h. Determine the incremental depreciation between the old and new equipment and the related tax shield...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

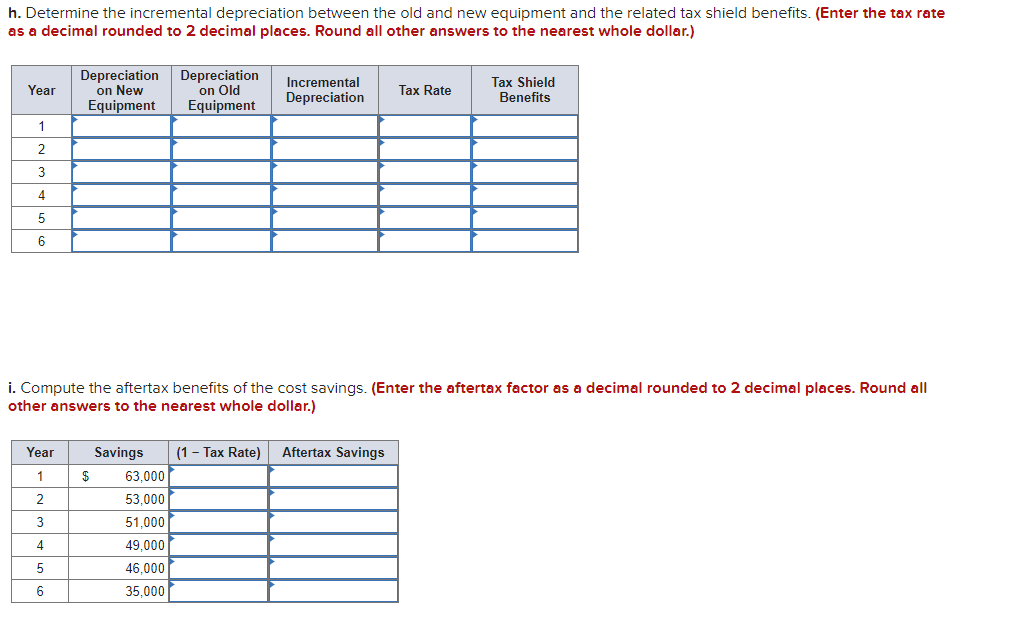

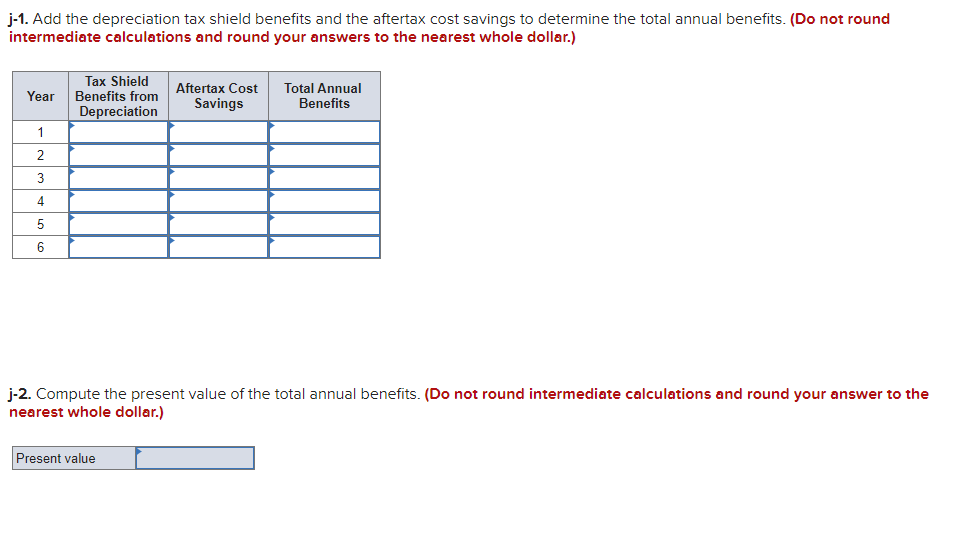

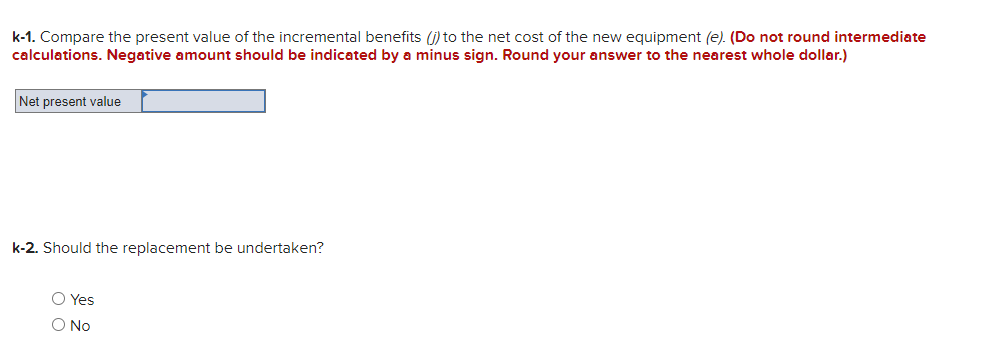

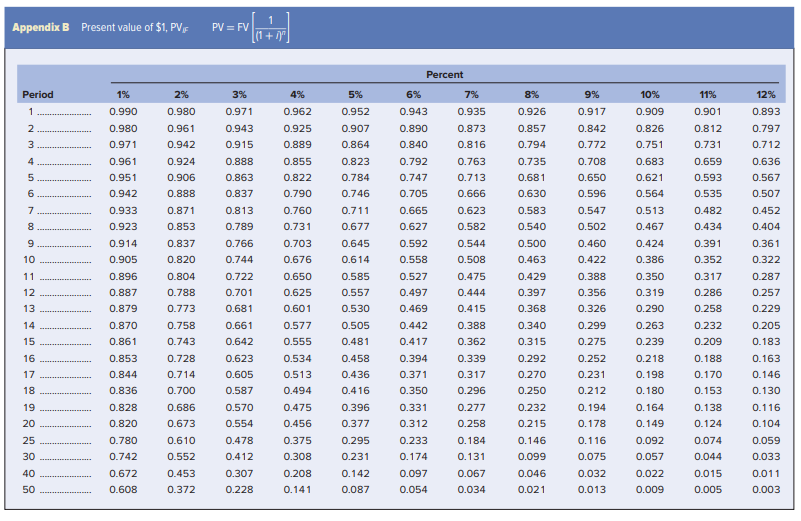

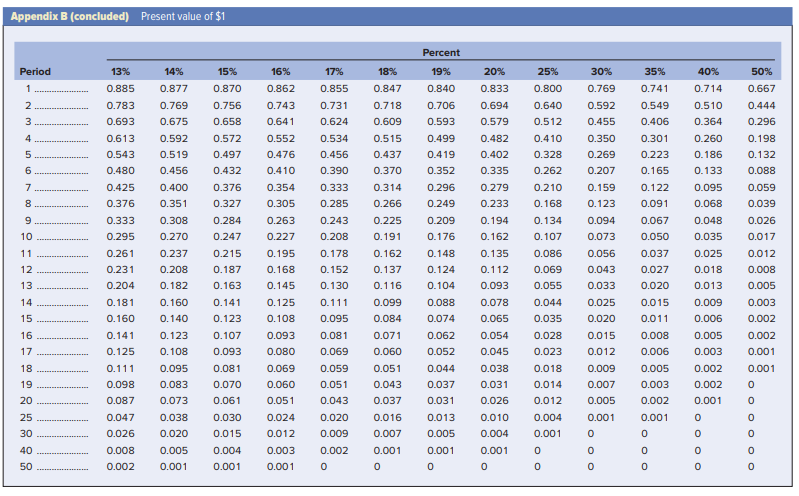

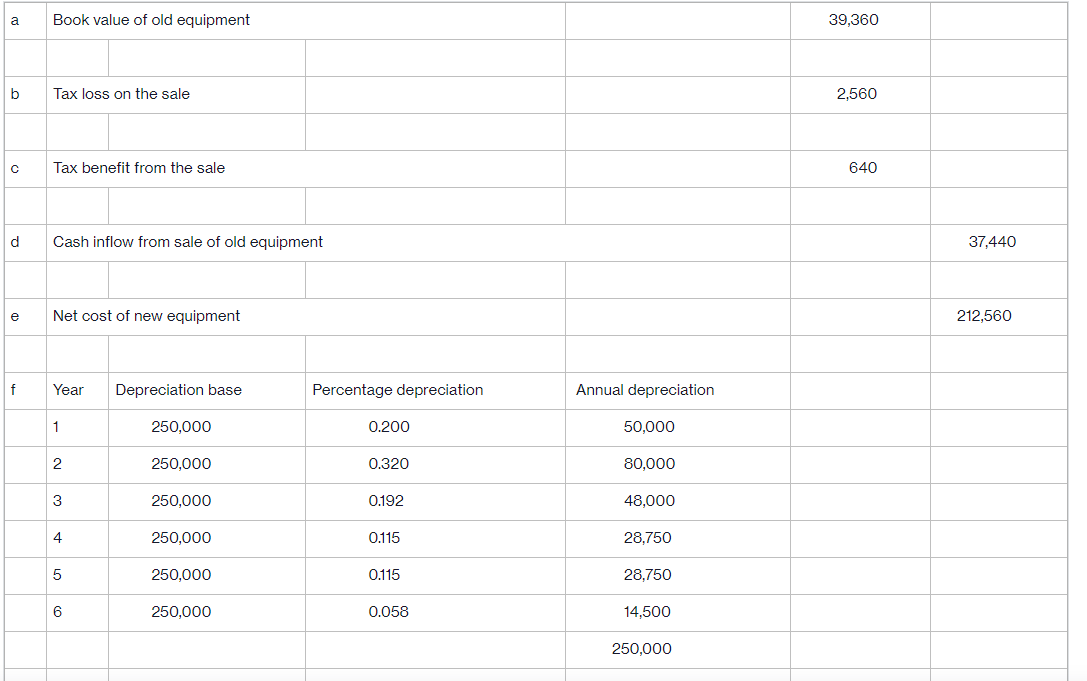

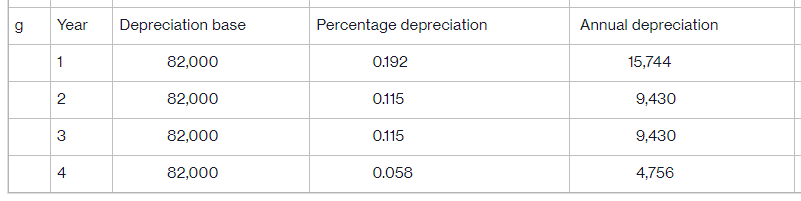

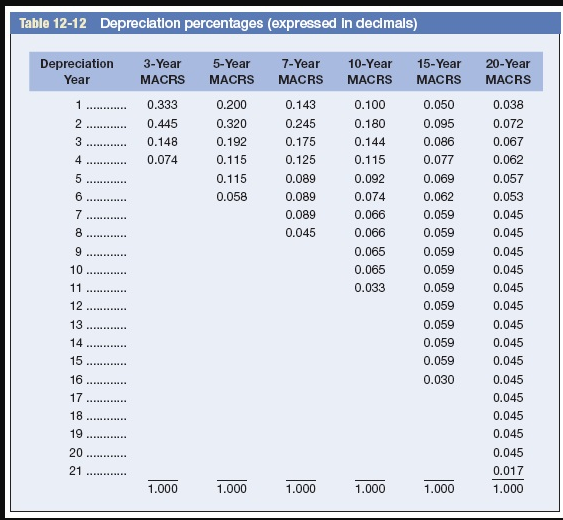

h. Determine the incremental depreciation between the old and new equipment and the related tax shield benefits. (Enter the tax rate as a decimal rounded to 2 decimal places. Round all other answers to the nearest whole dollar.) Year Depreciation on New Equipment Depreciation on Old Equipment Incremental Depreciation Tax Rate Tax Shield Benefits 1 2 3 4 5 6 i. Compute the aftertax benefits of the cost savings. (Enter the aftertax factor as a decimal rounded to 2 decimal places. Round all other answers to the nearest whole dollar.) Year Savings (1 - Tax Rate) Aftertax Savings 1 $ 63,000 2 53,000 3 51,000 4 49,000 5 46,000 6 35,000 j-1. Add the depreciation tax shield benefits and the aftertax cost savings to determine the total annual benefits. (Do not round intermediate calculations and round your answers to the nearest whole dollar.) Year Tax Shield Benefits from Depreciation Aftertax Cost Savings Total Annual Benefits 1 2 3 4 5 6 j-2. Compute the present value of the total annual benefits. (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Present value k-1. Compare the present value of the incremental benefits (/) to the net cost of the new equipment (e). (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answer to the nearest whole dollar.) Net present value k-2. Should the replacement be undertaken? Yes No Appendix B Present value of $1, PV, 1 PV=FV 1+ Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.901 0.893 23456780 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 0.812 0.797 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 0.567 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 0.482 0.452 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 0.404 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 0.352 0.322 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 0.317 0.287 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 0.258 0.229 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 0.232 0.205 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 0.209 0.183 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 0.138 0.116 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 0.124 0.104 25 0.780 0.610 0.478 0.375 0.295 0.233 0.184 0.146 0.116 0.092 0.074 0.059 30 0.742 0.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.208 0.142 0.097 0.067 0.046 0.032 0.022 0.015 0.011 50 0.608 0.372 0.228 0.141 0.087 0.054 0.034 0.021 0.013 0.009 0.005 0.003 Appendix B (concluded) Present value of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 35% 40% 50% 1 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.800 0.769 0.741 0.714 0.667 2 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.592 0.549 0.510 0.444 3 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 4 0.613 0.592 0.572 0.552 0.534 0.515 0.499 0.482 0.410 0.350 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 6 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.088 7 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 0.095 0.059 8 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 0.168 0.123 0.091 0.068 0.039 9 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 10 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 0.107 0.073 0.050 0.035 0.017 11 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 0.086 0.056 0.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 0.055 0.033 0.020 0.013 0.005 14 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 0.044 0.025 0.015 0.009 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 0.035 0.020 0.011 0.006 0.002 16 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 0.028 0.015 0.008 0.005 0.002 17 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 0.023 0.012 0.006 0.003 0.001 18 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 0.018 0.009 0.005 0.002 0.001 19 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 0.014 0.007 0.003 0.002 20 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026 0.012 0.005 0.002 0.001 25 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010 0.004 0.001 0.001 