Tankmaster Manufacturing Company is a large manufacturer of domestic oil tanks. Since it came into existence...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

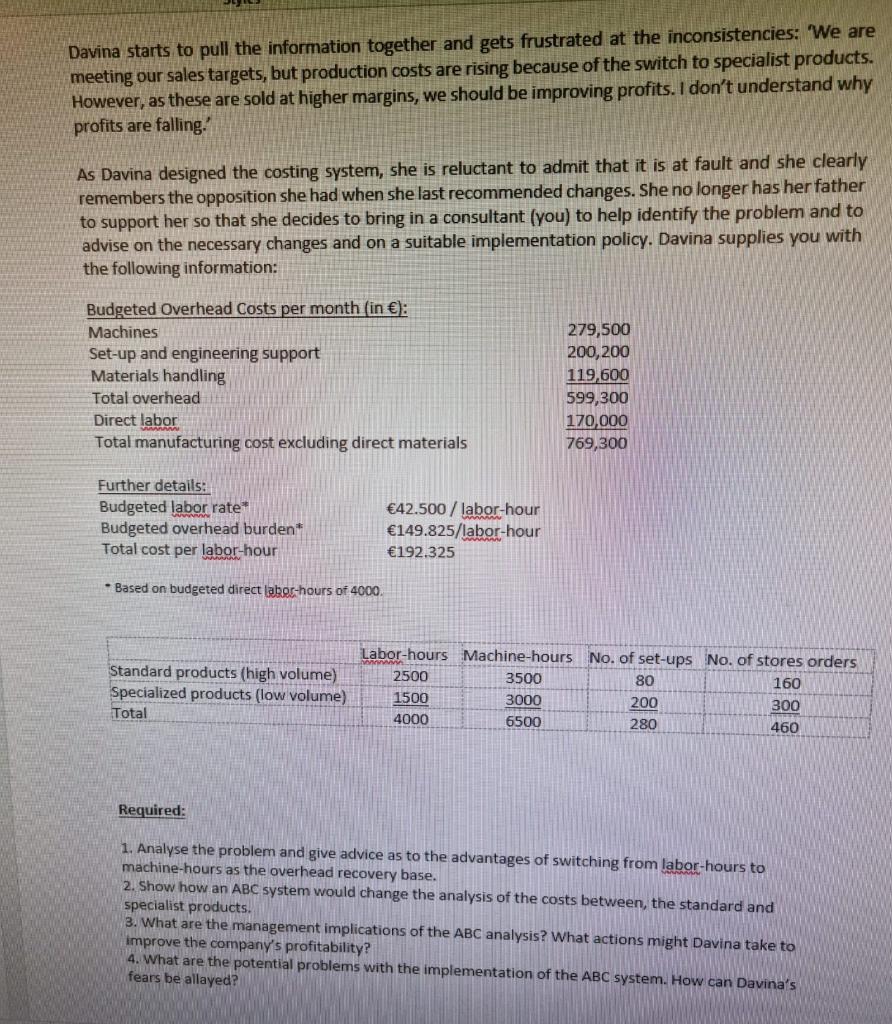

Tankmaster Manufacturing Company is a large manufacturer of domestic oil tanks. Since it came into existence in 1980, the company has enjoyed steady growth in both sales and profits. Davina Tankmaster, the founder's daughter, joined the company in 2010 after graduating with a degree in Accounting and Finance from Manchester University. One of her first tasks was to revise the costing system, as there was a need for more accurate product cost information to support the company's strategy of offering keen prices in a highly competitive market dominated by a few large firms. Davina had faced considerable opposition to the changes she had suggested, with several managers being willing to accept the shortcoming of the old system because they had learned to live with it. Davina won the day largely because of her father's support as the latter was convinced that learned to live with' was a euphemism for 'learned to manipulate to our own advantage'. Davina's father has now retired so that Davina is now conscious of the need to prove herself. Accordingly, the last thing she wants at present is the upset of another major change in the costing system. However, profits are below budget and the accounting is critical of the current costing system, saying that it is hopelessly out of line with the company's updated manufacturing methods and also with current theories on product costing. He says, 'We are still absorbing overheads on labor-hours and we have an absurdly high overhead absorption rate of €150 per labor-hour. We are pricing ourselves out of the market on our old established products. Product costs would be more meaningful if we absorbed overheads on machine-hours. Davina decides she must investigate. Over the past five years, overhead costs had risen to €599,300 per month, a 46% increase, while direct labor-hours have risen from €168,200 to €170,000, a negligible amount. The product processes are now largely mechanized with a relatively high level of automation. Direct labor-hours are 4000 compared with machine-hours of 6500 (it is possible that some labor is still being classed as direct when in fact changes in technology have altered its nature to indirect). Davina asks the production manager about the rise in overhead costs, causing him to virtually explode: "How can I keep costs down when marketing ignores our standards specifications and insists on 23 different versions of every product? I need more specialist engineers to monitor the changes, and they don't come cheap. Also, there are completely new parts coming through from design with huge material costs; materials handling is a real headache. And the number of specials going through on small production runs continues to increase. I need many more set-ups per shift and that is skilled work, but you can't pick up that sort of skilled labor easily, so overtime is through the roof. Davina talks to the marketing manager next: "We are facing fierce competition for our bread-and- butter, high-volume lines and we just can't match the low prices in the market. However, we have successfully increased our sales of the more specialized tanks despite an increase in prices forced on us by production. So, we are meeting our overall sales targets and as we encourage this trend towards the higher margin specialist products, our profits will rise. I don't see any problem here at present, but there will be if you don't make production get control of the cost increases. English Blte Davina starts to pull the information together and gets frustrated at the inconsistencies: "We are meeting our sales targets, but production costs are rising because of the switch to specialist products. However, as these are sold at higher margins, we should be improving profits. I don't understand why profits are falling. As Davina designed the costing system, she is reluctant to admit that it is at fault and she clearly remembers the opposition she had when she last recommended changes. She no longer has her father to support her so that she decides to bring in a consultant (you) to help identify the problem and to advise on the necessary changes and on a suitable implementation policy. Davina supplies you with the following information: Budgeted Overhead Costs per month (in €): Machines 279,500 200,200 Set-up and engineering support Materials handling 119,600 Total overhead Direct labor Total manufacturing cost excluding direct materials 599,300 170,000 769,300 Further details: Budgeted Jabor rate Budgeted overhead burden* Total cost per labor-hour €42.500/ labor-hour €149.825/labor-hour €192.325 * Based on budgeted direct labor-hours of 4000. Labor-hours Machine-hours No. of set-ups No. of stores orders Standard products (high volume) Specialized products (low volume) 2500 3500 80 160 1500 3000 200 300 Total 4000 6500 280 460 Required: 1. Analyse the problem and give advice as to the advantages of switching from labor-hours to machine-hours as the overhead recovery base. 2. Show how an ABC system would change the analysis of the costs between, the standard and specialist products. 3. What are the management implications of the ABC analysis? What actions might Davina take to improve the company's profitability? 4. What are the potential problems with the implementation of the ABC system. How can Davina's fears be allayed? Tankmaster Manufacturing Company is a large manufacturer of domestic oil tanks. Since it came into existence in 1980, the company has enjoyed steady growth in both sales and profits. Davina Tankmaster, the founder's daughter, joined the company in 2010 after graduating with a degree in Accounting and Finance from Manchester University. One of her first tasks was to revise the costing system, as there was a need for more accurate product cost information to support the company's strategy of offering keen prices in a highly competitive market dominated by a few large firms. Davina had faced considerable opposition to the changes she had suggested, with several managers being willing to accept the shortcoming of the old system because they had learned to live with it. Davina won the day largely because of her father's support as the latter was convinced that learned to live with' was a euphemism for 'learned to manipulate to our own advantage'. Davina's father has now retired so that Davina is now conscious of the need to prove herself. Accordingly, the last thing she wants at present is the upset of another major change in the costing system. However, profits are below budget and the accounting is critical of the current costing system, saying that it is hopelessly out of line with the company's updated manufacturing methods and also with current theories on product costing. He says, 'We are still absorbing overheads on labor-hours and we have an absurdly high overhead absorption rate of €150 per labor-hour. We are pricing ourselves out of the market on our old established products. Product costs would be more meaningful if we absorbed overheads on machine-hours. Davina decides she must investigate. Over the past five years, overhead costs had risen to €599,300 per month, a 46% increase, while direct labor-hours have risen from €168,200 to €170,000, a negligible amount. The product processes are now largely mechanized with a relatively high level of automation. Direct labor-hours are 4000 compared with machine-hours of 6500 (it is possible that some labor is still being classed as direct when in fact changes in technology have altered its nature to indirect). Davina asks the production manager about the rise in overhead costs, causing him to virtually explode: "How can I keep costs down when marketing ignores our standards specifications and insists on 23 different versions of every product? I need more specialist engineers to monitor the changes, and they don't come cheap. Also, there are completely new parts coming through from design with huge material costs; materials handling is a real headache. And the number of specials going through on small production runs continues to increase. I need many more set-ups per shift and that is skilled work, but you can't pick up that sort of skilled labor easily, so overtime is through the roof. Davina talks to the marketing manager next: "We are facing fierce competition for our bread-and- butter, high-volume lines and we just can't match the low prices in the market. However, we have successfully increased our sales of the more specialized tanks despite an increase in prices forced on us by production. So, we are meeting our overall sales targets and as we encourage this trend towards the higher margin specialist products, our profits will rise. I don't see any problem here at present, but there will be if you don't make production get control of the cost increases. English Blte Davina starts to pull the information together and gets frustrated at the inconsistencies: "We are meeting our sales targets, but production costs are rising because of the switch to specialist products. However, as these are sold at higher margins, we should be improving profits. I don't understand why profits are falling. As Davina designed the costing system, she is reluctant to admit that it is at fault and she clearly remembers the opposition she had when she last recommended changes. She no longer has her father to support her so that she decides to bring in a consultant (you) to help identify the problem and to advise on the necessary changes and on a suitable implementation policy. Davina supplies you with the following information: Budgeted Overhead Costs per month (in €): Machines 279,500 200,200 Set-up and engineering support Materials handling 119,600 Total overhead Direct labor Total manufacturing cost excluding direct materials 599,300 170,000 769,300 Further details: Budgeted Jabor rate Budgeted overhead burden* Total cost per labor-hour €42.500/ labor-hour €149.825/labor-hour €192.325 * Based on budgeted direct labor-hours of 4000. Labor-hours Machine-hours No. of set-ups No. of stores orders Standard products (high volume) Specialized products (low volume) 2500 3500 80 160 1500 3000 200 300 Total 4000 6500 280 460 Required: 1. Analyse the problem and give advice as to the advantages of switching from labor-hours to machine-hours as the overhead recovery base. 2. Show how an ABC system would change the analysis of the costs between, the standard and specialist products. 3. What are the management implications of the ABC analysis? What actions might Davina take to improve the company's profitability? 4. What are the potential problems with the implementation of the ABC system. How can Davina's fears be allayed?

