The WorldValue fund has value weights on asset classes and returns as given in the table...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

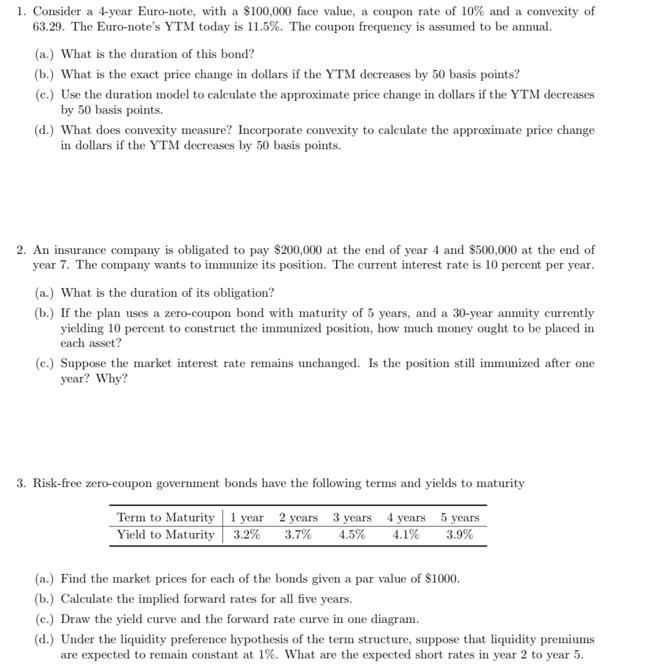

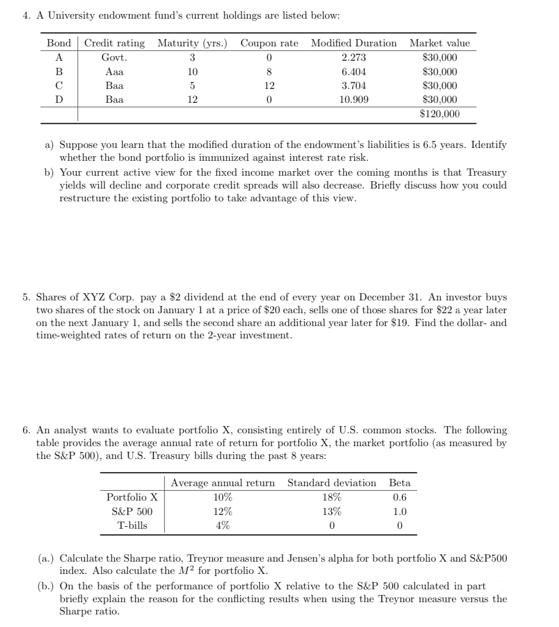

The WorldValue fund has value weights on asset classes and returns as given in the table below. There are four major asset classes: Europe, Pacific, Emerging and North America. The table also shows the weights and returns of the fund's benchmark portfolio, the World Index. World Value Fund weight (%) World Value Fund return (%) World Index weight (%) World Index return (%) Europe Pacific Emerging North America 22.2 28.0 16.3 -3.4 4.5 12.8 20.0 18.5 12.0 0.1 4.7 10.6 33.5 3.4 49.5 2.7 (a.) How did the World Value fund perform compared with the benchmark, overperformance or un- derperformance? (b.) Provide a performance attribution of World Value's return in terms of its broad asset class allo- cation and stock selection relative to the benchmark. 1. Consider a 4-year Euro-note, with a $100,000 face value, a coupon rate of 10% and a convexity of 63.29. The Euro-note's YTM today is 11.5%. The coupon frequency is assumed to be annual. (a.) What is the duration of this bond? (b.) What is the exact price change in dollars if the YTM decreases by 50 basis points? (c.) Use the duration model to calculate the approximate price change in dollars if the YTM decreases by 50 basis points. (d.) What does convexity measure? Incorporate convexity to calculate the approximate price change in dollars if the YTM decreases by 50 basis points. 2. An insurance company is obligated to pay $200,000 at the end of year 4 and $500,000 at the end of year 7. The company wants to immunize its position. The current interest rate is 10 percent per year. (a.) What is the duration of its obligation? (b.) If the plan uses a zero-coupon bond with maturity of 5 years, and a 30-year annuity currently yielding 10 percent to construct the immunized position, how much money ought to be placed in each asset? (c.) Suppose the market interest rate remains unchanged. Is the position still immunized after one year? Why? 3. Risk-free zero-coupon government bonds have the following terms and yields to maturity Term to Maturity 1 year 2 years 3 years 4 years 5 years Yield to Maturity 3.2% 3.7% 4.5% 4.1% 3.9% (a.) Find the market prices for each of the bonds given a par value of $1000. (b.) Calculate the implied forward rates for all five years. (e.) Draw the yield curve and the forward rate curve in one diagram. (d.) Under the liquidity preference hypothesis of the term structure, suppose that liquidity premiums are expected to remain constant at 1%. What are the expected short rates in year 2 to year 5. 4. A University endowment fund's current holdings are listed below: Bond Credit rating Maturity (yrs.) Coupon rate Modified Duration Market value A B C D Govt. Aaa Baa Baa 3 10 5 12 0820 12 Portfolio X S&P 500 T-bills 2.273 6.404 3.704 10.909 a) Suppose you learn that the modified duration of the endowment's liabilities is 6.5 years. Identify whether the bond portfolio is immunized against interest rate risk. b) Your current active view for the fixed income market over the coming months is that Treasury yields will decline and corporate credit spreads will also decrease. Briefly discuss how you could restructure the existing portfolio to take advantage of this view. 5. Shares of XYZ Corp. pay a $2 dividend at the end of every year on December 31. An investor buys two shares of the stock on January 1 at a price of $20 each, sells one of those shares for $22 a year later on the next January 1, and sells the second share an additional year later for $19. Find the dollar- and time-weighted rates of return on the 2-year investment. $30,000 $30,000 $30,000 $30,000 $120,000 6. An analyst wants to evaluate portfolio X, consisting entirely of U.S. common stocks. The following table provides the average annual rate of return for portfolio X, the market portfolio (as measured by the S&P 500), and U.S. Treasury bills during the past 8 years: Average annual return Standard deviation Beta 10% 0.6 12% 4% 18% 13% 0 1.0 0 (a.) Calculate the Sharpe ratio, Treynor measure and Jensen's alpha for both portfolio X and S&P500 index. Also calculate the M² for portfolio X. (b.) On the basis of the performance of portfolio X relative to the S&P 500 calculated in