30 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004 0.001 40 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001 0 50 0.002 0.001 0.001 0.001 0 0 0 0 00 000 oooo oooooo 0 0 a Book value of old equipment 39,360 b Tax loss on the sale Tax benefit from the sale d Cash inflow from sale of old equipment e Net cost of new equipment f Year Depreciation base Percentage depreciation Annual depreciation 1 250,000 0.200 50,000 2 250,000 0.320 80,000 3 250,000 0.192 48,000 4 250,000 0.115 28,750 5 250,000 0.115 28,750 6 250,000 0.058 14,500 250,000 2,560 640 37,440 212,560 g Year Depreciation base Percentage depreciation Annual depreciation 1 82,000 0.192 15,744 2 82,000 0.115 9,430 3 82,000 0.115 9,430 4 82,000 0.058 4,756 Table 12-12 Depreciation percentages (expressed in decimals) Depreciation 3-Year 5-Year Year MACRS MACRS 7-Year 10-Year MACRS MACRS 15-Year 20-Year MACRS MACRS 1 0.333 0.200 0.143 0.100 0.050 0.038 234 569 0.445 0.320 0.245 0.180 0.095 0.072 0.148 0.192 0.175 0.144 0.086 0.067 0.074 0.115 0.125 0.115 0.077 0.062 0.115 0.089 0.092 0.069 0.057 0.058 0.089 0.074 0.062 0.053 0.089 0.066 0.059 0.045 8 0.045 0.066 0.059 0.045 9 10 0.065 0.059 0.045 0.065 0.059 0.045 21 3456722 11 12 13 14 15 0.033 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 16 0.030 0.045 17 18 19 0.045 0.045 0.045 20 0.045 0.017 1.000 1.000 1.000 1.000 1.000 1.000 h. Determine the incremental depreciation between the old and new equipment and the related tax shield benefits. (Enter the tax rate as a decimal rounded to 2 decimal places. Round all other answers to the nearest whole dollar.) Year Depreciation on New Equipment Depreciation on Old Equipment Incremental Depreciation Tax Rate Tax Shield Benefits 1 2 3 4 5 6 i. Compute the aftertax benefits of the cost savings. (Enter the aftertax factor as a decimal rounded to 2 decimal places. Round all other answers to the nearest whole dollar.) Year Savings (1 - Tax Rate) Aftertax Savings 1 $ 63,000 2 53,000 3 51,000 4 49,000 5 46,000 6 35,000 j-1. Add the depreciation tax shield benefits and the aftertax cost savings to determine the total annual benefits. (Do not round intermediate calculations and round your answers to the nearest whole dollar.) Year Tax Shield Benefits from Depreciation Aftertax Cost Savings Total Annual Benefits 1 2 3 4 5 6 j-2. Compute the present value of the total annual benefits. (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Present value k-1. Compare the present value of the incremental benefits (/) to the net cost of the new equipment (e). (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answer to the nearest whole dollar.) Net present value k-2. Should the replacement be undertaken? Yes No Appendix B Present value of $1, PV, 1 PV=FV 1+ Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.901 0.893 23456780 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 0.812 0.797 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 0.567 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 0.482 0.452 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 0.404 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 0.352 0.322 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 0.317 0.287 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 0.258 0.229 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 0.232 0.205 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 0.209 0.183 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 0.138 0.116 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 0.124 0.104 25 0.780 0.610 0.478 0.375 0.295 0.233 0.184 0.146 0.116 0.092 0.074 0.059 30 0.742 0.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.208 0.142 0.097 0.067 0.046 0.032 0.022 0.015 0.011 50 0.608 0.372 0.228 0.141 0.087 0.054 0.034 0.021 0.013 0.009 0.005 0.003 Appendix B (concluded) Present value of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 35% 40% 50% 1 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.800 0.769 0.741 0.714 0.667 2 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.592 0.549 0.510 0.444 3 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 4 0.613 0.592 0.572 0.552 0.534 0.515 0.499 0.482 0.410 0.350 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 6 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.088 7 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 0.095 0.059 8 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 0.168 0.123 0.091 0.068 0.039 9 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 10 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 0.107 0.073 0.050 0.035 0.017 11 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 0.086 0.056 0.