Soleh Ali, the founder and owner of Soleh Kopi-O, put down the book he was reading...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

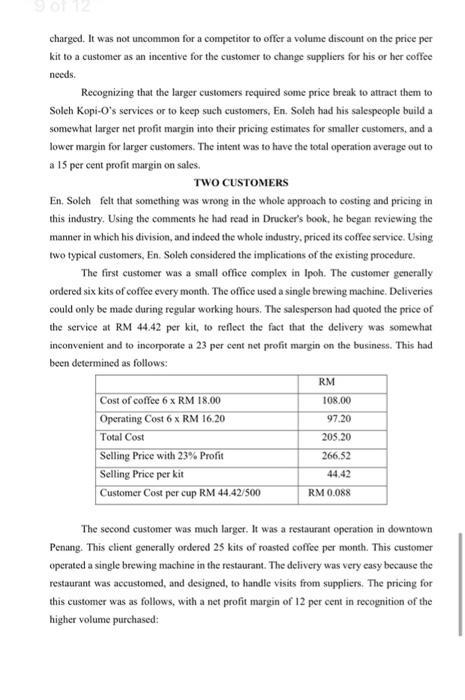

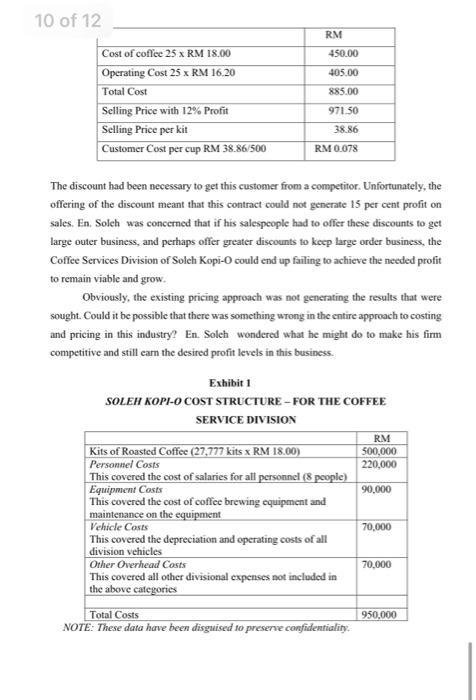

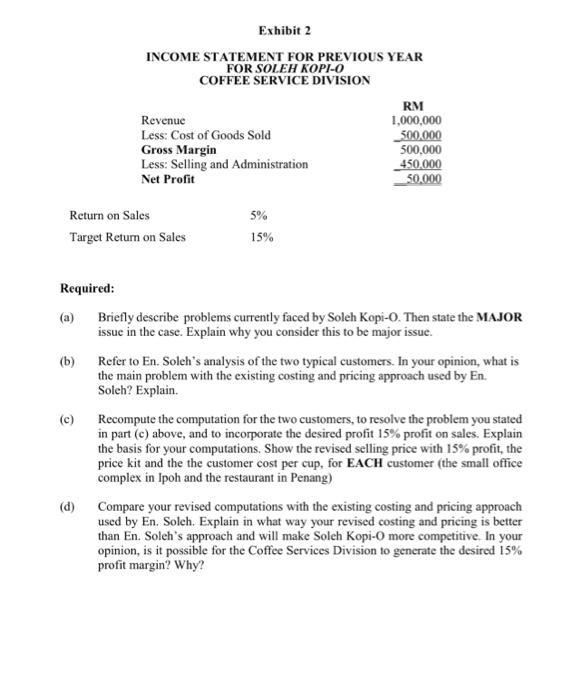

Soleh Ali, the founder and owner of Soleh Kopi-O, put down the book he was reading and thought, "Is Drucker right, that most companies do not know the true unit costs of their business?" It had been two years since his firm entered the food service industry in Penang. En. Soleh now wondered what he might do to make his new division competitive with the giants, and yet generate the kind of returns he felt were necessary and appropriate for his investment. Solch Ali had spent most of his working career in the coffee business. He had worked in all aspects, from roasting the beans to selling the finished product both wholesale and retail. Over the years he had worked in both large and small firms. When the opportunity arose, be invested money and effort into building his own business, Soleh Kopi-O, and focused on the roasting and selling of packaged coffee to the "Away from Home" coffee market. AWAY FROM HOME COFFEE MARKET The "Away from Home" coffee market designation included all coffee consumed outside of the retail market. Conventional customers in this market included restaurants, hospitals, stadiums, catering trucks and the like. Because of the volume of coffee purchased, these customers found it advantageous to deal directly with roasters, as opposed to purchasing their needs through the retail channel. The roasters generally sold the coffee to these customers priced by the kilogram. Over time, a segment of this market emerged called coffee service. It consisted primarily of very small customers such as business offices. Unfortunately, these customers required frequent purchases of small quantities of coffee. Traditionally, roasters avoided this segment because the cost of serving such small customers was greater than the gross profit generated from the sales transaction of the coffee. If the roaster raised the price to cover this shortfall in margin from selling coffee by the kilogram, the increased price per kg compared unfavorably with the amount that the customer could pay a general wholesaler or even a retail store. To address this need in the segment, entrepreneurs formed businesses. Often they operated out of their own homes. These coffee service operators acted as middlemen between the roasters and the small customers. The operator purchased significant volumes of packaged coffee from the roaster. This coffee was then re-packaged into"kits"-akit being equivalent to 500 cups of coffee. As part of the service the operator would also provide the customer with: . . Rented coffee brewing equipment Free maintenance of the equipment Packaged coffee ready for use Delivery to the customer's location Allied products such as tea, hot chocolate, cups etc. To simplify the process, the coffee service operator would offer the complete package of service to the customer at "so much per cup" or per kit. This avoided the kg price comparison. As well, the quoted price included charges for the equipment, the supplies such as filters, and the coffee. Gradually, as more Away from Home customers began using the smaller and more flexible coffee machines, the industry began to specialize. The customers wanted pot-sized packages, filters and more frequent delivery services. Some of the larger roasters created distribution operations to serve this market. These distribution services adopted the practice of selling the coffee to customers in this market "by the cup" or by the kit. SETTING UP OF SOLEH KOPI-O At its inception, Soleh Kopi-O faced a broad range of competitors. Aside from the giant roasters such as Maxwell House and Nescafe, there were national coffee service firms such as Hang Tuah Coffee and Kopi-O Asli. Other companies operated within a particular geographic region, for example, Butterworth. Finally, there were the local competitors who handled the coffee service segment of the market. Initially, Soleh Kopi-O was only a roasting operation selling to distributors. Two years ago, Soleh Kopi-O began operating a food service division in the Penang area. En. Solch felt that the market was large enough to allow a new firm to enter the business successfully. This division also gave him the opportunity to try out some of his ideas on how such a business might be run. Roasting Operations Soleh Kopi-O operated its own roasting plant. The company purchased and stored green coffee beans. Given the volume of the company's business, Soleh Kopi-O could not afford to buy a full shipload of green coffee. Instead, it purchased its green coffee needs through a local broker. There was a wide variety of green coffee beans available in the world from some 45 exporting countries. The quality and price levels for these beans were spread over a fairly wide spectrum. By carefully blending less expensive beans in the roasting process with higher grade coffees, it was possible to reduce the material cost of some blends of coffee. The green coffee beans were delivered in 60- or 70-kg bags from places such as Africa, India, Mexico and South America. In this green state, the beans could be stored for relatively long periods of time. Once roasted and ready for brewing, coffee would become stale very quickly. The use of high grade, expensive packaging would keep coffee fresh for perhaps six months. This allowed food service operators the chance to deliver their product less frequently than in the past. The first stage of the roasting process involved loading a charge of green coffee beans into a roaster. The mix of beans used in the charge was based upon the recipe for a specific blend of coffee ordered by the customer. Depending on the size of the roaster, a charge of beans could be as small as one or as large as four of the 60- to 70-kg bags. This operation involved blowing hot air through the beans until they were heated to approximately 400°F. In this heating stage, the beans burst open, and discarded a shell called the chaff. The flow of hot air carried the very light chaff to a separator. The roasted beans, when cooled, were transported mechanically to a grinder, where they were ground into finer particles. To keep the flavor of the roasting process, it was necessary to package the coffee quickly. The ground roasted coffee was taken to an automated packaging machine which loaded the coffee into sealed packages for the customer. Most of the roasting and grinding equipment had been functioning for more than 30 years. Although the equipment was not new in terms of design, the process was not labor intensive to convert the beans from their green state into packaged coffee. Nevertheless, the cumulative cost of the direct and indirect labor was significantly more than the cost for the energy to roast the beans. The roasting and grinding process involved a significant amount of shrinkage of green coffee beans. Approximately 12 per cent of the weight disappeared in the roasting process due to moisture loss. A further four per cent of the weight disappeared due to combustible material loss. Some beans were lost in the process of separating the chaff. On rare occasions a malfunction in the roaster would burn the beans, making the charge useless for commercial purposes. Finally, some beans simply turned into powder during the grinding stage and could not be packaged To accommodate this loss of materials by shrinkage, the cost of green coffee was expressed in terms of the yield of roasted products. Soleh Kopi-O estimated a cost of RM 2.15 in green beans for each kg of roasted coffee produced. The additional productions costs, including direct and indirect production labor, packaging materials, depreciation on the equipment, and general production overhead for the roasting plant, were estimated at RM 0.35 per kg of roasted coffee. Some of the regional firms and all of the local competitors had to purchase their coffee from roasters before selling it to customers. Several coffee service distributors purchased coffee from Soleh Kopi-O roasting division in kits. A kit of coffee consisted of 42 packages, each weighing 1.75 grams. The cost of the kit varied depending upon the blend of coffee involved. The kits also included filters for the brewing operation. Currently, the roasting division priced the kit at the cost of the roasted coffee, the cost of the filters, and a margin to cover administrative costs and profit. Last year, the average market price of a kit to coffee service operators was RM 18.00. In order to properly evaluate the different operations within Solch Kopi-O, each unit functioned at arm's length from each other. This meant that the roasted coffee was sold to the Coffee Services Division at the same prices that it was sold to competing distributors. This policy avoided the problem of cross subsidization between functions. Coffee Services Division In the food service division, the task involved salespeople contacting potential customers, assessing their needs and quoting them a price for the service. This process involved a visit to the customer's site to evaluate the operation. On this visit, the salesperson determined the type and quantity of equipment needed for an efficient coffee service in the location. The salesperson also estimated the annual volume and blend of coffee that the customer wanted. This included the frequency with which the customer expected to be resupplied. Using this information, the salesperson quoted one all-inclusive price for the service to the customer. This was expressed as the price per lot of coffee ordered or the cost per brewed cup. After the contract was signed, the distribution operation of the division became involved. The customer phoned in an order indicating how much coffee was desired, as well as any allied products. The clerk, upon receiving the call, filled out an invoice for the order and gave it to the dispatcher. The dispatcher arranged to have the contents of the invoice gathered from the division's warehouse, loaded on the delivery vehicle and taken to the customer. The driver who delivered the order dropped off the invoice and either collected for the order or had it signed for by the customer. The usual administrative overhead of telephones, clerk, files and records, accounting services and dispatch was needed. These items generally appeared to grow in chunks as the number of customers increased and the volume of order transactions grew. Last year, the annual cost of operating the administration, marketing and sales, and distribution activities was RM 450,000 (see Exhibit 1). Division Results Within two years, the Coffee Services Division of Soleh Kopi-O had grown to the point where it had a relatively stable customer base in the Penang area. Last year, it had sold approximately RM 1 million worth of coffee to some 1,000 customers and had handled in the range of 18,000 invoices. Given the competitive nature of the business, and the newness of Soleh Kopi-O's Coffee Services Division into the industry, the profit margin targeted from sales had been 15 per cent of the sales RM. En. Soleh felt that this represented a fair to return for the assets employed. Last year the average selling price of a kit" of roast coffee by the division had been well in line with the industry average. Unfortunately, the desired profit margin of 15 per cent of sales had not been attained. Instead, as Exhibit 2 shows, the profit margin had been lower than 10 per cent of sales. A National Coffee Service Association survey had reported that the average industry earnings had been even lower. Pricing The traditional pricing approach by the industry ensured that all costs of the operation were recovered in the selling price of the service. The operating costs charged to the customer were based upon the allocation of the sales and administration costs in relation to the kits of coffee that were sold the previous year. In the case of Soleh Kopi-O, this amounted to RM 16.20 per kit, for the 27,777 kits sold. The equipment cost involved charges for the brewing equipment used by the customers as well as maintenance. Based on last year's costs and sales volume, this cost was RM 3.24 per kit, and was included as part of the above RM16.20. Finally, the price was marked up to reflect the desired profit margin to the company. Customers ordered coffee in multiples of kits. The salesperson tried to arrange the size of order for the customer so that it was only necessary to make a delivery to the customer once a month. One of the key competitive dimensions in the food service industry ry was price. Customers paid from RM 25.00 to RM 45.00 per kit for coffee service from most distributors. Each of the distributors offered the same array of service in terms of equipment, coffee and allied products. The differences between suppliers were reflected in the price charged. It was not uncommon for a competitor to offer a volume discount on the price per kit to a customer as an incentive for the customer to change suppliers for his or her coffee needs. Recognizing that the larger customers required some price break to attract them to Soleh Kopi-O's services or to keep such customers, En. Solch had his salespeople build a somewhat larger net profit margin into their pricing estimates for smaller customers, and a lower margin for larger customers. The intent was to have the total operation average out to a 15 per cent profit margin on sales. TWO CUSTOMERS En. Solch felt that something was wrong in the whole approach to costing and pricing in this industry. Using the comments he had read in Drucker's book, he began reviewing the manner in which his division, and indeed the whole industry, priced its coffee service. Using two typical customers, En. Soleh considered the implications of the existing procedure. The first customer was a small office complex in Ipoh. The customer generally ordered six kits of coffee every month. The office used a single brewing machine. Deliveries could only be made during regular working hours. The salesperson had quoted the price of the service at RM 44.42 per kit, to reflect the fact that the delivery was somewhat inconvenient and to incorporate a 23 per cent net profit margin on the business. This had been determined as follows: Cost of coffee 6 x RM 18.00 Operating Cost 6 x RM 16.20 Total Cost Selling Price with 23% Profit Selling Price per kit Customer Cost per cup RM 44.42/500 RM 108.00 97.20 205.20 266.52 44.42 RM 0.088 The second customer was much larger. It was a restaurant operation in downtown Penang. This client generally ordered 25 kits of roasted coffee per month. This customer operated a single brewing machine in the restaurant. The delivery was very easy because the restaurant was accustomed, and designed, to handle visits from suppliers. The pricing for this customer was as follows, with a net profit margin of 12 per cent in recognition of the higher volume purchased: 10 of 12 Cost of coffee 25 x RM 18.00 Operating Cost 25 x RM 16.20 Total Cost Selling Price with 12% Profit Selling Price per kit Customer Cost per cup RM 38.86/500 RM 450.00 405.00 885.00 971.50 38.86 RM 0.078 The discount had been necessary to get this customer from a competitor. Unfortunately, the offering of the discount meant that this contract could not generate 15 per cent profit on sales. En. Solch was concerned that if his salespeople had to offer these discounts to get large outer business, and perhaps offer greater discounts to keep large order business, the Coffee Services Division of Soleh Kopi-O could end up failing to achieve the needed profit to remain viable and grow. Obviously, the existing pricing approach was not generating the results that were sought. Could it be possible that there was something wrong in the entire approach to costing and pricing in this industry? En. Soleh wondered what he might do to make his firm competitive and still earn the desired profit levels in this business. Exhibit 1 SOLEH KOPI-O COST STRUCTURE-FOR THE COFFEE SERVICE DIVISION Kits of Roasted Coffee (27,777 kits x RM 18.00) Personnel Costs This covered the cost of salaries for all personnel (8 people) Equipment Costs This covered the cost of coffee brewing equipment and maintenance on the equipment Vehicle Costs This covered the depreciation and operating costs of all division vehicles Other Overhead Costs This covered all other divisional expenses not included in the above categories Total Costs NOTE: These data have been disguised to preserve confidentiality RM 500,000 220,000 90,000 70,000 70,000 950,000 Required: Return on Sales Target Return on Sales (b) (c) Exhibit 2 INCOME STATEMENT FOR PREVIOUS YEAR FOR SOLEH KOPI-O COFFEE SERVICE DIVISION (d) Revenue Less: Cost of Goods Sold Gross Margin Less: Selling and Administration Net Profit 5% 15% RM 1,000,000 500.000 500,000 450.000 50,000 Briefly describe problems currently faced by Soleh Kopi-O. Then state the MAJOR issue in the case. Explain why you consider this to be major issue. Refer to En. Soleh's analysis of the two typical customers. In your opinion, what is the main problem with the existing costing and pricing approach used by En. Soleh? Explain. Recompute the computation for the two customers, to resolve the problem you stated in part (c) above, and to incorporate the desired profit 15% profit on sales. Explain the basis for your computations. Show the revised selling price with 15% profit, the price kit and the the customer cost per cup, for EACH customer (the small office complex in Ipoh and the restaurant in Penang) Compare your revised computations with the existing costing and pricing approach used by En. Soleh. Explain in what way your revised costing and pricing is better than En. Soleh's approach and will make Soleh Kopi-O more competitive. In your opinion, is it possible for the Coffee Services Division to generate the desired 15% profit margin? Why? Soleh Ali, the founder and owner of Soleh Kopi-O, put down the book he was reading and thought, "Is Drucker right, that most companies do not know the true unit costs of their business?" It had been two years since his firm entered the food service industry in Penang. En. Soleh now wondered what he might do to make his new division competitive with the giants, and yet generate the kind of returns he felt were necessary and appropriate for his investment. Solch Ali had spent most of his working career in the coffee business. He had worked in all aspects, from roasting the beans to selling the finished product both wholesale and retail. Over the years he had worked in both large and small firms. When the opportunity arose, be invested money and effort into building his own business, Soleh Kopi-O, and focused on the roasting and selling of packaged coffee to the "Away from Home" coffee market. AWAY FROM HOME COFFEE MARKET The "Away from Home" coffee market designation included all coffee consumed outside of the retail market. Conventional customers in this market included restaurants, hospitals, stadiums, catering trucks and the like. Because of the volume of coffee purchased, these customers found it advantageous to deal directly with roasters, as opposed to purchasing their needs through the retail channel. The roasters generally sold the coffee to these customers priced by the kilogram. Over time, a segment of this market emerged called coffee service. It consisted primarily of very small customers such as business offices. Unfortunately, these customers required frequent purchases of small quantities of coffee. Traditionally, roasters avoided this segment because the cost of serving such small customers was greater than the gross profit generated from the sales transaction of the coffee. If the roaster raised the price to cover this shortfall in margin from selling coffee by the kilogram, the increased price per kg compared unfavorably with the amount that the customer could pay a general wholesaler or even a retail store. To address this need in the segment, entrepreneurs formed businesses. Often they operated out of their own homes. These coffee service operators acted as middlemen between the roasters and the small customers. The operator purchased significant volumes of packaged coffee from the roaster. This coffee was then re-packaged into"kits"-akit being equivalent to 500 cups of coffee. As part of the service the operator would also provide the customer with: . . Rented coffee brewing equipment Free maintenance of the equipment Packaged coffee ready for use Delivery to the customer's location Allied products such as tea, hot chocolate, cups etc. To simplify the process, the coffee service operator would offer the complete package of service to the customer at "so much per cup" or per kit. This avoided the kg price comparison. As well, the quoted price included charges for the equipment, the supplies such as filters, and the coffee. Gradually, as more Away from Home customers began using the smaller and more flexible coffee machines, the industry began to specialize. The customers wanted pot-sized packages, filters and more frequent delivery services. Some of the larger roasters created distribution operations to serve this market. These distribution services adopted the practice of selling the coffee to customers in this market "by the cup" or by the kit. SETTING UP OF SOLEH KOPI-O At its inception, Soleh Kopi-O faced a broad range of competitors. Aside from the giant roasters such as Maxwell House and Nescafe, there were national coffee service firms such as Hang Tuah Coffee and Kopi-O Asli. Other companies operated within a particular geographic region, for example, Butterworth. Finally, there were the local competitors who handled the coffee service segment of the market. Initially, Soleh Kopi-O was only a roasting operation selling to distributors. Two years ago, Soleh Kopi-O began operating a food service division in the Penang area. En. Solch felt that the market was large enough to allow a new firm to enter the business successfully. This division also gave him the opportunity to try out some of his ideas on how such a business might be run. Roasting Operations Soleh Kopi-O operated its own roasting plant. The company purchased and stored green coffee beans. Given the volume of the company's business, Soleh Kopi-O could not afford to buy a full shipload of green coffee. Instead, it purchased its green coffee needs through a local broker. There was a wide variety of green coffee beans available in the world from some 45 exporting countries. The quality and price levels for these beans were spread over a fairly wide spectrum. By carefully blending less expensive beans in the roasting process with higher grade coffees, it was possible to reduce the material cost of some blends of coffee. The green coffee beans were delivered in 60- or 70-kg bags from places such as Africa, India, Mexico and South America. In this green state, the beans could be stored for relatively long periods of time. Once roasted and ready for brewing, coffee would become stale very quickly. The use of high grade, expensive packaging would keep coffee fresh for perhaps six months. This allowed food service operators the chance to deliver their product less frequently than in the past. The first stage of the roasting process involved loading a charge of green coffee beans into a roaster. The mix of beans used in the charge was based upon the recipe for a specific blend of coffee ordered by the customer. Depending on the size of the roaster, a charge of beans could be as small as one or as large as four of the 60- to 70-kg bags. This operation involved blowing hot air through the beans until they were heated to approximately 400°F. In this heating stage, the beans burst open, and discarded a shell called the chaff. The flow of hot air carried the very light chaff to a separator. The roasted beans, when cooled, were transported mechanically to a grinder, where they were ground into finer particles. To keep the flavor of the roasting process, it was necessary to package the coffee quickly. The ground roasted coffee was taken to an automated packaging machine which loaded the coffee into sealed packages for the customer. Most of the roasting and grinding equipment had been functioning for more than 30 years. Although the equipment was not new in terms of design, the process was not labor intensive to convert the beans from their green state into packaged coffee. Nevertheless, the cumulative cost of the direct and indirect labor was significantly more than the cost for the energy to roast the beans. The roasting and grinding process involved a significant amount of shrinkage of green coffee beans. Approximately 12 per cent of the weight disappeared in the roasting process due to moisture loss. A further four per cent of the weight disappeared due to combustible material loss. Some beans were lost in the process of separating the chaff. On rare occasions a malfunction in the roaster would burn the beans, making the charge useless for commercial purposes. Finally, some beans simply turned into powder during the grinding stage and could not be packaged To accommodate this loss of materials by shrinkage, the cost of green coffee was expressed in terms of the yield of roasted products. Soleh Kopi-O estimated a cost of RM 2.15 in green beans for each kg of roasted coffee produced. The additional productions costs, including direct and indirect production labor, packaging materials, depreciation on the equipment, and general production overhead for the roasting plant, were estimated at RM 0.35 per kg of roasted coffee. Some of the regional firms and all of the local competitors had to purchase their coffee from roasters before selling it to customers. Several coffee service distributors purchased coffee from Soleh Kopi-O roasting division in kits. A kit of coffee consisted of 42 packages, each weighing 1.75 grams. The cost of the kit varied depending upon the blend of coffee involved. The kits also included filters for the brewing operation. Currently, the roasting division priced the kit at the cost of the roasted coffee, the cost of the filters, and a margin to cover administrative costs and profit. Last year, the average market price of a kit to coffee service operators was RM 18.00. In order to properly evaluate the different operations within Solch Kopi-O, each unit functioned at arm's length from each other. This meant that the roasted coffee was sold to the Coffee Services Division at the same prices that it was sold to competing distributors. This policy avoided the problem of cross subsidization between functions. Coffee Services Division In the food service division, the task involved salespeople contacting potential customers, assessing their needs and quoting them a price for the service. This process involved a visit to the customer's site to evaluate the operation. On this visit, the salesperson determined the type and quantity of equipment needed for an efficient coffee service in the location. The salesperson also estimated the annual volume and blend of coffee that the customer wanted. This included the frequency with which the customer expected to be resupplied. Using this information, the salesperson quoted one all-inclusive price for the service to the customer. This was expressed as the price per lot of coffee ordered or the cost per brewed cup. After the contract was signed, the distribution operation of the division became involved. The customer phoned in an order indicating how much coffee was desired, as well as any allied products. The clerk, upon receiving the call, filled out an invoice for the order and gave it to the dispatcher. The dispatcher arranged to have the contents of the invoice gathered from the division's warehouse, loaded on the delivery vehicle and taken to the customer. The driver who delivered the order dropped off the invoice and either collected for the order or had it signed for by the customer. The usual administrative overhead of telephones, clerk, files and records, accounting services and dispatch was needed. These items generally appeared to grow in chunks as the number of customers increased and the volume of order transactions grew. Last year, the annual cost of operating the administration, marketing and sales, and distribution activities was RM 450,000 (see Exhibit 1). Division Results Within two years, the Coffee Services Division of Soleh Kopi-O had grown to the point where it had a relatively stable customer base in the Penang area. Last year, it had sold approximately RM 1 million worth of coffee to some 1,000 customers and had handled in the range of 18,000 invoices. Given the competitive nature of the business, and the newness of Soleh Kopi-O's Coffee Services Division into the industry, the profit margin targeted from sales had been 15 per cent of the sales RM. En. Soleh felt that this represented a fair to return for the assets employed. Last year the average selling price of a kit" of roast coffee by the division had been well in line with the industry average. Unfortunately, the desired profit margin of 15 per cent of sales had not been attained. Instead, as Exhibit 2 shows, the profit margin had been lower than 10 per cent of sales. A National Coffee Service Association survey had reported that the average industry earnings had been even lower. Pricing The traditional pricing approach by the industry ensured that all costs of the operation were recovered in the selling price of the service. The operating costs charged to the customer were based upon the allocation of the sales and administration costs in relation to the kits of coffee that were sold the previous year. In the case of Soleh Kopi-O, this amounted to RM 16.20 per kit, for the 27,777 kits sold. The equipment cost involved charges for the brewing equipment used by the customers as well as maintenance. Based on last year's costs and sales volume, this cost was RM 3.24 per kit, and was included as part of the above RM16.20. Finally, the price was marked up to reflect the desired profit margin to the company. Customers ordered coffee in multiples of kits. The salesperson tried to arrange the size of order for the customer so that it was only necessary to make a delivery to the customer once a month. One of the key competitive dimensions in the food service industry ry was price. Customers paid from RM 25.00 to RM 45.00 per kit for coffee service from most distributors. Each of the distributors offered the same array of service in terms of equipment, coffee and allied products. The differences between suppliers were reflected in the price charged. It was not uncommon for a competitor to offer a volume discount on the price per kit to a customer as an incentive for the customer to change suppliers for his or her coffee needs. Recognizing that the larger customers required some price break to attract them to Soleh Kopi-O's services or to keep such customers, En. Solch had his salespeople build a somewhat larger net profit margin into their pricing estimates for smaller customers, and a lower margin for larger customers. The intent was to have the total operation average out to a 15 per cent profit margin on sales. TWO CUSTOMERS En. Solch felt that something was wrong in the whole approach to costing and pricing in this industry. Using the comments he had read in Drucker's book, he began reviewing the manner in which his division, and indeed the whole industry, priced its coffee service. Using two typical customers, En. Soleh considered the implications of the existing procedure. The first customer was a small office complex in Ipoh. The customer generally ordered six kits of coffee every month. The office used a single brewing machine. Deliveries could only be made during regular working hours. The salesperson had quoted the price of the service at RM 44.42 per kit, to reflect the fact that the delivery was somewhat inconvenient and to incorporate a 23 per cent net profit margin on the business. This had been determined as follows: Cost of coffee 6 x RM 18.00 Operating Cost 6 x RM 16.20 Total Cost Selling Price with 23% Profit Selling Price per kit Customer Cost per cup RM 44.42/500 RM 108.00 97.20 205.20 266.52 44.42 RM 0.088 The second customer was much larger. It was a restaurant operation in downtown Penang. This client generally ordered 25 kits of roasted coffee per month. This customer operated a single brewing machine in the restaurant. The delivery was very easy because the restaurant was accustomed, and designed, to handle visits from suppliers. The pricing for this customer was as follows, with a net profit margin of 12 per cent in recognition of the higher volume purchased: 10 of 12 Cost of coffee 25 x RM 18.00 Operating Cost 25 x RM 16.20 Total Cost Selling Price with 12% Profit Selling Price per kit Customer Cost per cup RM 38.86/500 RM 450.00 405.00 885.00 971.50 38.86 RM 0.078 The discount had been necessary to get this customer from a competitor. Unfortunately, the offering of the discount meant that this contract could not generate 15 per cent profit on sales. En. Solch was concerned that if his salespeople had to offer these discounts to get large outer business, and perhaps offer greater discounts to keep large order business, the Coffee Services Division of Soleh Kopi-O could end up failing to achieve the needed profit to remain viable and grow. Obviously, the existing pricing approach was not generating the results that were sought. Could it be possible that there was something wrong in the entire approach to costing and pricing in this industry? En. Soleh wondered what he might do to make his firm competitive and still earn the desired profit levels in this business. Exhibit 1 SOLEH KOPI-O COST STRUCTURE-FOR THE COFFEE SERVICE DIVISION Kits of Roasted Coffee (27,777 kits x RM 18.00) Personnel Costs This covered the cost of salaries for all personnel (8 people) Equipment Costs This covered the cost of coffee brewing equipment and maintenance on the equipment Vehicle Costs This covered the depreciation and operating costs of all division vehicles Other Overhead Costs This covered all other divisional expenses not included in the above categories Total Costs NOTE: These data have been disguised to preserve confidentiality RM 500,000 220,000 90,000 70,000 70,000 950,000 Required: Return on Sales Target Return on Sales (b) (c) Exhibit 2 INCOME STATEMENT FOR PREVIOUS YEAR FOR SOLEH KOPI-O COFFEE SERVICE DIVISION (d) Revenue Less: Cost of Goods Sold Gross Margin Less: Selling and Administration Net Profit 5% 15% RM 1,000,000 500.000 500,000 450.000 50,000 Briefly describe problems currently faced by Soleh Kopi-O. Then state the MAJOR issue in the case. Explain why you consider this to be major issue. Refer to En. Soleh's analysis of the two typical customers. In your opinion, what is the main problem with the existing costing and pricing approach used by En. Soleh? Explain. Recompute the computation for the two customers, to resolve the problem you stated in part (c) above, and to incorporate the desired profit 15% profit on sales. Explain the basis for your computations. Show the revised selling price with 15% profit, the price kit and the the customer cost per cup, for EACH customer (the small office complex in Ipoh and the restaurant in Penang) Compare your revised computations with the existing costing and pricing approach used by En. Soleh. Explain in what way your revised costing and pricing is better than En. Soleh's approach and will make Soleh Kopi-O more competitive. In your opinion, is it possible for the Coffee Services Division to generate the desired 15% profit margin? Why?

Expert Answer:

Answer rating: 100% (QA)

a Brief ly describe problems currently faced by Sole h Kop i O ANS WER S ole h Kop i O is currently facing several problems Firstly the profit margin of the Coffee Services Division is lower than the ... View the full answer

Related Book For

Federal Taxation 2016 Comprehensive

ISBN: 9780134104379

29th edition

Authors: Thomas R. Pope, Timothy J. Rupert, Kenneth E. Anderson

Posted Date:

Students also viewed these general management questions

-

Pedro Bourbone is the founder and owner of a highly successful small business and, over the past several years, has accumulated a significant amount of personal wealth. His port-folio of stocks and...

-

Pedro Bourbone is the founder and owner of a highly successful small business and, over the past several years, has accumulated a significant amount of personal wealth. His portfolio of stocks and...

-

Pedro Bourbone is the founder and owner of a highly successful small business and, over the past several years, has accumulated a significant amount of personal wealth. His portfolio of stocks and...

-

Hi, I need help with this accounting problem, thanks inadvance.l [The following information applies to the questions displayed below.] Delph Company uses a job-order costing system and has two...

-

Let X be the number of heads when a fair coin is flipped four times. a. Find the distribution of X and then use simulation to generate 1000 values of X. b. Is the simulated distribution indicative of...

-

Describe and explain the circular flow model. Scarcity, Trade-Offs, and Production Possibilities CHAPTER 3

-

What are inspirational leadership perspectives?

-

The following table summarizes the average annual return and the standard deviation of returns for several types of securities over the past 75 years. Assume annual returns in each case are...

-

**#15.) When is a rectangle a square? a) When diagonals are congruent b) When diagonals bisect each other c) When diagonals bisect angles d) When all four angles are right angles

-

Consider the calculation of the continuation value. Suppose Firm C has a WACC of 7%. Firm C's investment banker prepares a DCF valuation of Firm C using the WACC ap- proach. In her DCF valuation,...

-

Quiz Company provided the following information related to its two product lines Product 1 Product 2 10,000 20,000 Units sold Price per unit $20 $15 Variable cost per unit 10 12 Direct fixed costs...

-

By paying a student-athlete to endorse its brand or company, what value or benefit does the company receive? What are potential risks associated with entering into a NIL agreement with a student...

-

On April 1, 2024, La Salsa Corporation sold some equipment for $18,000. The original cost was $50,000, the estimated residual value was $8,000, and the expected useful life was six years. On December...

-

compare the process of managing an operating budget to that of managing a capital budget and identify knowledge gap

-

A proton is hovering above the center of a 2m wide circular table without moving. You discover the table surface has a total net charge of +50uC. How high above the table must the proton be located...

-

Eastport Inc. was organized on June 5, 2016. It was authorized to issue 300,000 shares of $10 par common stock and 50,000 shares of 5 percent cumulative class A preferred stock. The class A stock had...

-

Clonex Labs, Incorporated, uses the weighted-average method in its process costing system. The following data are available for one department for October Percent Completed Units Work in process,...

-

What services are provided by the provincial and territorial governments?

-

In the current year, Melissa, a single employee whose AGI is $100,000 before any of the items below, incurs the following expenses: Safe deposit box rental for investments .. $ 100 Tax return...

-

On March 1, 2015, Sarah entered into a three-year lease of an automobile used exclusively in her business. The automobiles FMV was $58,500 at the inception of the lease. Sarah made ten monthly lease...

-

Wicker Corporation made estimated tax payments of $6,000 in Year 1. On March 12 of Year 2, it filed its Year 1 tax return showing a $20,000 tax liability, and it paid the $14,000 balance at that...

-

Construct a combined common-size and common-base year balance sheet for 2007. What will be the common-base year value for the 2007 net fixed assets? a. 0.89 b. 0.92 c. 1.12 d. 1.32 AHS INC. 2007...

-

What will be the value of AHS' equity multiplier during 2007? a. 0.44 b. 0.56 c. 1.78 d. 1.82 AHS INC. 2007 Income Statement (S in millions) Net sales S 9625 Cost of goods sold 5225 Depreciation 1890...

-

What will be the value of AHS' current ratio during 2007? a. 1.14 b. 1.42 c. 1.49 d. 1.53 AHS INC. 2007 Income Statement (S in millions) Net sales S 9625 Cost of goods sold 5225 Depreciation 1890...

Study smarter with the SolutionInn App