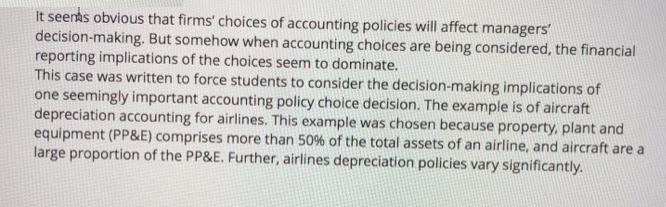

It seems obvious that firms' choices of accounting policies will affect managers' decision-making. But somehow when...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

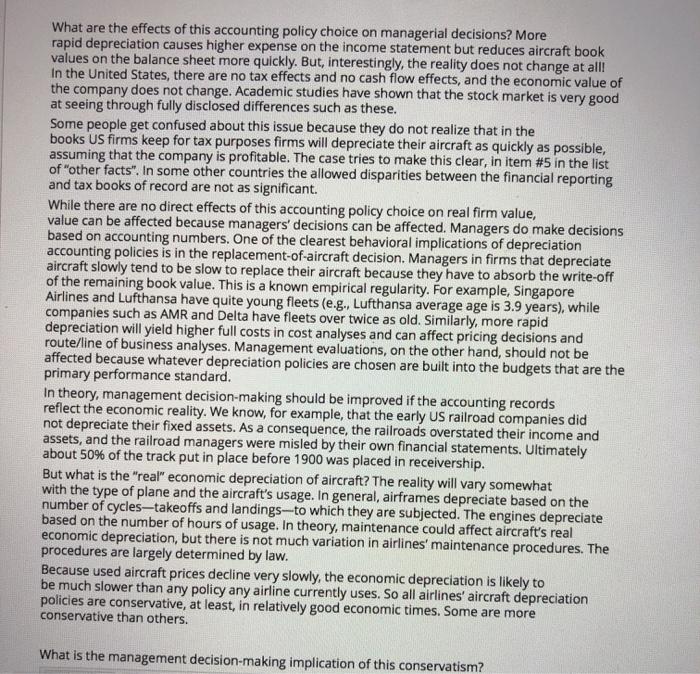

It seems obvious that firms' choices of accounting policies will affect managers' decision-making. But somehow when accounting choices are being considered, the financial reporting implications of the choices seem to dominate. This case was written to force students to consider the decision-making implications of one seemingly important accounting policy choice decision. The example is of aircraft depreciation accounting for airlines. This example was chosen because property, plant and equipment (PP&E) comprises more than 50% of the total assets of an airline, and aircraft are a large proportion of the PP&E. Further, airlines depreciation policies vary significantly. What are the effects of this accounting policy choice on managerial decisions? More rapid depreciation causes higher expense on the income statement but reduces aircraft book values on the balance sheet more quickly. But, interestingly, the reality does not change at all! In the United States, there are no tax effects and no cash flow effects, and the economic value of the company does not change. Academic studies have shown that the stock market is very good at seeing through fully disclosed differences such as these. Some people get confused about this issue because they do not realize that in the books US firms keep for tax purposes firms will depreciate their aircraft as quickly as possible, assuming that the company is profitable. The case tries to make this clear, in item #5 in the list of "other facts". In some other countries the allowed disparities between the financial reporting and tax books of record are not as significant. While there are no direct effects of this accounting policy choice on real firm value, value can be affected because managers' decisions can be affected. Managers do make decisions based on accounting numbers. One of the clearest behavioral implications of depreciation accounting policies is in the replacement-of-aircraft decision. Managers in firms that depreciate aircraft slowly tend to be slow to replace their aircraft because they have to absorb the write-off of the remaining book value. This is a known empirical regularity. For example, Singapore Airlines and Lufthansa have quite young fleets (e.g., Lufthansa average age is 3.9 years), while companies such as AMR and Delta have fleets over twice as old. Similarly, more rapid depreciation will yield higher full costs in cost analyses and can affect pricing decisions and route/line of business analyses. Management evaluations, on the other hand, should not be affected because whatever depreciation policies are chosen are built into the budgets that are the primary performance standard. In theory, management decision-making should be improved if the accounting records reflect the economic reality. We know, for example, that the early US railroad companies did not depreciate their fixed assets. As a consequence, the railroads overstated their income and assets, and the railroad managers were misled by their own financial statements. Ultimately about 50% of the track put in place before 1900 was placed in receivership. But what is the "real" economic depreciation of aircraft? The reality will vary somewhat with the type of plane and the aircraft's usage. In general, airframes depreciate based on the number of cycles-takeoffs and landings-to which they are subjected. The engines depreciate based on the number of hours of usage. In theory, maintenance could affect aircraft's real economic depreciation, but there is not much variation in airlines' maintenance procedures. The procedures are largely determined by law. Because used aircraft prices decline very slowly, the economic depreciation is likely to be much slower than any policy any airline currently uses. So all airlines' aircraft depreciation policies are conservative, at least, in relatively good economic times. Some are more conservative than others. What is the management decision-making implication of this conservatism? It seems obvious that firms' choices of accounting policies will affect managers' decision-making. But somehow when accounting choices are being considered, the financial reporting implications of the choices seem to dominate. This case was written to force students to consider the decision-making implications of one seemingly important accounting policy choice decision. The example is of aircraft depreciation accounting for airlines. This example was chosen because property, plant and equipment (PP&E) comprises more than 50% of the total assets of an airline, and aircraft are a large proportion of the PP&E. Further, airlines depreciation policies vary significantly. What are the effects of this accounting policy choice on managerial decisions? More rapid depreciation causes higher expense on the income statement but reduces aircraft book values on the balance sheet more quickly. But, interestingly, the reality does not change at all! In the United States, there are no tax effects and no cash flow effects, and the economic value of the company does not change. Academic studies have shown that the stock market is very good at seeing through fully disclosed differences such as these. Some people get confused about this issue because they do not realize that in the books US firms keep for tax purposes firms will depreciate their aircraft as quickly as possible, assuming that the company is profitable. The case tries to make this clear, in item #5 in the list of "other facts". In some other countries the allowed disparities between the financial reporting and tax books of record are not as significant. While there are no direct effects of this accounting policy choice on real firm value, value can be affected because managers' decisions can be affected. Managers do make decisions based on accounting numbers. One of the clearest behavioral implications of depreciation accounting policies is in the replacement-of-aircraft decision. Managers in firms that depreciate aircraft slowly tend to be slow to replace their aircraft because they have to absorb the write-off of the remaining book value. This is a known empirical regularity. For example, Singapore Airlines and Lufthansa have quite young fleets (e.g., Lufthansa average age is 3.9 years), while companies such as AMR and Delta have fleets over twice as old. Similarly, more rapid depreciation will yield higher full costs in cost analyses and can affect pricing decisions and route/line of business analyses. Management evaluations, on the other hand, should not be affected because whatever depreciation policies are chosen are built into the budgets that are the primary performance standard. In theory, management decision-making should be improved if the accounting records reflect the economic reality. We know, for example, that the early US railroad companies did not depreciate their fixed assets. As a consequence, the railroads overstated their income and assets, and the railroad managers were misled by their own financial statements. Ultimately about 50% of the track put in place before 1900 was placed in receivership. But what is the "real" economic depreciation of aircraft? The reality will vary somewhat with the type of plane and the aircraft's usage. In general, airframes depreciate based on the number of cycles-takeoffs and landings-to which they are subjected. The engines depreciate based on the number of hours of usage. In theory, maintenance could affect aircraft's real economic depreciation, but there is not much variation in airlines' maintenance procedures. The procedures are largely determined by law. Because used aircraft prices decline very slowly, the economic depreciation is likely to be much slower than any policy any airline currently uses. So all airlines' aircraft depreciation policies are conservative, at least, in relatively good economic times. Some are more conservative than others. What is the management decision-making implication of this conservatism?

Expert Answer:

Answer rating: 100% (QA)

ANSWER Decisionmaking is an integral part of modern management Essentially rational or sound decisio... View the full answer

Related Book For

Business Analytics Data Analysis and Decision Making

ISBN: 978-1305947542

6th edition

Authors: S. Christian Albright, Wayne L. Winston

Posted Date:

Students also viewed these accounting questions

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Googles ease of use and superior search results have propelled the search engine to its num- ber one status, ousting the early dominance of competitors such as WebCrawler and Infos- eek. Even later...

-

1. Enis falsely accuses Monalisa of stealing from Island Tours, Inc., their employer. Enis's statement is defamatory only if a. a third party hears it. b. Monalisa has not been caught. c. the...

-

Airlines are said to have high operating risk. Why?

-

Explain the advantages and disadvantages to a covered call writer of closing out the position prior to expiration?

-

Applying the Cost of Goods Sold Model Milton Company reported inventory of \(\$ 60,000\) at the beginning of 2018. During the year, it purchased inventory of \(\$ 625,000\) and sold inventory for...

-

A bond with 5 years to maturity and a coupon rate of 6% has a par, or face, value of $20,000. Interest is paid annually. If you required a return of 8% on this bond, what is the value of this bond to...

-

What is an account receivable? How is it used and configured?

-

1. Assume a 30% tax rate, and the Totals per financial statements provided. Complete the following schedule as per Figure 16.4. Assume that the Totals per financial statements (second to bottom row)...

-

In the Price Leadership model of Exhibit X-3, how much will be the combined supply of the followers in equilibrium? 6 units 9 units 3 units 5 units Zero

-

The income statement for the year 2020 of Blossom Co. contains the following informat Revenues $70900 Expenses: Salaries and Wages Expense $45400 Rent Expense 12500 Advertising Expense 10100 Supplies...

-

Question 3. Tables. Reconstruct the sentence, table and caption shown below. To label the table, use \labelftab: Math2024tasks) after the caption line. To make the cross- reference to "Table 1" in...

-

Recall the geometric series formula = 1 k=0 for all |r| < 1, i.e. -1

-

54. Data: In the following, price, revenue and cost functions, which have been established by an organization for one of its products, Q, represent the number of units produced and sold per week:...

-

jennifer Haslam is sole trader. The following transactions reflects the activities that took place in the month of May 2021. May 01 Started business with $80,000 in the bank May 02 Paid cheque for...

-

A _________ in the BCG Matrix would have a high market share in a low-growth market, and the correct grand or master strategy is______________. Question 81 options: Cash Cow, retrenchment Dog, growth

-

Distinguish between the work performed by public accountants and the work performed by accountants in commerce and industry and in not-for-profit organisations.

-

We didn't discuss the role of sample size in this chapter as thoroughly as we did for confidence intervals in the previous chapter, but more advanced books do include sample size formulas for...

-

The file P12_11.xlsx contains annual U.S. federal debt from 1960 through 2011. Fit an exponential growth curve to these data. Write a short report to summarize your findings. If the U.S. federal debt...

-

Continuing the previous problem, the same data have been split into two sets in the file P17_10.xlsx. The first 9500 observations are in the Training Data sheet, and the last 500 observations are in...

-

Accounting for Partly Completed Events: A Prelude to Chapter 3} Ehrlich Smith, the owner of The Shoe Box, has asked you to help him understand the proper way to account for certain accounting items...

-

Explain how the periodicity assumption, revenue recognition principle, and matching concept affect the determination of income. - The revenue recognition principle under IAS 18 currently specifies...

-

Professional and Ethical Behaviour} Your close friend Avery was recently hired to work in the accounting department at Ted's Automotive Ltd. You are excited to have your friend working at the same...

Study smarter with the SolutionInn App