Expert Answer:

Answer rating: 100% (QA)

Required 1 Analy se the problem and give advice as to the advantages of switching from labor hours to machine hours as the overhead recovery base ANS WER The main advantage of switching from labor hou... View the full answer

Related Book For

Financial reporting, financial statement analysis and valuation a strategic perspective

ISBN: 978-0324789416

7th Edition

Authors: James M Wahlen, Stephen P Baginskl, Mark T Bradshaw

Posted Date:

Students also viewed these finance questions

-

The Appleridge Company is a large manufacturer of capital goods. (The demand for capital goods typically swings up and down a great deal between good and bad economic times.) Business has been good...

-

The Marshall Company is a large manufacturer of office furniture. The company has recently adopted lean accounting and has identified two value streamsoffice chairs and office tables. Total sales in...

-

Network Company is a large manufacturer of optical storage systems based in British Columbia. Its practical annual capacity is 7,500 units, and, for the past few years, its budgeted and actual sales...

-

The following data applies to the two unrelated companies Lloyd Ltd and Cole Ltd: All taxable and deductible temporary differences relate to the profit or loss. Assume a corporate tax rate of 30%. A....

-

Define the terms acceptance test, integration test, system test, and unit test. In what order are these tests normally performed? Who performs (or evaluates the results of) each type of test?

-

What types of decision makers are most interested in a companys liquidity and why?

-

Examine how accruals affect the current liability category.

-

Last year Clark Company issued a 10-year, 12% semiannual coupon bond at its par value of $1,000. Currently, the bond can be called in 4 years at a price of $1,060 and it sells for $1,100. a. What are...

-

One type of air blower can fill a blimp (or dirigible) in eight hours working alone, while a second blower fills the same blimp in twelve hours working alone. Working together, how long will it take...

-

On December 31, 2023, Stilton Service Companys year-end, the unadjusted trial balance included the following items: Required 1. Prepare the adjusting entry on the books of Stilton Service Company to...

-

Scenario: As an Angel Investor you have been asked to assess an entrepreneur's product and financing options. In your role as an Angel Investor you focus on one year at a time. The entrepreneur asks...

-

Katherine, a senior management executive at a magazine publisher (JBL Publishing), is negotiating with a union representative over the contract of production workers. The main issues are wage...

-

Choose an economic principle, or principles from the subject and using your own observations explain some pattern of events or behavior. The assignment does not need to contain complex terminology,...

-

Mike Brooks is an art collector in central Hobart, currently prices of local veterans' sculptures have skyrocketed. Today, Mike buys a sculpture of the first female lieutenant colonel for $795,500....

-

What are financial instruments, and how do they differ from other assets? 2. What are the main categories of financial instruments? 3. What is the difference between a debt instrument and an equity...

-

For the partially complete factorization, find the other binomial which will complete the factorization. b2-7b-30 = (b+3)(_ Answer How to enter your answer (opens in new window)

-

Reflecting on the past 10 weeks, if you had the opportunity to talk to the incoming MKT500 students, what would you tell them is the most important learning in this class? What is the one piece of adv

-

San Carlos Bank and Trust Company uses a credit-scoring system to evaluate most consumer loans that amount to more than $2,500. The key factors used in its scoring system are found at the conclusion...

-

In Integrative Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this portion of the Starbucks Integrative Case, we use the projected financial statements from...

-

Effective financial statement analysis requires an understanding of a firms economic characteristics. The relations between various financial statement items provide evidence of many of these...

-

Explain the theory behind the free cash flows valuation approach. Why are free cash flows value-relevant to common equity shareholders when they are not cash flows to those shareholders, but rather...

-

What information do the tangible capital asset turnover ratio, the average age of tangible capital assets, and the return on total assets provide users of financial statements?(Appendix)

-

What factors should be considered when selecting the amortization period for an intangible asset?(Appendix)

-

Apple a Day, Inc., and Unforgettable Edibles, Inc. are food catering businesses that operate in the same metropolitan area. Their customers include Fortune 500 companies, regional firms, and...

Study smarter with the SolutionInn App