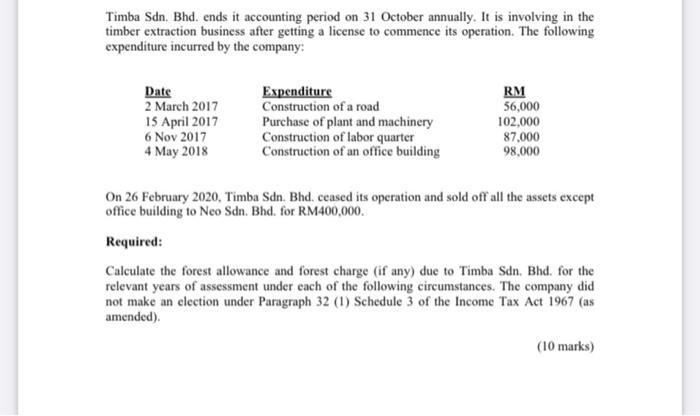

Timba Sdn. Bhd. ends it accounting period on 31 October annually. It is involving in the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

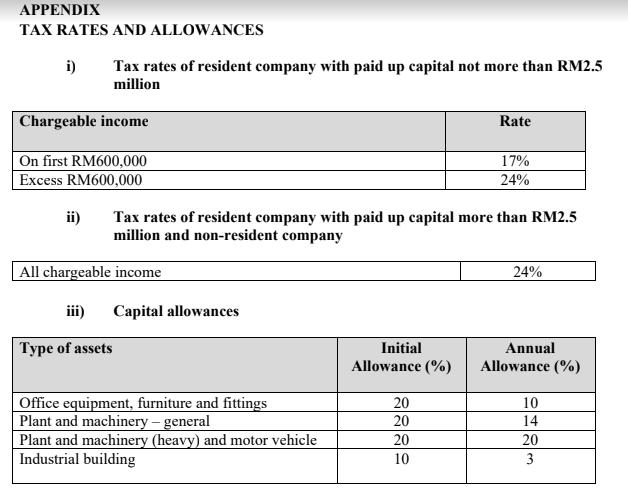

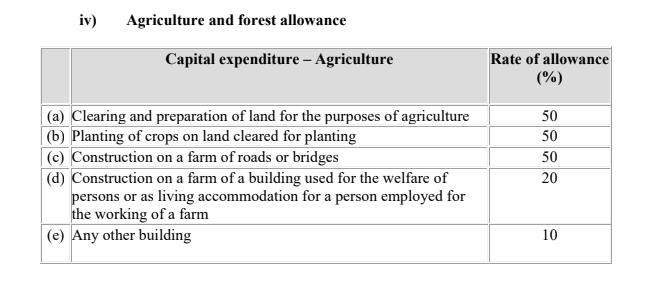

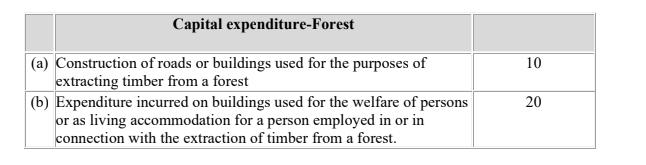

Timba Sdn. Bhd. ends it accounting period on 31 October annually. It is involving in the timber extraction business after getting a license to commence its operation. The following expenditure incurred by the company: Date 2 March 2017 15 April 2017 6 Nov 2017 4 May 2018 Expenditure Construction of a road Purchase of plant and machinery Construction of labor quarter Construction of an office building RM 56,000 102,000 87,000 98,000 On 26 February 2020, Timba Sdn. Bhd. ceased its operation and sold off all the assets except office building to Neo Sdn. Bhd. for RM400,000. Required: Calculate the forest allowance and forest charge (if any) due to Timba Sdn. Bhd. for the relevant years of assessment under each of the following circumstances. The company did not make an election under Paragraph 32 (1) Schedule 3 of the Income Tax Act 1967 (as amended). (10 marks) APPENDIX TAX RATES AND ALLOWANCES i) Tax rates of resident company with paid up capital not more than RM2.5 million Chargeable income On first RM600,000 Excess RM600,000 ii) All chargeable income Tax rates of resident company with paid up capital more than RM2.5 million and non-resident company iii) Type of assets Capital allowances Office equipment, furniture and fittings Plant and machinery - general Plant and machinery (heavy) and motor vehicle Industrial building Initial Allowance (%) Rate 20 20 20 10 17% 24% 24% Annual Allowance (%) 10 14 20 3 iv) Agriculture and forest allowance Capital expenditure - Agriculture (a) Clearing and preparation of land for the purposes of agriculture (b) Planting of crops on land cleared for planting (c) Construction on a farm of roads or bridges (d) Construction on a farm of a building used for the welfare of persons or as living accommodation for a person employed for the working of a farm (e) Any other building Rate of allowance (%) 50 50 50 20 10 Capital expenditure-Forest (a) Construction of roads or buildings used for the purposes of extracting timber from a forest (b) Expenditure incurred on buildings used for the welfare of persons or as living accommodation for a person employed in or in connection with the extraction of timber from a forest. 10 20 Timba Sdn. Bhd. ends it accounting period on 31 October annually. It is involving in the timber extraction business after getting a license to commence its operation. The following expenditure incurred by the company: Date 2 March 2017 15 April 2017 6 Nov 2017 4 May 2018 Expenditure Construction of a road Purchase of plant and machinery Construction of labor quarter Construction of an office building RM 56,000 102,000 87,000 98,000 On 26 February 2020, Timba Sdn. Bhd. ceased its operation and sold off all the assets except office building to Neo Sdn. Bhd. for RM400,000. Required: Calculate the forest allowance and forest charge (if any) due to Timba Sdn. Bhd. for the relevant years of assessment under each of the following circumstances. The company did not make an election under Paragraph 32 (1) Schedule 3 of the Income Tax Act 1967 (as amended). (10 marks) APPENDIX TAX RATES AND ALLOWANCES i) Tax rates of resident company with paid up capital not more than RM2.5 million Chargeable income On first RM600,000 Excess RM600,000 ii) All chargeable income Tax rates of resident company with paid up capital more than RM2.5 million and non-resident company iii) Type of assets Capital allowances Office equipment, furniture and fittings Plant and machinery - general Plant and machinery (heavy) and motor vehicle Industrial building Initial Allowance (%) Rate 20 20 20 10 17% 24% 24% Annual Allowance (%) 10 14 20 3 iv) Agriculture and forest allowance Capital expenditure - Agriculture (a) Clearing and preparation of land for the purposes of agriculture (b) Planting of crops on land cleared for planting (c) Construction on a farm of roads or bridges (d) Construction on a farm of a building used for the welfare of persons or as living accommodation for a person employed for the working of a farm (e) Any other building Rate of allowance (%) 50 50 50 20 10 Capital expenditure-Forest (a) Construction of roads or buildings used for the purposes of extracting timber from a forest (b) Expenditure incurred on buildings used for the welfare of persons or as living accommodation for a person employed in or in connection with the extraction of timber from a forest. 10 20

Expert Answer:

Related Book For

Modern Advanced Accounting in Canada

ISBN: 978-1259087554

7th edition

Authors: Hilton Murray, Herauf Darrell

Posted Date:

Students also viewed these accounting questions

-

Paragraph 33(1) of the Malaysian Income Tax Act 1967 provides the general deduction test for a business. A summary of paragraph 33(1) is as follows: " Subject to this Act, the adjusted income of a...

-

Under what circumstances is an assets depreciation amount not included in total in a companys current income statement?

-

If its accounting period ends December 31, would a company be using a natural business year or a fiscal year?

-

I have this data frame with the years and values, can you make a model to predict the value of meats,fish,fruits and vegetables and grains? based on the current values of the table and historical...

-

Titus Manin Black Limited is trying to determine the value of its ending inventory as of February 28, 2012, the companys year-end. The following transactions occurred, and the accountant asked your...

-

Various foreign currency-denominated transactions settled in subsequent year ATV had two foreign currency transactions during December 2016, as follows: December 12 Purchased electronic parts on...

-

\(\sqrt{19}\) Identify each number as a natural number, an integer, a rational number, or a real number.

-

Creation Company produces gadgets for the coveted small appliance market. The following data reflect activity for the year 2014: Costs incurred: Purchases of direct materials (net) on credit...... $...

-

Problem 27-23 (AICPA Adapted) Patterson Company provided the following information on January 1, 2020: Vehicle cost 5,000,000 Useful life in years 5 Useful life in miles 100,000 Residual value...

-

Below are shown three different crystallographic planes for a unit cell of some hypothetical metal. The circles represent atoms: (a) To what crystal system does the unit cell belong? (b) What would...

-

Figure 1 4 - 1 1 - 2 . png Refer to Figure 1 4 - 1 . Which of the four prices corresponds to a perfectly competitive firm earning negative economic profits in the short run and shutting down? Group...

-

To achieve desired consumer behaviour and to build profitable relationships in defined target markets, there are five (5) alternative concepts also referred to as the Evolution of Marketing) under...

-

The price elasticity of demand for coke is -0.24. The price elasticity of supply for coke is 0.38. The income elasticity of demand for coke is 0.8. The equilibrium quantity is 39.95 metric tons,...

-

A 4.5 kg backpack slides across the classroom floor with some positive velocity. There is a coefficient of sliding friction of 0.24 between the backpack and the floor. What force of friction will act...

-

How do emergent properties and self-organization phenomena manifest within complex biological systems, and what are the implications of these organizational principles for understanding organismal...

-

On June 3 0 , 2 0 2 5 , Michael Jones Company issued $ 3 , 4 9 3 , 0 0 0 . 0 0 face value of 1 4 % , 2 0 - year bonds at $ 4 , 0 1 8 , 5 6 0 . 0 0 , a yield of 1 2 % . Jones uses the effective -...

-

1. Do you think that geography is a valid reason to favor one language over another?

-

Ex. (17): the vector field F = x i-zj + yz k is defined over the volume of the cuboid given by 0x a,0 y b, 0zc, enclosing the surface S. Evaluate the surface integral ff, F. ds?

-

Access the 2011 financial statements for Atco Ltd. by going to investor relations section of the companys website. Answer the same questions as in Problem 1. For each question, indicate where in the...

-

The comparative consolidated income statements of a parent and its 75%-owned subsidiary were prepared incorrectly as at December 31 and are shown in the following table. The following items were...

-

Summarized below are the balances in the accumulated unrealized exchange accounts in the consolidated balance sheets of four companies at the end of two successive years. Each company reported in...

-

On December 1, 2017, Sizzler Foods, a U.S. company, purchased merchandise from a Hong Kong supplier at a price of HK\($10,000,000,\) payable in three months in Hong Kong dollars. To hedge its exposed...

-

On March 15, 2017, Hunt Brands, a U.S. company, purchased merchandise from a South African company at a price of R1,000,000, payable in two months in rands. To hedge its exposed liability position,...

-

On September 3, 2017, Robin Franchises, a U.S. company, sold merchandise to a franchisee in the U.K., at a price of 8,000,000, payable in three months in pounds. To hedge its exposed asset position,...

Study smarter with the SolutionInn App