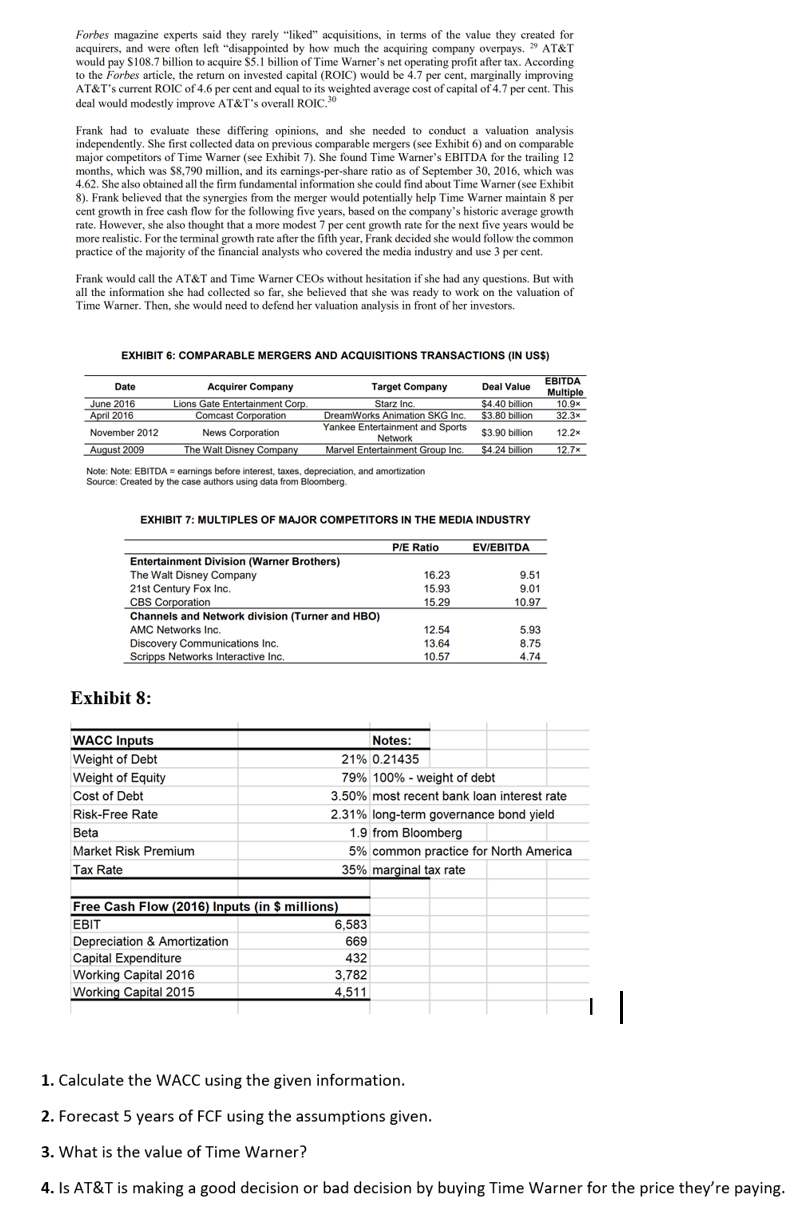

Forbes magazine experts said they rarely liked acquisitions, in terms of the value they created for...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer To calculate the Weighted Average Cost of Capital WACC we need to use the following inputs provided in Exhibit 8 Weight of Debt 21 Weight of Eq... View the full answer

Related Book For

Posted Date: