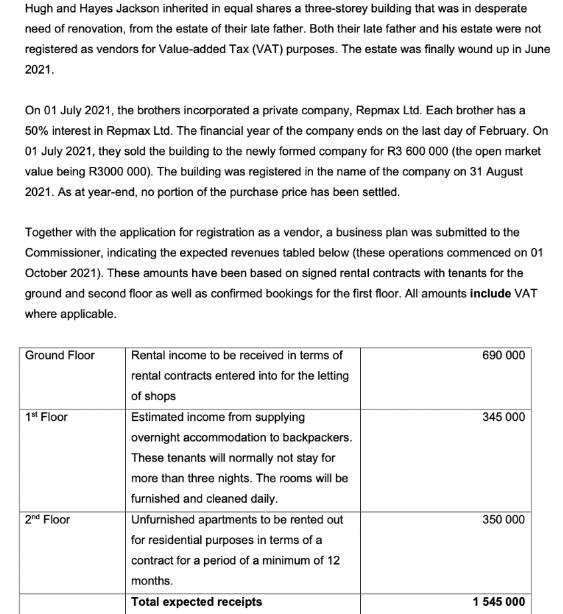

Hugh and Hayes Jackson inherited in equal shares a three-storey building that was in desperate need...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

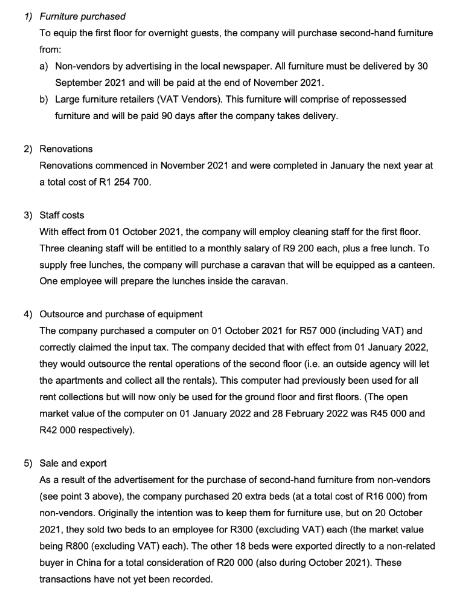

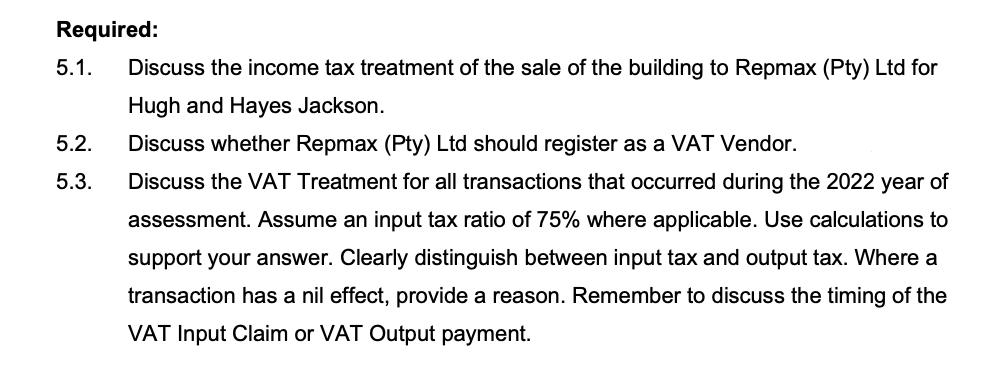

Hugh and Hayes Jackson inherited in equal shares a three-storey building that was in desperate need of renovation, from the estate of their late father. Both their late father and his estate were not registered as vendors for Value-added Tax (VAT) purposes. The estate was finally wound up in June 2021. On 01 July 2021, the brothers incorporated a private company, Repmax Ltd. Each brother has a 50% interest in Repmax Ltd. The financial year of the company ends on the last day of February. On 01 July 2021, they sold the building to the newly formed company for R3 600 000 (the open market value being R3000 000). The building was registered in the name of the company on 31 August 2021. As at year-end, no portion of the purchase price has been settled. Together with the application for registration as a vendor, a business plan was submitted to the Commissioner, indicating the expected revenues tabled below (these operations commenced on 01 October 2021). These amounts have been based on signed rental contracts with tenants for the ground and second floor as well as confirmed bookings for the first floor. All amounts include VAT where applicable. Ground Floor 1st Floor 2nd Floor Rental income to be received in terms of rental contracts entered into for the letting of shops Estimated income from supplying overnight accommodation to backpackers. These tenants will normally not stay for more than three nights. The rooms will be furnished and cleaned daily. Unfurnished apartments to be rented out for residential purposes in terms of a contract for a period of a minimum of 12 months. Total expected receipts 690 000 345 000 350 000 1 545 000 1) Furniture purchased To equip the first floor for overnight guests, the company will purchase second-hand furniture from: a) Non-vendors by advertising in the local newspaper. All furniture must be delivered by 30 September 2021 and will be paid at the end of November 2021. b) Large furniture retailers (VAT Vendors). This furniture will comprise of repossessed furniture and will be paid 90 days after the company takes delivery. 2) Renovations Renovations commenced in November 2021 and were completed in January the next year at a total cost of R1 254 700. 3) Staff costs With effect from 01 October 2021, the company will employ cleaning staff for the first floor. Three cleaning staff will be entitled to a monthly salary of R9 200 each, plus a free lunch. To supply free lunches, the company will purchase a caravan that will be equipped as a canteen. One employee will prepare the lunches inside the caravan. 4) Outsource and purchase of equipment The company purchased a computer on 01 October 2021 for R57 000 (including VAT) and correctly claimed the input tax. The company decided that with effect from 01 January 2022, they would outsource the rental operations of the second floor (i.e. an outside agency will let the apartments and collect all the rentals). This computer had previously been used for all rent collections but will now only be used for the ground floor and first floors. (The open market value of the computer on 01 January 2022 and 28 February 2022 was R45 000 and R42 000 respectively). 5) Sale and export As a result of the advertisement for the purchase of second-hand furniture from non-vendors (see point 3 above), the company purchased 20 extra beds (at a total cost of R16 000) from non-vendors. Originally the intention was to keep them for furniture use, but on 20 October 2021, they sold two beds to an employee for R300 (excluding VAT) each (the market value being R800 (excluding VAT) each). The other 18 beds were exported directly to a non-related buyer in China for a total consideration of R20 000 (also during October 2021). These transactions have not yet been recorded. Required: 5.1. Discuss the income tax treatment of the sale of the building to Repmax (Pty) Ltd for Hugh and Hayes Jackson. Discuss whether Repmax (Pty) Ltd should register as a VAT Vendor. Discuss the VAT Treatment for all transactions that occurred during the 2022 year of assessment. Assume an input tax ratio of 75% where applicable. Use calculations to support your answer. Clearly distinguish between input tax and output tax. Where a transaction has a nil effect, provide a reason. Remember to discuss the timing of the VAT Input Claim or VAT Output payment. 5.2. 5.3. Hugh and Hayes Jackson inherited in equal shares a three-storey building that was in desperate need of renovation, from the estate of their late father. Both their late father and his estate were not registered as vendors for Value-added Tax (VAT) purposes. The estate was finally wound up in June 2021. On 01 July 2021, the brothers incorporated a private company, Repmax Ltd. Each brother has a 50% interest in Repmax Ltd. The financial year of the company ends on the last day of February. On 01 July 2021, they sold the building to the newly formed company for R3 600 000 (the open market value being R3000 000). The building was registered in the name of the company on 31 August 2021. As at year-end, no portion of the purchase price has been settled. Together with the application for registration as a vendor, a business plan was submitted to the Commissioner, indicating the expected revenues tabled below (these operations commenced on 01 October 2021). These amounts have been based on signed rental contracts with tenants for the ground and second floor as well as confirmed bookings for the first floor. All amounts include VAT where applicable. Ground Floor 1st Floor 2nd Floor Rental income to be received in terms of rental contracts entered into for the letting of shops Estimated income from supplying overnight accommodation to backpackers. These tenants will normally not stay for more than three nights. The rooms will be furnished and cleaned daily. Unfurnished apartments to be rented out for residential purposes in terms of a contract for a period of a minimum of 12 months. Total expected receipts 690 000 345 000 350 000 1 545 000 1) Furniture purchased To equip the first floor for overnight guests, the company will purchase second-hand furniture from: a) Non-vendors by advertising in the local newspaper. All furniture must be delivered by 30 September 2021 and will be paid at the end of November 2021. b) Large furniture retailers (VAT Vendors). This furniture will comprise of repossessed furniture and will be paid 90 days after the company takes delivery. 2) Renovations Renovations commenced in November 2021 and were completed in January the next year at a total cost of R1 254 700. 3) Staff costs With effect from 01 October 2021, the company will employ cleaning staff for the first floor. Three cleaning staff will be entitled to a monthly salary of R9 200 each, plus a free lunch. To supply free lunches, the company will purchase a caravan that will be equipped as a canteen. One employee will prepare the lunches inside the caravan. 4) Outsource and purchase of equipment The company purchased a computer on 01 October 2021 for R57 000 (including VAT) and correctly claimed the input tax. The company decided that with effect from 01 January 2022, they would outsource the rental operations of the second floor (i.e. an outside agency will let the apartments and collect all the rentals). This computer had previously been used for all rent collections but will now only be used for the ground floor and first floors. (The open market value of the computer on 01 January 2022 and 28 February 2022 was R45 000 and R42 000 respectively). 5) Sale and export As a result of the advertisement for the purchase of second-hand furniture from non-vendors (see point 3 above), the company purchased 20 extra beds (at a total cost of R16 000) from non-vendors. Originally the intention was to keep them for furniture use, but on 20 October 2021, they sold two beds to an employee for R300 (excluding VAT) each (the market value being R800 (excluding VAT) each). The other 18 beds were exported directly to a non-related buyer in China for a total consideration of R20 000 (also during October 2021). These transactions have not yet been recorded. Required: 5.1. Discuss the income tax treatment of the sale of the building to Repmax (Pty) Ltd for Hugh and Hayes Jackson. Discuss whether Repmax (Pty) Ltd should register as a VAT Vendor. Discuss the VAT Treatment for all transactions that occurred during the 2022 year of assessment. Assume an input tax ratio of 75% where applicable. Use calculations to support your answer. Clearly distinguish between input tax and output tax. Where a transaction has a nil effect, provide a reason. Remember to discuss the timing of the VAT Input Claim or VAT Output payment. 5.2. 5.3.

Expert Answer:

Answer rating: 100% (QA)

51 The sale of the building to Repmax Pty Ltd by Hugh and Hayes Jackson would be subject to income tax Since the building was sold to the company it is considered a disposal of an asset by the individ... View the full answer

Related Book For

South-Western Federal Taxation 2018 Comprehensive

ISBN: 9781337386005

41st Edition

Authors: David M. Maloney, William H. Hoffman, Jr., William A. Raabe, James C. Young

Posted Date:

Students also viewed these law questions

-

Write a single statement that will print the message "first is " followed by a space followed by the value of first, and then a space, followed by "second = " , followed by the value of second. Print...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Various statistical software packages tend to provide different measures of association. Use statistical software to calculate the Goodman-Kruskal gamma, Somers D, or Kendalls tau-a for the space...

-

KG Spring Skating School Inc. had the following account balances as at April 30, 2012: Cash $23,000; Equipment $2,000; Accounts Payable $500; Unearned Revenue (for advance registration fees) $17,500;...

-

An extermination firm is testing several brands of pesticide spray, all of which claim to be effective against ants. Under controlled conditions, each spray is used on 10 ants of the species listed...

-

Sebel Corporation had cash flows from operating activities during the past year of $194,000. During the year, the company expended $25,000 for dividends; expended $158,000 for property, plant, and...

-

The T-accounts for Equipment and the related Accumulated Depreciation Equip. for Coldsmith Company at the end of 2014 are shown here. In addition, Coldsmith Companys income statement reported a loss...

-

\ table [ [ Current assets.,End of Year, \ table [ [ Beginning of ] , [ Year ] ] ] , [ Cash and cash equivalentc,, ] , [ Accounts receivable,$ 5 7 , 0 0 0 , $ 8 4 , 0 0 0

-

The budget director of Birding Homes & Feeders Inc., with the assistance of the controller, treasurer, production manager, and sales manager, has gathered the following data for use in developing the...

-

TechNova Ltd. Initial Financial Position (31 December 2023): Share capital, authorised and issued: 200,000 7% cumulative preference shares of $1 each: $200,000 500,000 ordinary shares of $1 each:...

-

The following dataset on supermarket sales is obtained from Kaggle. It contains a sample dataset from the internal database of a supermarket from three different branches for three months. The...

-

(5%) Problem 3: Cranes use a system of two pulleys to provide mechanical advantage, which reduces the force they need to apply to lift a particular weight (two such possible configurations are shown...

-

According to a recent press report, The South Reserve Bank ( hereafter The Bank ) fined Capitec and the local branch of Deutsche Bank a combined total of R 2 5 m last year for shortcomings in the...

-

List four aggravating factors for the risks faced by Stora Ensothat could impact the profits generated by the companies in the forest produce industry based on risks identified in table. Risk...

-

Swazi Inc. has an average tax rate of 23% and has pre-tax cost of equity of 14% and after tax debt cost of 4%. The firm's Market Value of Debt to Equity is 0.8. Swazi is in the process of evaluating...

-

Diving Equipment Private Limited ("DEPL") is a distributor who imports five major brands of diving equipment and distributes them to local sports shops. The company makes adjusting entries at each...

-

on 8 For the following set of lengths 130, 170, 160, 160, 150, 190 Third quartile is: et red d out of Select one: O a. 160 a question O b. 145 O c. 175 O d. 180

-

Fran, who is in the 35% tax bracket, recently collected $100,000 on a life insurance policy she carried on her father. She currently owes $120,000 on her personal residence and $120,000 on business...

-

Jayden calculates his Federal income tax by using both the Tax Tables and the Tax Rate Schedules. Because the Tax Rate Schedules yield a slightly lower tax liability, he plans to pay this amount. a....

-

David contributes to charity some tangible personal property that he had used in his business and depreciated. At the date of the donation, the property has a fair market value of $233,000 and an...

-

During 20x6, Chester Corporation reported a net income of $1,529,500. On January 1, Chester had 1,400,000 shares of common stock outstanding. The company issued an additional 840,000 shares of common...

-

The stockholders equity section of Ruff Corporations balance sheet on December 31, 20x7, follows. Prepare a statement of stockholders equity for the year ended December 31, 20x8, assuming these...

-

On January 15, the board of directors of Picado International declared a 3-for-1 stock split of its $12 par value common stock, of which 1,600,000 shares were authorized and 400,000 were issued and...

Study smarter with the SolutionInn App