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 0.055 0.033 0.020 0.013 0.005 14 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 0.044 0.025 0.015 0.009 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 0.035 0.020 0.011 0.006 0.002 16 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 0.028 0.015 0.008 0.005 0.002 17 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 0.023 0.012 0.006 0.003 0.001 18 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 0.018 0.009 0.005 0.002 0.001 19 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 0.014 0.007 0.003 0.002 20 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026 0.012 0.005 0.002 0.001 25 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010 0.004 0.001 0.001 30 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004 0.001 40 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001 0 50 0.002 0.001 0.001 0.001 0 0 0 0 00 000 oooo oooooo 0 0 a Book value of old equipment 39,360 b Tax loss on the sale Tax benefit from the sale d Cash inflow from sale of old equipment e Net cost of new equipment f Year Depreciation base Percentage depreciation Annual depreciation 1 250,000 0.200 50,000 2 250,000 0.320 80,000 3 250,000 0.192 48,000 4 250,000 0.115 28,750 5 250,000 0.115 28,750 6 250,000 0.058 14,500 250,000 2,560 640 37,440 212,560 g Year Depreciation base Percentage depreciation Annual depreciation 1 82,000 0.192 15,744 2 82,000 0.115 9,430 3 82,000 0.115 9,430 4 82,000 0.058 4,756 Table 12-12 Depreciation percentages (expressed in decimals) Depreciation 3-Year 5-Year Year MACRS MACRS 7-Year 10-Year MACRS MACRS 15-Year 20-Year MACRS MACRS 1 0.333 0.200 0.143 0.100 0.050 0.038 234 569 0.445 0.320 0.245 0.180 0.095 0.072 0.148 0.192 0.175 0.144 0.086 0.067 0.074 0.115 0.125 0.115 0.077 0.062 0.115 0.089 0.092 0.069 0.057 0.058 0.089 0.074 0.062 0.053 0.089 0.066 0.059 0.045 8 0.045 0.066 0.059 0.045 9 10 0.065 0.059 0.045 0.065 0.059 0.045 21 3456722 11 12 13 14 15 0.033 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 0.059 0.045 16 0.030 0.045 17 18 19 0.045 0.045 0.045 20 0.045 0.017 1.000 1.000 1.000 1.000 1.000 1.000

