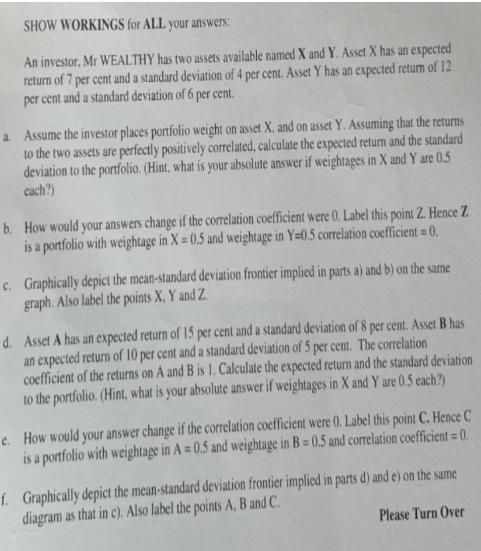

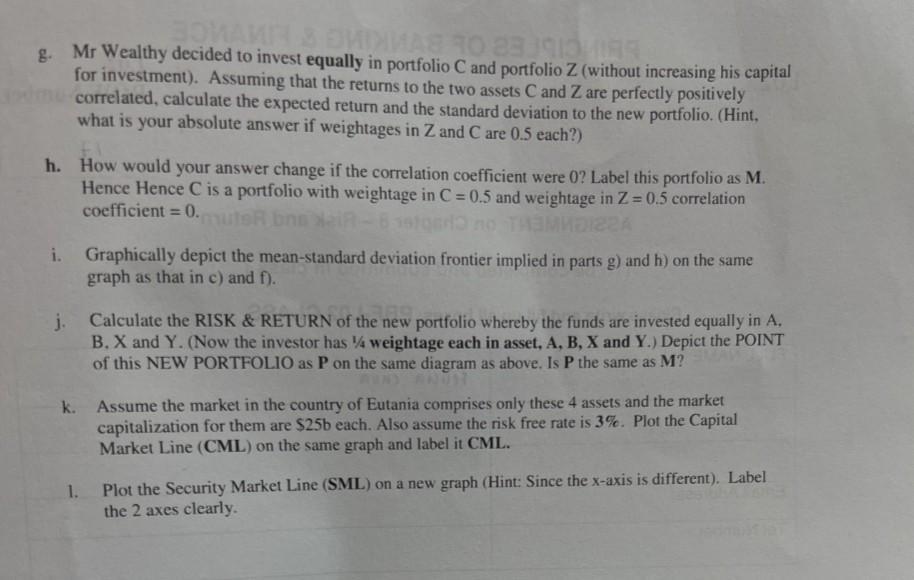

SHOW WORKINGS for ALL your answers: An investor, Mr WEALTHY has two assets available named X...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Lets start with part a a Given Asset X Expected return X 7 Standard deviation X 4 Asset Y Expected return Y 12 Standard deviation Y 6 Portfolio weight... View the full answer

Related Book For

Posted Date: