus the cost of activities should be allocated to products based on the cost driver of these activities. Several steps are required to implement activity-based costing mainly: (i) Identifying the main activities (ii) Determining the cost drivers for these activity measures. Analysis And Results Basically this study is based on a case study from the fabrication company in order to demonstrate and apply the Activity-Based Costing method together with traditional costing method for three selected product range as shown in Table 2. Table 2 also shows the product range value (in Malaysia ringgit, MYR) and the number of units being produced in year 2020. (1) Case Analysis using Traditional Costing 3. Product Name Product C (Low Range) Product E (Medium Range) Product S (High Range) Direct materials Direct labor Overhead cost Table 2 shows the typical traditional costing system which calculates the total cost of raw materials and direct labor, then applies the overhead costs using 5% of total direct cost as allocation factor for three respective product range. Tracking and compiling the direct costs (direct materials and direct labors) are almost straightforward task, however, the most difficult parts is managing and allocating overhead costs to individual products as shown in Table 2. Miller (1996) argued that traditional costing system is like "one- stage costing" in which the overhead costs is allocated to the proportion of the amount of resources, such as, in this case 5% of total direct cost. Lack of accurate of overhead cost allocation method will lead to distorted overall product manufacturing cost Table 2: Manufacturing cost per unit by using traditional costing (MYR) Product S 189560 68990 No Total Range of Product Value (MYR) 40,000 to 80,000 81,000 to 150,000 151,000 to 400,000 12445 Table 1: Product range 3 Product C 33500 25650 5% from total direct cost (ii) Case Analysis Using ABC Costing System The activities performed during the fabrication process of these parts can be divided into the following categories as shown in Table 3. Table 3: Number of activities Product E 72450 38950 Output in Year 2020 (unit) 120 140 180 Activity Purchasing materials Setting up machines. Running machines Assembling products Inspecting finished products Identify the Cost Driver For Each Activity ABC costing system will not include the direct materials and direct labors because both were directly traced to each product as shown in previous Figure 1. A cost driver is the action that causes the costs associated with the activity. Identifying cost drivers requires gathering information and interviewing key personnel in various areas of the organization, such as purchasing, production, quality control, and accounting. After careful scrutiny of the process required for each activity, the following cost drivers have been established as shown in Table 4. Table 4: Estimated annual overhead costs (MYR) and annual cost driver activity Cost driver Estimated annual overhead cost Estimated annual cost driver activity 2200 requisitions 550 setups Activity Purchasing materials 900,000 Setting-up machines 420,000 Running machines 300,000 Assembling products 250,000 Inspecting finished 350,000 products Activity Purchasing materials Setting-up machines Running machines Assembling products Inspecting finished products Cost Driver Volume Product C 19 Number of purchase requisitions Number of machine setups Number of machine hours Number of direct labor hours Allocating Overhead Costs to Products C, E and S The activity costs for each product were calculated. Table 5 shows the cost driver volume for each product C, E and S by activity. Table 5: Costs driver volume for a unit products C, E and S 8 17 120 31 Number of inspection hours 1800 hours Cost Driver Volume Product E 21.5 7.25 22.75 350 55 32,000 hours 7,000 hours Cost Driver Volume Product S 48.5 9.25 39.3 555.33 189.33 Prepare ABC template that shows: Calculation of rate for each cost driver and assign those cost to the range of products. (ii) Illustrates how the activity costs were allocated to three different product C,E and S. Discuss how the highest cost driver rate (that is, purchasing materials, setting up machine) can be reduced to improve profitability of each product. (iv) Analyse the cost structure of Product C,E and S. (v) (i) Show the comparison of cost between ABC and traditional costing system and percentage of variation in manufacturing cost for each product. (vi) Highlights the differences in accuracy and complexity of these 2 methods derive from earlier calculations. (vii) Provide conclusion from the analysis conducted between traditional costing system and ABC system with suggestion for effective costing method between that two. A costing system is designed to monitor the costs incurred in a production system. The system comprises of a set of forms, processes, controls, and reports that are designed to aggregate and report to management about revenues, costs, and profitability. Most manufacturing businesses around the world initially develop their costing system prior placing their products in the market. There are basically two types of costing system that the businesses are currently follows: Traditional costing method and activity based costing method. On the one hand, traditional costing system calculates the total cost of raw material and direct labor, then allocates the overhead costs using arbitrary allocation factors such as direct labor hours (Rezaie et al., 2008). On the other hand, ABC is being developed by Cooper and Kaplan (1991) as an alternative to solve the arbitrary overhead allocation problems. ABC attributes variable, fixed and overhead directly to each product by using the activities require to produce the product in accordance with the way resources are consumed by the activities (Cooper, 1990; Cokins, 1996) An example in manufacturing industries such as, forging industry (Rezaie et al., 2008), rebar fabrication (Young Woo et al., 2011), machine assembly (Gunasekaran, 1999) and others (Alnestig and Segerstedt, 1996; Baxendale, 2001) do have teams to come out with costing calculation on each product. In this study, the real life example of case study company was chosen to demonstrate the calculation of manufacturing costs between traditional costing and ABC method. Manufacturing costs is defined as those costs that are directly involved in manufacturing of product which consists of direct material, direct labor and manufacturing overhead (Horngren et al., 1999). The main business of this selected company is to fabricate special vehicles components such as petrol tankers, diesel tankers, vacuum tankers, aircraft refuelers and others. Currently, the company is using traditional costing system to calculate its product manufacturing costs. The purpose of the study is to develop a ABC manufacturing costs calculation template (using a Microsoft Excel) for the company to be used at engineering department and to compare between traditional costing and ABC method. 