Expert Answer:

Related Book For

Foundations of Financial Management

ISBN: 978-1259194078

15th edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen

Posted Date:

Students also viewed these finance questions

-

Do you think that the increase in e-commerce acquisitions is beneficial or disadvantageous to small businesses?

-

d. Blood is mostly water, but has a lower surface tension (~55 mN/m), why? (what contents in blood attribute to the surface tension reduction? Why?

-

Hercules Exercise Equipment Co. purchased a computerized measuring device two years ago for $74,000. The equipment falls into the five-year category for MACRS depreciation and can currently be sold...

-

A restaurant records the following data over a month for its food: Opening inventory: $31,000 Purchases: $88,000 Closing Inventory: $28,000 Transfers in: $800 Transfers out: $200 Employee meals:...

-

A survey is conducted from a population of people of whom 40% have a college degree. The following sample data were recorded for a question asked of each person sampled, "Do you have a college...

-

Let Hf (c) be a bounding hyperplane of a cone C in a normed linear space X, that is, f (x) c for every x C. Then f (x) 0 for every x C

-

Stillsville Corporation manufactures an electronic switch for dishwashers. The cost base per unit, excluding selling and administrative expenses, is $60. The per unit cost of selling and...

-

A recent study by Web Mystery Shoppers International indicates that holiday gift cards are becoming increasingly popular at online retailers. Two years ago, online shoppers had to really hunt at most...

-

The quadrilateral KLMN is a square. Given two of the vertices are M(0.0), N(c,0), determine the coordinates of the point K? K(0, c) K(c, c) K(-c, 0) K(c2.c2) M(0,0) N(c,0)

-

Write a program that queries information from two files. The first file contains the names and telephone numbers of a group of people. The second file contains the names and Social Security numbers...

-

You are planning a trip to the United Kingdom and expect that you will spend 2.300 pounds. How much will your spending be in US dollars if the exchange rate is 7287 pounds per dollar?

-

Explain the impact of innovative construction techniques such as 3D printing and modular construction on the field of structural engineering. What are the potential benefits and challenges associated...

-

Baller Financial is a banking services company that offers many different types of checking accounts. The bank has recently adopted an activity-based costing system to assign costs to their various...

-

Benoit Company produces three products-A, B, and C. Data concerning the three products follow (per unit): Product B A Selling price Variable expenses: $ 92.00 $ 66.00 $ 82.00 Direct materials Total...

-

How can finite element analysis be used to simulate complex structural behaviors, and what are the primary factors that influence the accuracy of FEA models in civil engineering applications ?

-

When you are giving a sales presentation, _ _ _ _ _ . it is likely that your prospect will wait until you have finished your presentation before asking you questions very often the prospect will ask...

-

What is the ideal number of children to have? This question was asked on the Sullivan Statistics Survey I. Draw a dot plot of the variable Children from theSullivanStatsSurveyI data set at...

-

When it comes to translating the financial statements of entities in highly inflationary countries, which of the following approaches makes more sense and why? a. Remeasure using the temporal method,...

-

Why do currency differences affect foreign exchange reporting?

-

Why do German and French approaches to reporting foreign exchange gains and losses differ from those in the United Kingdom?

Study smarter with the SolutionInn App