Assume that items 1 through 8 are situations that Jones, CPA, has encountered during his audit...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

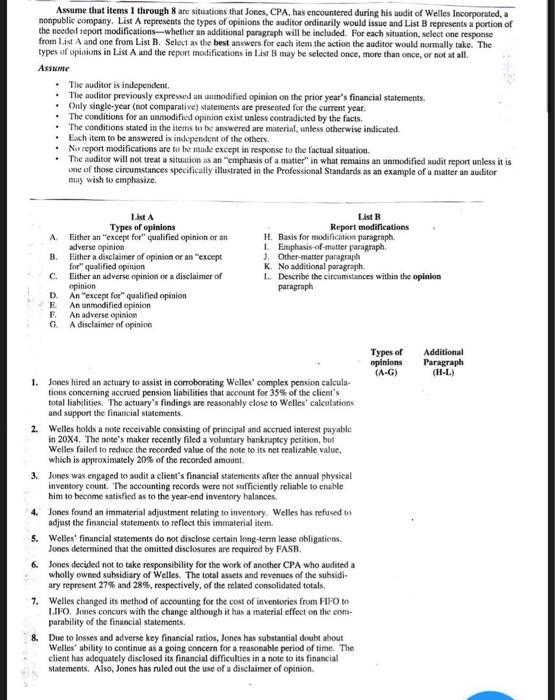

Assume that items 1 through 8 are situations that Jones, CPA, has encountered during his audit of Welles Incorporated, a nonpublic company. List A represents the types of opinions the auditor ordinarily would issue and List B represents a portion of the needed report modifications-whether an additional paragraph will be included. For each situation, select one response from List A and one from List B. Select as the best answers for each item the action the auditor would normally take. The types of opinions in List A and the report modifications in List B may be selected once, more than once, or not at all. Assume . The auditor is independent. • The auditor previously expressed an unmodified opinion on the prior year's financial statements. • Only single-year (not comparative) statements are presented for the current year. . The conditions for an unmodified opinion exist unless contradicted by the facts. The conditions stated in the items to be answered are material, unless otherwise indicated. • Each item to be answered is independent of the others. No report modifications are to be made except in response to the factual situation. • The auditor will not treat a situation as an "emphasis of a matter" in what remains an unmodified audit report unless it is one of those circumstances specifically illustrated in the Professional Standards as an example of a matter an auditor may wish to emphasize. A B. 6 C. D E F. G. List A Types of opinions Either an "except for" qualified opinion or an adverse opinion Either a disclaimer of opinion or an "except for" qualified opinion Either an adverse opinion or a disclaimer of opinion An "except for qualified opinion An unmodified opinion An adverse opinion A disclaimer of opinion List B Report modifications H. Basis for modification paragraph. I. Emphasis-of-mutter paragraph. J. Other-matter paragraph K. No additional paragraph. L.. Describe the circumstances within the opinion paragraph 1. Jones hired an actuary to assist in corroborating Welles' complex pension calcula- tions concerning accrued pension liabilities that account for 35% of the client's total liabilities. The actuary's findings are reasonably close to Welles' calculations and support the financial statements. 2. Welles holds a note receivable consisting of principal and accrued interest payable in 20X4. The note's maker recently filed a voluntary bankruptcy petition, but Welles failed to reduce the recorded value of the note to its net realizable value, which is approximately 20% of the recorded amount. 3. Jones was engaged to audit a client's financial statements after the annual physical inventory count. The accounting records were not sufficiently reliable to enable him to become satisfied as to the year-end inventory balances. 4. Jones found an immaterial adjustment relating to inventory. Welles has refused to adjust the financial statements to reflect this immaterial item. 5. Welles financial statements do not disclose certain long-term lease obligations. Jones determined that the omitted disclosures are required by FASB. 6. Jones decided not to take responsibility for the work of another CPA who audited a wholly owned subsidiary of Welles. The total assets and revenues of the subsidi- ary represent 27% and 28%, respectively, of the related consolidated totals. 7. Welles changed its method of accounting for the cost of inventories from FIFO to LIFO. Jones concurs with the change although it has a material effect on the com- parability of the financial statements. Due to losses and adverse key financial ratios, Jones has substantial doubt about Welles' ability to continue as a going concern for a reasonable period of time. The client has adequately disclosed its financial difficulties in a note to its financial statements. Also, Jones has ruled out the use of a disclaimer of opinion. Types of opinions (A-G) Additional Paragraph (H-L) Assume that items 1 through 8 are situations that Jones, CPA, has encountered during his audit of Welles Incorporated, a nonpublic company. List A represents the types of opinions the auditor ordinarily would issue and List B represents a portion of the needed report modifications-whether an additional paragraph will be included. For each situation, select one response from List A and one from List B. Select as the best answers for each item the action the auditor would normally take. The types of opinions in List A and the report modifications in List B may be selected once, more than once, or not at all. Assume . The auditor is independent. • The auditor previously expressed an unmodified opinion on the prior year's financial statements. • Only single-year (not comparative) statements are presented for the current year. . The conditions for an unmodified opinion exist unless contradicted by the facts. The conditions stated in the items to be answered are material, unless otherwise indicated. • Each item to be answered is independent of the others. No report modifications are to be made except in response to the factual situation. • The auditor will not treat a situation as an "emphasis of a matter" in what remains an unmodified audit report unless it is one of those circumstances specifically illustrated in the Professional Standards as an example of a matter an auditor may wish to emphasize. A B. 6 C. D E F. G. List A Types of opinions Either an "except for" qualified opinion or an adverse opinion Either a disclaimer of opinion or an "except for" qualified opinion Either an adverse opinion or a disclaimer of opinion An "except for qualified opinion An unmodified opinion An adverse opinion A disclaimer of opinion List B Report modifications H. Basis for modification paragraph. I. Emphasis-of-mutter paragraph. J. Other-matter paragraph K. No additional paragraph. L.. Describe the circumstances within the opinion paragraph 1. Jones hired an actuary to assist in corroborating Welles' complex pension calcula- tions concerning accrued pension liabilities that account for 35% of the client's total liabilities. The actuary's findings are reasonably close to Welles' calculations and support the financial statements. 2. Welles holds a note receivable consisting of principal and accrued interest payable in 20X4. The note's maker recently filed a voluntary bankruptcy petition, but Welles failed to reduce the recorded value of the note to its net realizable value, which is approximately 20% of the recorded amount. 3. Jones was engaged to audit a client's financial statements after the annual physical inventory count. The accounting records were not sufficiently reliable to enable him to become satisfied as to the year-end inventory balances. 4. Jones found an immaterial adjustment relating to inventory. Welles has refused to adjust the financial statements to reflect this immaterial item. 5. Welles financial statements do not disclose certain long-term lease obligations. Jones determined that the omitted disclosures are required by FASB. 6. Jones decided not to take responsibility for the work of another CPA who audited a wholly owned subsidiary of Welles. The total assets and revenues of the subsidi- ary represent 27% and 28%, respectively, of the related consolidated totals. 7. Welles changed its method of accounting for the cost of inventories from FIFO to LIFO. Jones concurs with the change although it has a material effect on the com- parability of the financial statements. Due to losses and adverse key financial ratios, Jones has substantial doubt about Welles' ability to continue as a going concern for a reasonable period of time. The client has adequately disclosed its financial difficulties in a note to its financial statements. Also, Jones has ruled out the use of a disclaimer of opinion. Types of opinions (A-G) Additional Paragraph (H-L)

Expert Answer:

Answer rating: 100% (QA)

Answer 1When an auditor recruits an expert to help with authenticating a customer gauge here complex benefits estimations furthermore that experts discoveries are sensibly near those of the customer n... View the full answer

Related Book For

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

Posted Date:

Students also viewed these accounting questions

-

Complete problem below. List a represents the types of opinions the auditor ordinarily would issue and List B represents the report modifications [if any] that would be necessary. Select as the best...

-

Items 1 through 8 are selected questions typically found in internal control questionnaires used by auditors to obtain an understanding of internal control in the payroll and personnel cycle. In...

-

Items 1 through 8 are selected questions typically found in questionnaires used by auditors to obtain an understanding of internal control in the inventory and warehousing cycle. In using the...

-

Necked Amber purchased a bond for $1,038.90 exactly two years ago. At that time, the bond had a maturity of five years and a coupon rate of 10% (paid semi-annually). Assuming the rates below are the...

-

Use the following ratio information for Johnson International and the industry averages for Johnson's line of business to: a. Construct the DuPont system of analysis for both Johnson and the...

-

In Problem, graph each inequality subject to the non negative restrictions. 24x + 30y > 7,200, x 0, y 0

-

Classifying Internal Control Procedures \section*{Required:} Match each of the control procedures listed below with the most closely related control procedures type. Your answer should pair each of...

-

Steve Madison needs $250,000 in 10 years. How much must he invest at the end of each year, at 11% interest, to meet his needs?

-

The following accounts are taken from the financial statements of Paradise Tropical Resorts at June 3 0 , 2 0 1 9 . ( Amounts are in millions. ) Accounts Payable $ 1 , 5 4 0 Accounts Receivable 3 4 0...

-

Imagine that Howard has asked you to write some queries to help him make better use of his data. For each information request below, write a single query that provides the answer set. When a task...

-

Cabral SA is authorized to issue 1 , 0 0 0 , 0 0 0 , $ 5 par value ordinary shares. It also It is authorized to issue 2 0 , 0 0 0 , $ 5 0 par value preference shares. In its first year, the company...

-

Windows and macOS both include a number of features and utilities designed for users with special needs. Compare the offerings of an OS. Can you think of any areas that have not been addressed by...

-

A. Explain how risk and interest rates on a loan are related

-

An initial deposit of $10,000 into investment account earning annual compound interest of 10.5% will grow to how much over 25 years

-

The general ledger of Vance Corporation as of December 31, includes the following accounts: Copyrights Deposits with advertising agency (will be used to promote goodwill) Discount on bonds payable...

-

Lori is a new hire and is keen to show her prowess in delta hedging to her boss. She reviews the put options on Waste Connections Ltd. and sells 60,000 put options. Spot price on the date of trading...

-

What are the characteristics or elements of professional business communication? Rank the top three characteristics and explain the criteria for the ranking. Explain why the first characteristic is mo

-

Use Stokes' Theorem to evaluate f(y+sin x) dx+(z+cos y) dy+rdz, where C is the rve r(t) = (sint, cost, sin 2t), t = [0, 2].

-

Multiple Choice Questions The following questions concern the use of analytical procedures during an audit. Select the best response. a. Analytical procedures used in planning an audit should focus...

-

Distinguish between the following payroll audit procedures and state the purpose of each: (1) Trace a random sample of prenumbered time cards to the related payments in the payroll register and...

-

The use of audit software has increased dramatically in recent years. Software is now used to fulfill administrative functions in the audit environment, document audit work, and conduct data...

-

Changes in sales price and variable costs (Learning Objective 3)} Use the information from the Bay Cruiseline Data Set. 1. Suppose Bay Cruiseline cuts its dinner cruise ticket price from \(\$ 60\) to...

-

Prepare a CVP graph (Learning Objective 2)} Use the information from the Bay Cruiseline Data Set. Draw a graph of Bay Cruiseline's CVP relationships. Include the sales revenue line, the fixed expense...

-

Interpret a CVP graph (Learning Objective 2)} Describe what each letter stands for in the CVP graph. D 300 200 F C G 150 H B A E The breakeven point is atunits and at J. dollars of sales.

Study smarter with the SolutionInn App