Answered step by step

Verified Expert Solution

Question

1 Approved Answer

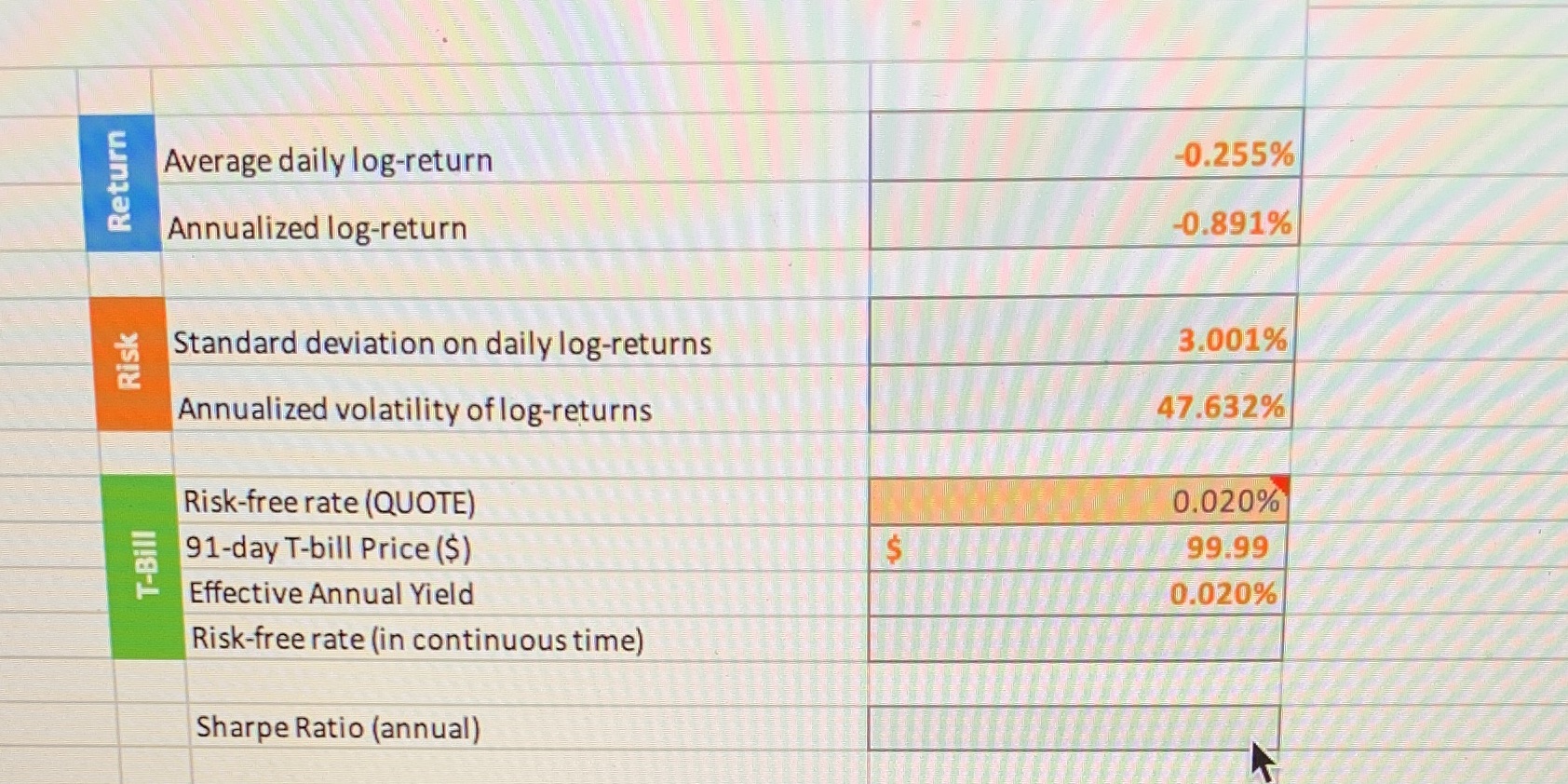

Calculate:A) Risk-Free rate (In continuous time)B) Sharpe Ratio (annual)Notes: 72 days of maturity. Average daily log-return Annualized log-return Standard deviation on daily log-returns Annualized volatility

Calculate:A) Risk-Free rate (In continuous time)B) Sharpe Ratio (annual)Notes: 72 days of maturity.

Average daily log-return Annualized log-return Standard deviation on daily log-returns Annualized volatility of log-returns T-Bill Risk Return -0.255% -0.891% 3.001% 47.632% Risk-free rate (QUOTE) 0.020% 91-day T-bill Price ($) $ 99.99 Effective Annual Yield 0.020% Risk-free rate (in continuous time) Sharpe Ratio (annual)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Core Principles and Applications

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

5th edition

1259289907, 978-1259289903