part briefly explain the reason for the conflicting results when using the Treynor measure versus the Sharpe ratio. The WorldValue fund has value weights on asset classes and returns as given in the table below. There are four major asset classes: Europe, Pacific, Emerging and North America. The table also shows the weights and returns of the fund's benchmark portfolio, the World Index. World Value Fund weight (%) World Value Fund return (%) World Index weight (%) World Index return (%) Europe Pacific Emerging North America 22.2 28.0 16.3 -3.4 4.5 12.8 20.0 18.5 12.0 0.1 4.7 10.6 33.5 3.4 49.5 2.7 (a.) How did the World Value fund perform compared with the benchmark, overperformance or un- derperformance? (b.) Provide a performance attribution of World Value's return in terms of its broad asset class allo- cation and stock selection relative to the benchmark. 1. Consider a 4-year Euro-note, with a $100,000 face value, a coupon rate of 10% and a convexity of 63.29. The Euro-note's YTM today is 11.5%. The coupon frequency is assumed to be annual. (a.) What is the duration of this bond? (b.) What is the exact price change in dollars if the YTM decreases by 50 basis points? (c.) Use the duration model to calculate the approximate price change in dollars if the YTM decreases by 50 basis points. (d.) What does convexity measure? Incorporate convexity to calculate the approximate price change in dollars if the YTM decreases by 50 basis points. 2. An insurance company is obligated to pay $200,000 at the end of year 4 and $500,000 at the end of year 7. The company wants to immunize its position. The current interest rate is 10 percent per year. (a.) What is the duration of its obligation? (b.) If the plan uses a zero-coupon bond with maturity of 5 years, and a 30-year annuity currently yielding 10 percent to construct the immunized position, how much money ought to be placed in each asset? (c.) Suppose the market interest rate remains unchanged. Is the position still immunized after one year? Why? 3. Risk-free zero-coupon government bonds have the following terms and yields to maturity Term to Maturity 1 year 2 years 3 years 4 years 5 years Yield to Maturity 3.2% 3.7% 4.5% 4.1% 3.9% (a.) Find the market prices for each of the bonds given a par value of $1000. (b.) Calculate the implied forward rates for all five years. (e.) Draw the yield curve and the forward rate curve in one diagram. (d.) Under the liquidity preference hypothesis of the term structure, suppose that liquidity premiums are expected to remain constant at 1%. What are the expected short rates in year 2 to year 5. 4. A University endowment fund's current holdings are listed below: Bond Credit rating Maturity (yrs.) Coupon rate Modified Duration Market value A B C D Govt. Aaa Baa Baa 3 10 5 12 0820 12 Portfolio X S&P 500 T-bills 2.273 6.404 3.704 10.909 a) Suppose you learn that the modified duration of the endowment's liabilities is 6.5 years. Identify whether the bond portfolio is immunized against interest rate risk. b) Your current active view for the fixed income market over the coming months is that Treasury yields will decline and corporate credit spreads will also decrease. Briefly discuss how you could restructure the existing portfolio to take advantage of this view. 5. Shares of XYZ Corp. pay a $2 dividend at the end of every year on December 31. An investor buys two shares of the stock on January 1 at a price of $20 each, sells one of those shares for $22 a year later on the next January 1, and sells the second share an additional year later for $19. Find the dollar- and time-weighted rates of return on the 2-year investment. $30,000 $30,000 $30,000 $30,000 $120,000 6. An analyst wants to evaluate portfolio X, consisting entirely of U.S. common stocks. The following table provides the average annual rate of return for portfolio X, the market portfolio (as measured by the S&P 500), and U.S. Treasury bills during the past 8 years: Average annual return Standard deviation Beta 10% 0.6 12% 4% 18% 13% 0 1.0 0 (a.) Calculate the Sharpe ratio, Treynor measure and Jensen's alpha for both portfolio X and S&P500 index. Also calculate the M² for portfolio X. (b.) On the basis of the performance of portfolio X relative to the S&P 500 calculated in part briefly explain the reason for the conflicting results when using the Treynor measure versus the Sharpe ratio.

