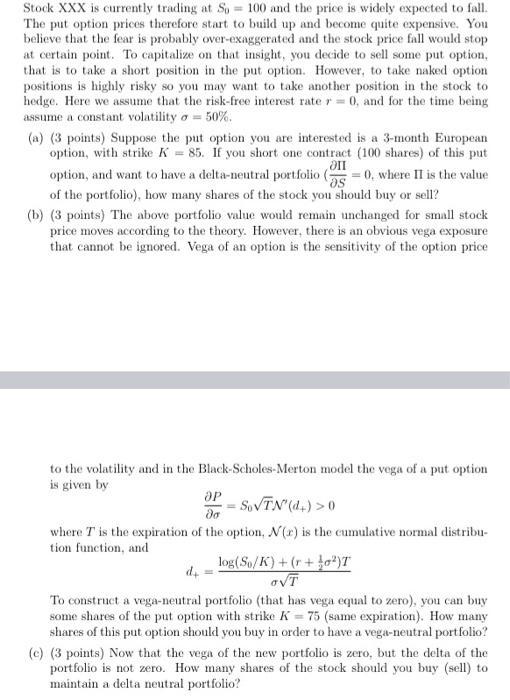

Stock XXX is currently trading at So= 100 and the price is widely expected to fall....

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

As only part b is asked kindly note Nd1 is written as N d1 1 2 e First we need to calculate the vega ... View the full answer

Related Book For

Fundamentals of Investing

ISBN: 978-0133075359

12th edition

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

Posted Date: