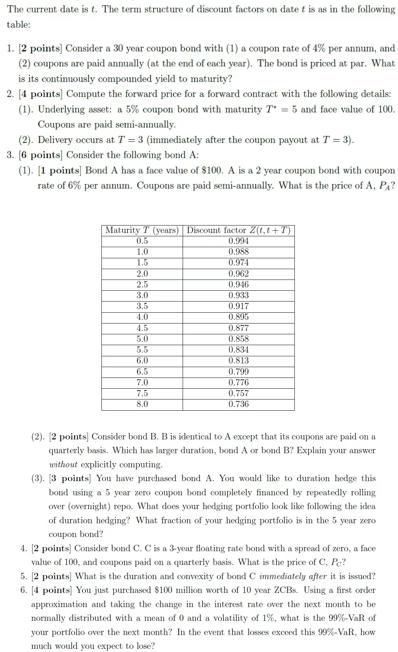

The current date is t. The term structure of discount factors on date t is as...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answers 1 Continuously compounded yield to maturity The continuously compounded yield to maturity YTM can be calculated using the following formula P C eYTM T 1 eYTM T where P is the bond price par va... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: