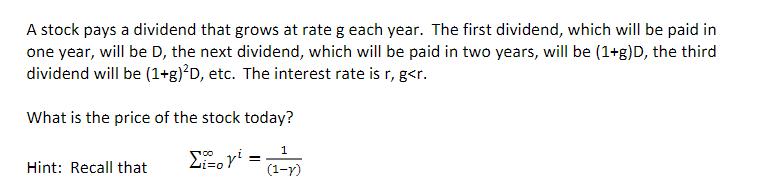

A stock pays a dividend that grows at rate g each year. The first dividend, which...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Stock Price with Growing Dividends The formula for the price P of a stock that pays a constant dividend D that grows at a rate g each year with an interest rate r and g r is P D r g This formula uses ... View the full answer

Related Book For

Foundations of Financial Management

ISBN: 978-1259024979

10th Canadian edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

Posted Date: