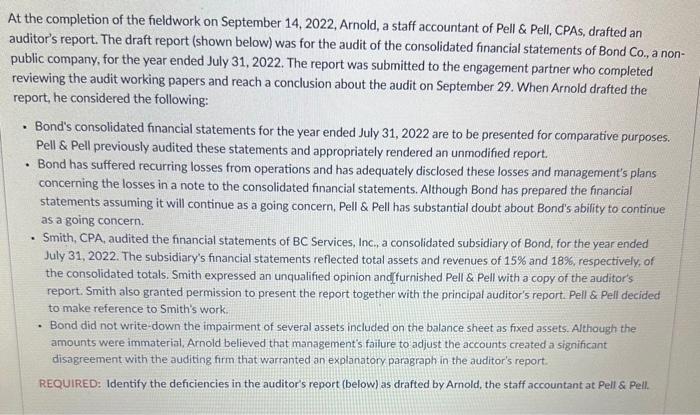

At the completion of the fieldwork on September 14, 2022, Arnold, a staff accountant of Pell...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

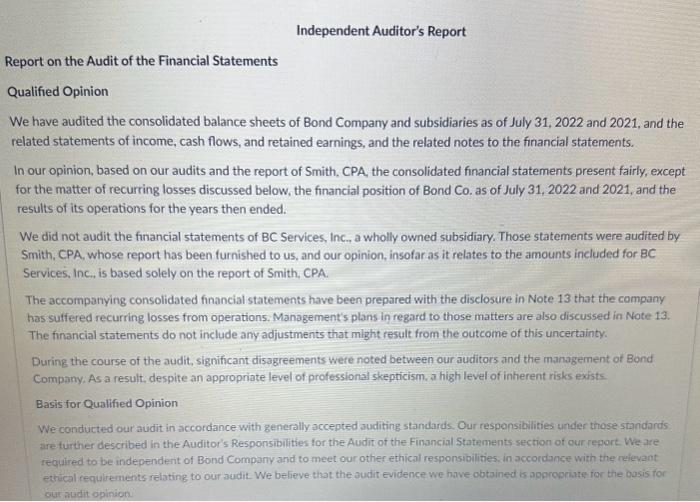

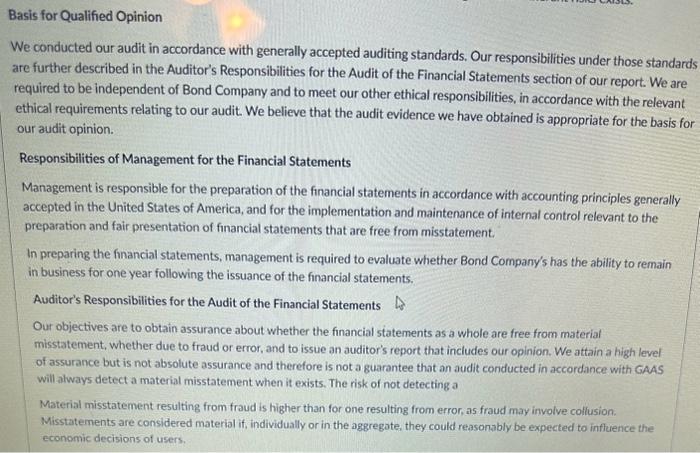

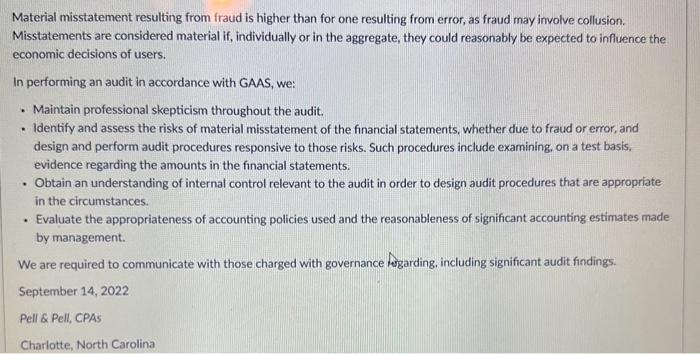

At the completion of the fieldwork on September 14, 2022, Arnold, a staff accountant of Pell & Pell, CPAS, drafted an auditor's report. The draft report (shown below) was for the audit of the consolidated financial statements of Bond Co., a non- public company, for the year ended July 31, 2022. The report was submitted to the engagement partner who completed reviewing the audit working papers and reach a conclusion about the audit on September 29. When Arnold drafted the report, he considered the following: • Bond's consolidated financial statements for the year ended July 31, 2022 are to be presented for comparative purposes. Pell & Pell previously audited these statements and appropriately rendered an unmodified report. • Bond has suffered recurring losses from operations and has adequately disclosed these losses and management's plans concerning the losses in a note to the consolidated financial statements. Although Bond has prepared the financial statements assuming it will continue as a going concern, Pell & Pell has substantial doubt about Bond's ability to continue as a going concern. Smith, CPA, audited the financial statements of BC Services, Inc., a consolidated subsidiary of Bond, for the year ended July 31, 2022. The subsidiary's financial statements reflected total assets and revenues of 15% and 18%, respectively, of the consolidated totals. Smith expressed an unqualified opinion and furnished Pell & Pell with a copy of the auditor's report. Smith also granted permission to present the report together with the principal auditor's report. Pell & Pell decided to make reference to Smith's work. • Bond did not write-down the impairment of several assets included on the balance sheet as fixed assets. Although the amounts were immaterial, Arnold believed that management's failure to adjust the accounts created a significant disagreement with the auditing firm that warranted an explanatory paragraph in the auditor's report. REQUIRED: Identify the deficiencies in the auditor's report (below) as drafted by Arnold, the staff accountant at Pell & Pell. Independent Auditor's Report Report on the Audit of the Financial Statements Qualified Opinion We have audited the consolidated balance sheets of Bond Company and subsidiaries as of July 31, 2022 and 2021, and the related statements of income, cash flows, and retained earnings, and the related notes to the financial statements. In our opinion, based on our audits and the report of Smith, CPA, the consolidated financial statements present fairly, except for the matter of recurring losses discussed below, the financial position of Bond Co. as of July 31, 2022 and 2021, and the results of its operations for the years then ended. We did not audit the financial statements of BC Services, Inc., a wholly owned subsidiary. Those statements were audited by Smith, CPA, whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for BC Services, Inc., is based solely on the report of Smith, CPA. The accompanying consolidated financial statements have been prepared with the disclosure in Note 13 that the company has suffered recurring losses from operations. Management's plans in regard to those matters are also discussed in Note 13. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. During the course of the audit, significant disagreements were noted between our auditors and the management of Bond Company. As a result, despite an appropriate level of professional skepticism, a high level of inherent risks exists. Basis for Qualified Opinion We conducted our audit in accordance with generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Bond Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is appropriate for the basis for our audit opinion. Basis for Qualified Opinion We conducted our audit in accordance with generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Bond Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is appropriate for the basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from misstatement. In preparing the financial statements, management is required to evaluate whether Bond Company's has the ability to remain in business for one year following the issuance of the financial statements. Auditor's Responsibilities for the Audit of the Financial Statements Our objectives are to obtain assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. We attain a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a Material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion. Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users. Material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion. Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users. In performing an audit in accordance with GAAS, we: . Maintain professional skepticism throughout the audit. Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts in the financial statements. • Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances. . • Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management. We are required to communicate with those charged with governance garding, including significant audit findings. September 14, 2022 Pell & Pell, CPAS Charlotte, North Carolina . At the completion of the fieldwork on September 14, 2022, Arnold, a staff accountant of Pell & Pell, CPAS, drafted an auditor's report. The draft report (shown below) was for the audit of the consolidated financial statements of Bond Co., a non- public company, for the year ended July 31, 2022. The report was submitted to the engagement partner who completed reviewing the audit working papers and reach a conclusion about the audit on September 29. When Arnold drafted the report, he considered the following: • Bond's consolidated financial statements for the year ended July 31, 2022 are to be presented for comparative purposes. Pell & Pell previously audited these statements and appropriately rendered an unmodified report. • Bond has suffered recurring losses from operations and has adequately disclosed these losses and management's plans concerning the losses in a note to the consolidated financial statements. Although Bond has prepared the financial statements assuming it will continue as a going concern, Pell & Pell has substantial doubt about Bond's ability to continue as a going concern. Smith, CPA, audited the financial statements of BC Services, Inc., a consolidated subsidiary of Bond, for the year ended July 31, 2022. The subsidiary's financial statements reflected total assets and revenues of 15% and 18%, respectively, of the consolidated totals. Smith expressed an unqualified opinion and furnished Pell & Pell with a copy of the auditor's report. Smith also granted permission to present the report together with the principal auditor's report. Pell & Pell decided to make reference to Smith's work. • Bond did not write-down the impairment of several assets included on the balance sheet as fixed assets. Although the amounts were immaterial, Arnold believed that management's failure to adjust the accounts created a significant disagreement with the auditing firm that warranted an explanatory paragraph in the auditor's report. REQUIRED: Identify the deficiencies in the auditor's report (below) as drafted by Arnold, the staff accountant at Pell & Pell. Independent Auditor's Report Report on the Audit of the Financial Statements Qualified Opinion We have audited the consolidated balance sheets of Bond Company and subsidiaries as of July 31, 2022 and 2021, and the related statements of income, cash flows, and retained earnings, and the related notes to the financial statements. In our opinion, based on our audits and the report of Smith, CPA, the consolidated financial statements present fairly, except for the matter of recurring losses discussed below, the financial position of Bond Co. as of July 31, 2022 and 2021, and the results of its operations for the years then ended. We did not audit the financial statements of BC Services, Inc., a wholly owned subsidiary. Those statements were audited by Smith, CPA, whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for BC Services, Inc., is based solely on the report of Smith, CPA. The accompanying consolidated financial statements have been prepared with the disclosure in Note 13 that the company has suffered recurring losses from operations. Management's plans in regard to those matters are also discussed in Note 13. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. During the course of the audit, significant disagreements were noted between our auditors and the management of Bond Company. As a result, despite an appropriate level of professional skepticism, a high level of inherent risks exists. Basis for Qualified Opinion We conducted our audit in accordance with generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Bond Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is appropriate for the basis for our audit opinion. Basis for Qualified Opinion We conducted our audit in accordance with generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Bond Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is appropriate for the basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from misstatement. In preparing the financial statements, management is required to evaluate whether Bond Company's has the ability to remain in business for one year following the issuance of the financial statements. Auditor's Responsibilities for the Audit of the Financial Statements Our objectives are to obtain assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. We attain a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a Material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion. Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users. Material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion. Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users. In performing an audit in accordance with GAAS, we: . Maintain professional skepticism throughout the audit. Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts in the financial statements. • Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances. . • Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management. We are required to communicate with those charged with governance garding, including significant audit findings. September 14, 2022 Pell & Pell, CPAS Charlotte, North Carolina .

Expert Answer:

Related Book For

Auditing and Assurance Services A Systematic Approach

ISBN: 978-0077732509

10th edition

Authors: William Messier Jr, Steven Glover, Douglas Prawitt

Posted Date:

Students also viewed these accounting questions

-

The following auditor's report was drafted by a staff accountant of Turner & Turner, CPAs, at the completion of the audit of the financial statements of Lyon Computers, Inc. (a nonpublic company) for...

-

The following auditors report was drafted by a staff accountant of Turner & Turner, CPAs, at the completion of the audit of the financial statements of Lyon Computers, Inc. (a non-public company) for...

-

(a) Why is the MD&A section of the annual report useful to the financial analyst? What types of information can be found in this section? (b) Using the excerpts from the MD&A of the Biolase,...

-

The payroll summary for EVB Inc. for the period August 3 - 10 is as follows: Factory Employees Sales and Admin. Employees Total Gross Earnings $80,000 $25,000 $105,000 Withholding and deductions:...

-

Modify your algorithm from Exercise 24.3-6 to run in O ((V + E) lg W ) time. (Hint: How many distinct shortest-path estimates can there be in V - S at any point in time?)

-

Why and how must marketers use fear appeals in advertising cautiously?

-

Popsi Corporation's current ratio is 0.5, while Cake Company's current ratio is 1.5. Both firms want to "window dress" their coming end-of-year financial statements. As part of their window dressing...

-

Techtra makes electronic components used by other firms in a wide variety of end products. Initially the firm bid for any type of electronic assembly work that became available (mostly subcontract...

-

Evaluate the function for the given value. 5x g(x)=e, x=-1 g(-1)= (Type an integer or a decimal. Round to the nearest thousandth as nee

-

Consolidation Eliminating Entries, First Year Packer Corporation buys 85 percent of the voting stock of Slattery Inc. on January 1, 2023, at an acquisition cost of $10,000,000. The fair value of the...

-

A defendant, a Hispanic 22-year-old man, was persuaded by his public defender to plead guilty to possession of marijuana to avoid a greater offense of possession with intent to distribute, even...

-

What is the title of the general ledger account used to summarize the total amount due from all charge customers?

-

What is the advantage of having special amount columns in a journal?

-

For what are special amount columns in a journal used?

-

Vincente Burgos states that his business is so small that he just records supplies and insurance as expenses when he pays for them. Thus, at the end of a fiscal period, Mr. Burgos does not record...

-

Gretel Bakken forgot to journalize and post the adjusting entry for prepaid insurance at the end of the June fiscal period. What effect will this omission have on the records of Ms. Bakkens business...

-

Allowance for Doubtful Accounts has a credit balance of $788 at the end of the year (before adjustment), and an analysis of accounts in the customers ledger indicates that the estimated amount of...

-

Consider a game of poker being played with a standard 52-card deck (four suits, each of which has 13 different denominations of cards). At a certain point in the game, six cards have been exposed. Of...

-

The "Accounts Receivable-Confirmation Statistics" working paper shown on the next page was prepared by an audit assistant for the 2015 audit of Lewis County Water Company, Inc., a continuing audit...

-

In 2015 Kida Company purchased more than $10 million worth of office equipment under its "special" ordering system, with individual orders ranging from $5,000 to $30,000. "Special" orders entail...

-

At December 31, 2015, EarthWear has $5,890,000 in a liability account labeled "Reserve for returns." The footnotes to the financial statements contain the following policy: "At the time of sale, the...

-

What difference has the introduction of a comprehensive income statement made to U.S. accounting for foreign exchange?

-

Why do you think it has been so difficult for accounting regulators to deal with accounting for foreign exchange over the last twenty-five years?

-

Choose a country and prepare a report on its foreign exchange risk. How do you think accountants should deal with this?

Study smarter with the SolutionInn App