2. Methodology ABC method used several cost pools, organized by activity and allocated overhead costs. Several steps are required to implement ABC method. However, the ABC method is to identify different activities of an organization and to calculate the cost of each activity and then costing the product based on consumption of activities. The overhead rate is established for each activity. Based on this principle, different steps required to develop an ABC system as shown in Table 1. Step 1 انه ای ماساه اباده 2 3 4 5 6 7 8 Table 1: Development ABC costing Description Identify costly activities required to complete products Assign overhead costs to the activities identified Identify the cost driver for each activity Calculate a predetermined overhead rate for each activity Predetermined Overhead Rates Determine range of product by costing range and total output Allocation of Overhead Costs Driver for Products Develop ABC costing template Direct materials Direct traceable Direct labor Direct traceable overheads Allocation by activities Product cost Figure 1: ABC costing system flowchart Figure 1 shows ABC costing system of the product equals total cost of raw materials and direct labor, then overhead costs are assigned to activity cost pools in accordance with the way resources are consumed by the activities. For example, activities required to produce product are purchasing materials, setting up machinery, assembling products, and inspecting finished products. These activities can be costly. Thus the cost of activities should be allocated to products based on the cost driver of these activities. Several steps are required to implement activity-based costing mainly: (i) Identifying the main activities (ii) Determining the cost drivers for these activity measures. Analysis And Results Basically this study is based on a case study from the fabrication company in order to demonstrate and apply the Activity-Based Costing method together with traditional costing method for three selected product range as shown in Table 2. Table 2 also shows the product range value (in Malaysia ringgit, MYR) and the number of units being produced in year 2020. (1) Case Analysis using Traditional Costing 3. Product Name Product C (Low Range) Product E (Medium Range) Product S (High Range) Direct materials Direct labor Overhead cost Table 2 shows the typical traditional costing system which calculates the total cost of raw materials and direct labor, then applies the overhead costs using 5% of total direct cost as allocation factor for three respective product range. Tracking and compiling the direct costs (direct materials and direct labors) are almost straightforward task, however, the most difficult parts is managing and allocating overhead costs to individual products as shown in Table 2. Miller (1996) argued that traditional costing system is like "one- stage costing" in which the overhead costs is allocated to the proportion of the amount of resources, such as, in this case 5% of total direct cost. Lack of accurate of overhead cost allocation method will lead to distorted overall product manufacturing cost Table 2: Manufacturing cost per unit by using traditional costing (MYR) Product S 189560 68990 No Total Range of Product Value (MYR) 40,000 to 80,000 81,000 to 150,000 151,000 to 400,000 12445 Table 1: Product range 3 Product C 33500 25650 5% from total direct cost (ii) Case Analysis Using ABC Costing System The activities performed during the fabrication process of these parts can be divided into the following categories as shown in Table 3. Table 3: Number of activities Product E 72450 38950 Output in Year 2020 (unit) 120 140 180 Activity Purchasing materials Setting up machines. Running machines Assembling products Inspecting finished products Identify the Cost Driver For Each Activity ABC costing system will not include the direct materials and direct labors because both were directly traced to each product as shown in previous Figure 1. A cost driver is the action that causes the costs associated with the activity. Identifying cost drivers requires gathering information and interviewing key personnel in various areas of the organization, such as purchasing, production, quality control, and accounting. After careful scrutiny of the process required for each activity, the following cost drivers have been established as shown in Table 4. Table 4: Estimated annual overhead costs (MYR) and annual cost driver activity Cost driver Estimated annual overhead cost Estimated annual cost driver activity 2200 requisitions 550 setups Activity Purchasing materials 900,000 Setting-up machines 420,000 Running machines 300,000 Assembling products 250,000 Inspecting finished 350,000 products Activity Purchasing materials Setting-up machines Running machines Assembling products Inspecting finished products Cost Driver Volume Product C 19 Number of purchase requisitions Number of machine setups Number of machine hours Number of direct labor hours Allocating Overhead Costs to Products C, E and S The activity costs for each product were calculated. Table 5 shows the cost driver volume for each product C, E and S by activity. Table 5: Costs driver volume for a unit products C, E and S 8 17 120 31 Number of inspection hours 1800 hours Cost Driver Volume Product E 21.5 7.25 22.75 350 55 32,000 hours 7,000 hours Cost Driver Volume Product S 48.5 9.25 39.3 555.33 189.33 Prepare ABC template that shows: Calculation of rate for each cost driver and assign those cost to the range of products. (ii) Illustrates how the activity costs were allocated to three different product C,E and S. Discuss how the highest cost driver rate (that is, purchasing materials, setting up machine) can be reduced to improve profitability of each product. (iv) Analyse the cost structure of Product C,E and S. (v) (i) Show the comparison of cost between ABC and traditional costing system and percentage of variation in manufacturing cost for each product. (vi) Highlights the differences in accuracy and complexity of these 2 methods derive from earlier calculations. (vii) Provide conclusion from the analysis conducted between traditional costing system and ABC system with suggestion for effective costing method between that two.