Expert Answer:

Answer rating: 100% (QA)

Here are the steps to solve this portfolio evaluation problem 1 Calculate the Sharpe ratio for portf... View the full answer

Related Book For

Accounting concepts and applications

ISBN: 978-0538745482

11th Edition

Authors: Albrecht Stice, Stice Swain

Posted Date:

Students also viewed these finance questions

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Read the case study and answer the question below with a one page response. What does a SWOT analysis reveal about the overall attractiveness of Under Armours situation? Founded in 1996 by former...

-

A strange function. Consider McCarthys 91 function: public static int mcCarthy(int n) { if (n > 100) return n - 10; return mcCarthy(mcCarthy(n+11)); } Determine the value of mcCarthy(50) without...

-

The proof represented by Equation 11-54-11-61 is expressed entirely in the summation convention. Rewrite this proof in matrix notation.

-

Zoriana sells stock that she acquired in 2013 for $7,500. Her basis in the stock is $14,000. She has a $2,000 long-term capital loss carryover from 2016.

-

Currency Call Option Premiums. List the factors that affect currency call option premiums and briefly explain the relationship that exists for each. Do you think an at-the-money call option in euros...

-

1. The auditors (P&T) claimed to have no duty to Anjoorian as a shareholder of FCC. The Rhode Island Supreme Court acknowledged that the duty of accounting professionals to third parties is an open...

-

On July 15, 2017, Fishing World paid 4 million Canadian dollars (CAD) to purchased 100% of the common stock of Wilderness Fishing, a Canadian firm. The common stock of Wilderness was on the...

-

The number of bears killed in 2014 for 56 counties in Pennsylvania is shown in the frequency distribution. Construct a histogram, frequency polygon, and ogive for the data. Comment on the skewness of...

-

Question 1 Your bank is providing a $30,000,000 loan to anBBB- rated corporate client. Refer to the information below. Bank's objective - ROE22% before tax Current Loan Interest rate:8% Average...

-

What are the major internal audit activities identified in the Institute of Internal Auditors' Statement of Responsibilities of Internal Auditors!

-

Briefly describe the auditor's strategy when applying probability-proportional-tosize sampling.

-

Why is probability-proportional-to-size sampling most appropriate when an auditor desires testing for material overstatements?

-

Under what conditions would an auditor choose a nonstatistical sampling plan in substantive tests of details?

-

Briefly describe the auditor's strategy when applying mean-per-unit (MPU) estimation.

-

A$85,000 mortgage is to be amortized by making monthly payments for20 years. Interest is 7.8% compounded semi-annually for a six-yearterm.(a)Computethe size of the monthly payment.(b)Determi 2 answers

-

Compile data on consumption and expenditures for the following categories in 30 different countries: (1) food and beverages, (2) clothing and footwear, (3) housing and home operations, (4) household...

-

Pearcy Company reports the following activity during October related to its inventory of cameras: Oct. 1 Beginning inventory consisted of 8 cameras costing $100 each. 3 Purchased 12 cameras costing...

-

Boyd Companys perpetual inventory records show that the ending inventory balance should be $182,000. However, a physical count of the inventory reveals the true ending balance of inventory to be...

-

Refer to the data in PE 9-3. Assume the company borrowed $20,000 of the purchase price from a bank. Make the necessary journal entry to record this transaction. Data from PE 9-3 K. Marie Company used...

-

Determine whether the following statements are true or false. a. Full cost companies do not book AROs. b. An oral agreement to dismantle equipment and restore the environment at the end of the...

-

Problem 10 is the same as problem 9 with respect to initial measurement of the ARO liability. Now assume that Ameritecs credit standing improves over time, causing the credit-adjusted risk-free rate...

-

Exron Oil and Gas Company constructs a natural gas treatment facility in three phases. The first phase was completed and placed into service on December 31, 2017. The second phase was completed and...

Healthcare Asset Management A Complete Guide 2020 Edition 1st Edition - ISBN: 0655921133 - Free Book

Study smarter with the SolutionInn App