Before your firm accepts any additional ongoing engagement, for example new audits, the partners meet to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

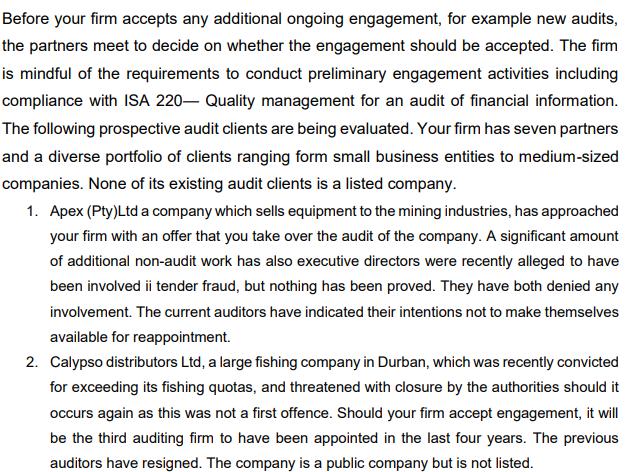

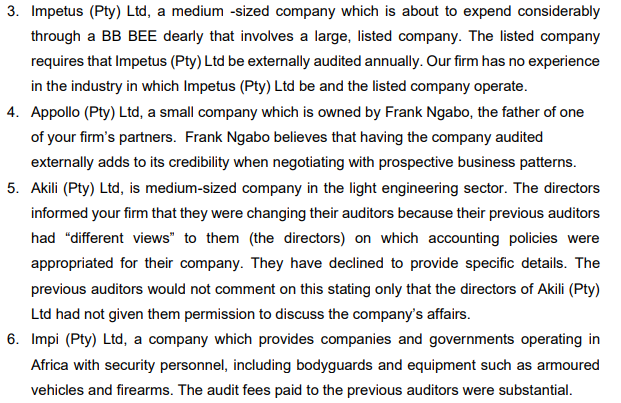

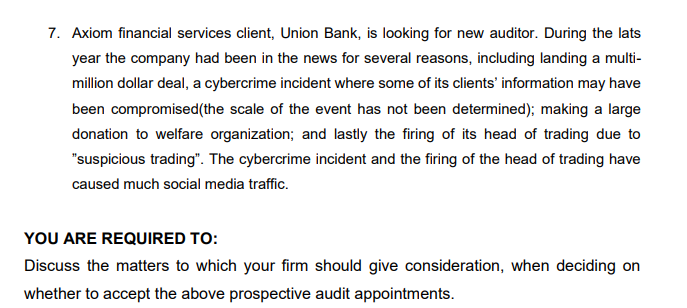

Before your firm accepts any additional ongoing engagement, for example new audits, the partners meet to decide on whether the engagement should be accepted. The firm is mindful of the requirements to conduct preliminary engagement activities including compliance with ISA 220- Quality management for an audit of financial information. The following prospective audit clients are being evaluated. Your firm has seven partners and a diverse portfolio of clients ranging form small business entities to medium-sized companies. None of its existing audit clients is a listed company. 1. Apex (Pty) Ltd a company which sells equipment to the mining industries, has approached your firm with an offer that you take over the audit of the company. A significant amount of additional non-audit work has also executive directors were recently alleged to have been involved ii tender fraud, but nothing has been proved. They have both denied any involvement. The current auditors have indicated their intentions not to make themselves available for reappointment. 2. Calypso distributors Ltd, a large fishing company in Durban, which was recently convicted for exceeding its fishing quotas, and threatened with closure by the authorities should it occurs again as this was not a first offence. Should your firm accept engagement, it will be the third auditing firm to have been appointed in the last four years. The previous auditors have resigned. The company is a public company but is not listed. 3. Impetus (Pty) Ltd, a medium -sized company which is about to expend considerably through a BB BEE dearly that involves a large, listed company. The listed company requires that Impetus (Pty) Ltd be externally audited annually. Our firm has no experience in the industry in which Impetus (Pty) Ltd be and the listed company operate. 4. Appollo (Pty) Ltd, a small company which is owned by Frank Ngabo, the father of one of your firm's partners. Frank Ngabo believes that having the company audited externally adds to its credibility when negotiating with prospective business patterns. 5. Akili (Pty) Ltd, is medium-sized company in the light engineering sector. The directors informed your firm that they were changing their auditors because their previous auditors had "different views" to them (the directors) on which accounting policies were appropriated for their company. They have declined to provide specific details. The previous auditors would not comment on this stating only that the directors of Akili (Pty) Ltd had not given them permission to discuss the company's affairs. 6. Impi (Pty) Ltd, a company which provides companies and governments operating in Africa with security personnel, including bodyguards and equipment such as armoured vehicles and firearms. The audit fees paid to the previous auditors were substantial. 7. Axiom financial services client, Union Bank, is looking for new auditor. During the lats year the company had been in the news for several reasons, including landing a multi- million dollar deal, a cybercrime incident where some of its clients' information may have been compromised (the scale of the event has not been determined); making a large donation to welfare organization; and lastly the firing of its head of trading due to "suspicious trading". The cybercrime incident and the firing of the head of trading have caused much social media traffic. YOU ARE REQUIRED TO: Discuss the matters to which your firm should give consideration, when deciding on whether to accept the above prospective audit appointments. Before your firm accepts any additional ongoing engagement, for example new audits, the partners meet to decide on whether the engagement should be accepted. The firm is mindful of the requirements to conduct preliminary engagement activities including compliance with ISA 220- Quality management for an audit of financial information. The following prospective audit clients are being evaluated. Your firm has seven partners and a diverse portfolio of clients ranging form small business entities to medium-sized companies. None of its existing audit clients is a listed company. 1. Apex (Pty) Ltd a company which sells equipment to the mining industries, has approached your firm with an offer that you take over the audit of the company. A significant amount of additional non-audit work has also executive directors were recently alleged to have been involved ii tender fraud, but nothing has been proved. They have both denied any involvement. The current auditors have indicated their intentions not to make themselves available for reappointment. 2. Calypso distributors Ltd, a large fishing company in Durban, which was recently convicted for exceeding its fishing quotas, and threatened with closure by the authorities should it occurs again as this was not a first offence. Should your firm accept engagement, it will be the third auditing firm to have been appointed in the last four years. The previous auditors have resigned. The company is a public company but is not listed. 3. Impetus (Pty) Ltd, a medium -sized company which is about to expend considerably through a BB BEE dearly that involves a large, listed company. The listed company requires that Impetus (Pty) Ltd be externally audited annually. Our firm has no experience in the industry in which Impetus (Pty) Ltd be and the listed company operate. 4. Appollo (Pty) Ltd, a small company which is owned by Frank Ngabo, the father of one of your firm's partners. Frank Ngabo believes that having the company audited externally adds to its credibility when negotiating with prospective business patterns. 5. Akili (Pty) Ltd, is medium-sized company in the light engineering sector. The directors informed your firm that they were changing their auditors because their previous auditors had "different views" to them (the directors) on which accounting policies were appropriated for their company. They have declined to provide specific details. The previous auditors would not comment on this stating only that the directors of Akili (Pty) Ltd had not given them permission to discuss the company's affairs. 6. Impi (Pty) Ltd, a company which provides companies and governments operating in Africa with security personnel, including bodyguards and equipment such as armoured vehicles and firearms. The audit fees paid to the previous auditors were substantial. 7. Axiom financial services client, Union Bank, is looking for new auditor. During the lats year the company had been in the news for several reasons, including landing a multi- million dollar deal, a cybercrime incident where some of its clients' information may have been compromised (the scale of the event has not been determined); making a large donation to welfare organization; and lastly the firing of its head of trading due to "suspicious trading". The cybercrime incident and the firing of the head of trading have caused much social media traffic. YOU ARE REQUIRED TO: Discuss the matters to which your firm should give consideration, when deciding on whether to accept the above prospective audit appointments.

Expert Answer:

Answer rating: 100% (QA)

When deciding whether to accept prospective audit appointments the firm should consider several important factors and matters for each of the cases pr... View the full answer

Related Book For

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

Posted Date:

Students also viewed these accounting questions

-

7 . Pink, Inc. had Bonds Payable of $ 8 0 , 0 0 0 as of April 1 7 , 2 0 1 5 . Their Premium on Bonds Payable account had a credit balance of $ 1 3 , 0 0 0 . If they retire the bonds for $ 7 5 , 0 0 0...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

On April 29, 2016, Auk Corporation acquires 100% of the outstanding stock of Amazon Corporation (E & P of $750,000) for $1.2 million. Amazon Corporation has assets with a fair market value of $1.4...

-

Data for Green Lawn Care Ltd. were presented in E3-1. 1. Issued common shares to shareholders in exchange for cash. 2. Paid monthly rent. 3. Purchased equipment on account. 4. Billed customers for...

-

Write down the time evolution equation for Heisenberg operators, calculating explicitly the evolution Hamiltonian, in the case of a free particle, and then calculate explicit expressions for...

-

Forensic accounting also may be known by another phrase, as indicated by the second forensic book published. What is the phrase and who published the book?

-

Starz Department Store is located near the Towne Shopping Mall. At the end of the company's calendar year on December 31, 2014, the following accounts appeared in two of its trial balances....

-

Paymore Products places orders for goods equal to 75% of its sales forecast in the next quarter. The sales forecasts for the next five quarters are as follows: Quarter in Coming Year Sales forecast...

-

NORDIC LIMITED: WORKING CAPITAL AND CAPITAL BUDGETING Nordic Limited commenced operations on 0 1 January 2 0 2 3 . Its mission was to provide an innovative product whilst ensuring creative customer...

-

On June 1, Huntley Company borrows $50,000 from the bank by signing a 60-day, 6%, interest-bearing note. Instructions: Prepare the necessary entries below associated with the note payable on the...

-

Explain how an auditor could perform a transaction walk-through for purchases and cash disbursements.

-

What incentives does an auditor have to assure that the timing and amount of discretionary write-downs for impaired assets is fairly presented in all material respects?

-

For which of the following portfolios are unrealized gains and losses not recognized? a. Trading securities. b. Call options. c. Available-for-sale securities. d. Held-to-maturity securities. Choose...

-

Which of the following control procedures is most likely to prevent or detect errors or frauds resulting from the production of unauthorized products or unauthorized quantities of authorized...

-

Why do auditors not usually rely on substantive tests alone when auditing accounts payable that result from credit purchase transactions?

-

You own a stock portfolio invested 25 percent in Stock Q, 20 percent in Stock R, 5 percent in Stock S, and 50 percent in Stock T. The betas for these four stocks are 1.34, 0.5, 1.17, and 1.47,...

-

What is a content filter? Where is it placed in the network to gain the best result for the organization?

-

Explain the relationships among the initial assessed control risk, tests of controls and substantive tests of transactions for cash disbursements, and the tests of details of cash balances. Give one...

-

Rank the following types of tests from most costly to least costly: analytical procedures, tests of details of balances, risk assessment procedures, tests of controls and substantive tests of...

-

For each engagement described below, indicate whether the engagement is likely to be conducted under international auditing standards, U.S. generally accepted auditing standards, or PCAOB auditing...

-

\((4+3) \times 2\) Perform the indicated calculation.

-

\(45 \div 15 \times 6+7^{2}-4 \times 15 \times 18 \div 12 \times 3\) Perform the indicated calculation.

-

\(10 \times 6^{3} \div 2 \times 5+3^{2}-240 \div 8 \times 9\) Perform the indicated calculation.

Study smarter with the SolutionInn App