Expert Answer:

Related Book For

Transportation A Global Supply Chain Perspective

ISBN: 9781337406642

9th Edition

Authors: Robert A. Novack, Brian Gibson, Yoshinori Suzuki, John J. Coyle

Posted Date:

Students also viewed these accounting questions

-

summarize this article TITLE Overhead cost pools. By: Lambert III, S.J., Chen, Kung H., Internal Auditor, 00205745, Oct96, Vol. 53, Issue 5 DATA BASE Business Source Complete Internal auditors who...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

The firm is considering between two mutually exclusive projects, Project A and Project B, that each require an upfront investment of $100m and are expected to produce free cash flow (FCF) only at the...

-

Alam Company is a manufacturing firm that uses job-order costing. At the beginning of the year, the company's inventory balances were as follows: Raw materials $ 25,400 Work in process $ 74,400...

-

Serendipity Sound, Inc., manufactures home theater sound systems in its Minneapolis Division. The divisional sales manager has estimated the following demand-curve data. Quantity Sold per Month Unit...

-

During economic or industry recessions, it is common to see downward revisions of bond ratings. Access Standard & Poors list of companies with lowered bond ratings and identify three whose names you...

-

Capacity management, denominator-level capacity concepts Capacity management, denominator-level capacity concepts match each of the following items with one or more of the denominator-level capacity...

-

I have no idea about my take home quiz. Please help me. ACCT: 2100 Introduction to Financial Accounting Spring 2016 Chapter 9 Take-Home Quiz Required: On March 17, 2016 you won $527.25 million in the...

-

The members of the Vistas Club are planning a month long hiking and camping trip through the Blue Ridge Mountains, from north Georgia to Virginia. There are a number of trails through the mountains...

-

In a toxic work environment, with toxic leaders, what methods or tools would you use from this course to improve culture, your work performance and other working conditions? How can you prevent yourse

-

Bottles Sold Napa Valley Winery has sought your expertise to help them compare forecasted sales using a regression trendline approach and exponential smoothing. They face a very pronounced seasonal...

-

XYZ Ltd. is evaluating two potential projects, Project X and Project Y. The expected net cash flows for both projects over five years are given below: Projected Net Cash Flows (in thousands of...

-

Watershed is a media services company that provides online streaming movie and television content. As a result of the competitive market of streaming service providers, Watershed is interested in...

-

XYZ Ltd. plans to invest in a new machine costing $8,000, expected to generate cash inflows of $2,500 annually for four years. Requirements: Calculate the NPV using a discount rate of 14%. Compute...

-

Draft a corporate constitution for your family convenient store in australia

-

Search either a Fiji or overseas based fraud case and answer the following questions: 1. Who committed the fraud? (Such as what was the position of the person who committed the fraud?) (0.25 mark) 2....

-

Calculate the Lagrange polynomial P 2 (x) for the values (1.00) = 1.0000, (1.02) = 0.9888, (1.04) = 0.9784 of the gamma function [(24) in App. A3.1] and from it approximations of (1.01) and (1.03).

-

Company Overview TEA Logistics Services, Inc. (TEA) was started in 2005 by three siblings in a family that had a long history of involvement in logistics. TEA began operations primarily as a freight...

-

The United States air traffic control system, managed by the Federal Aviation Administration (FAA), provides the necessary guidance for aircraft to fly safely between and origindestination pair. The...

-

What groups play a role in the development of national transportation policy? What roles does each group take?

-

Use the data in P 7 for this problem. Required 1. Prepare entries in journal form (refer to the review problem) to record the transactions, assuming use of the periodic inventory system. 2. User...

-

Books Unlimited is a well-established chain of 20 bookstores in western Ohio. In recent years the company has grown rapidly, adding five new stores in regional malls. The manager of each store...

-

Roman Sound Source, Inc., has operated in Kansas for 30 years. The company has always prided itself on providing individual attention to its customers. It carries a large inventory so it can offer a...

Study smarter with the SolutionInn App