Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

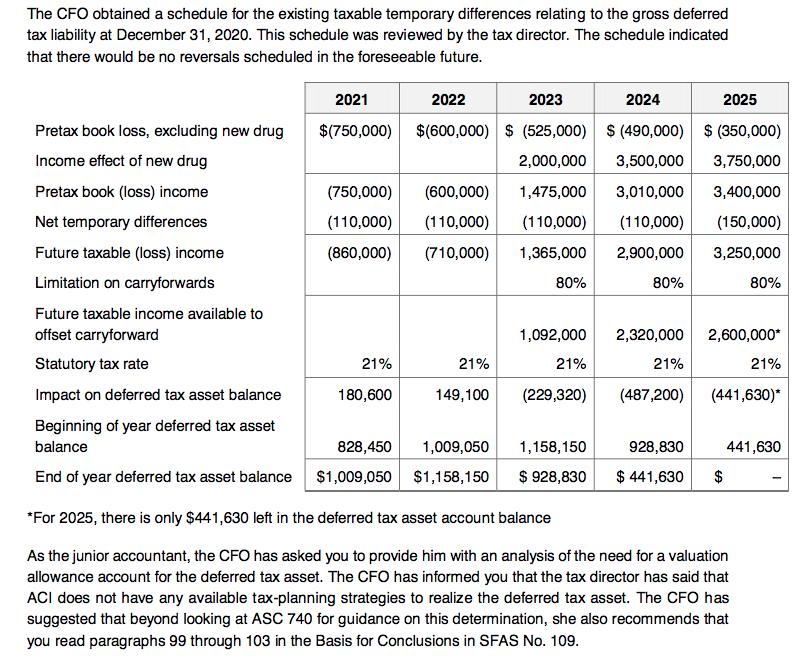

Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion? Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion?

Expert Answer:

Answer rating: 100% (QA)

Based on my analysis I recommend that the CFO should not establish a valuation allowance to offset the deferred tax asset balance because ACI is antic... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

Asbat Pharmaceuticals (Asbat) is a leading pharmaceutical company that has been in existence for 22 years. Asbat has a calendar year-end and is audited annually. Asbat only operates in the United...

-

The Company classifies its investments in both fixed income securities and publicly traded equity securities as available- for- sale investments. Fixed income securities primarily consist of U. S....

-

Lehman Brothers Holdings Inc. was originally founded in Montgomery, Alabama, in 1850 by three brothers. The company began as a small retailer that took cotton as payment for goods. The company...

-

Find the antiderivative for each function when C equals 0. a. f(x) = 1 7 b. g(x)== 11 +/- 150 is a. The antiderivative of 5 c. h(x)=4 -- X Part 1 of 3

-

Justin Swords started a small merchandising business in 2013. The business experienced the following events during its first year of operation. Assume that Swords uses the perpetual inventory system....

-

Explain why the following alkyl halide does not undergo a substitution reaction, regardless of the conditions under which the reaction is run: Cl

-

For the following data set: a. Construct the multiple regression equation b. Predict the value of y when x1 = 5.2, x2 = 9.1, x3 = 8.7, x4 = 2.8. c. What percentage of the variation in y is explained...

-

Webster ordered a bowl of fish chowder at the Blue Ship Tea Room. She was injured by a fish bone in the chowder, and she sued the tea room for breach of the implied warranty of merchantability. The...

-

Mike's Place has total assets of $123,800, a debt-equity ratio of 0.7, and net income of $8,100. What is the return on equity? (4 pts) T/A= $123,800.00 D/E ratio= 0.7 NI= $8,100.00 ROE= 11.12%

-

Western Environmental Inc. Comparative Balance Sheet Information Cash Accounts receivable (net) Inventory Prepaid expenses Equipment Accumulated depreciation. Accounts payable Nages payable Income...

-

As Superintendent Field, how can you align the strategic objectives of the National Park Service with the redevelopment of Caneel Bay? Given the mission of the National Park Service, which...

-

How does the auditor use regression analysis?

-

Describe five transactions or events that may create substantial doubt as to the ability of an entity to continue as a going concern.

-

List six pairs of accounts on which audit work is often performed simultaneously.

-

Differentiate among known, projected, and likely misstatements.

-

Explain the review process for audit working papers.

-

Present Value, Future Value, and Discounting Cash Flow. Question 1 of 6 If the PV of $139 is $125, what is the discount factor? Select the correct response: 11.2 10.5 13.0 3.25 12.1 1.36 9.9 Present...

-

Find the radius of convergence in two ways: (a) Directly by the CauchyHadamard formula in Sec. 15.2. (b) From a series of simpler terms by using Theorem 3 or Theorem 4.

-

Canadian National Railway Company (CN) spans Canada and mid-America and provides freight transport services from the Atlantic Ocean to the Pacific Ocean and to the Gulf of Mexico. It is currently the...

-

Using the following key, identify the effects of the following transactions or conditions on the various financial statement elements: I = increases; D = decreases; NE = no effect. Note that the...

-

Massachusetts Stove Company manufactures wood-burning stoves for the heating of homes and businesses. The company has approached you, as chief lending officer for the Massachusetts Regional Bank,...

-

The cable is subjected to the uniform loading. Determine the equation \(y=f(x)\) which defines the cable shape \(A B\) and the maximum tension in the cable.. 50 ft 50 ft |- B 150 lb/ft 20 ft x

-

The beams \(A B\) and \(B C\) are supported by the cable that has a parabolic shape. Draw the shear and moment diagrams for members \(A B\) and \(B C\). The hanger at \(B\) is attached to member \(A...

-

The cable has a mass of \(0.5 \mathrm{~kg} / \mathrm{m}\) and is \(25 \mathrm{~m}\) long. Determine the vertical and horizontal components of force it exerts on the top of the tower. B 30 15 m

Study smarter with the SolutionInn App