Use the data contained in the case to estimate the postmerger cash flows for 2018 through...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

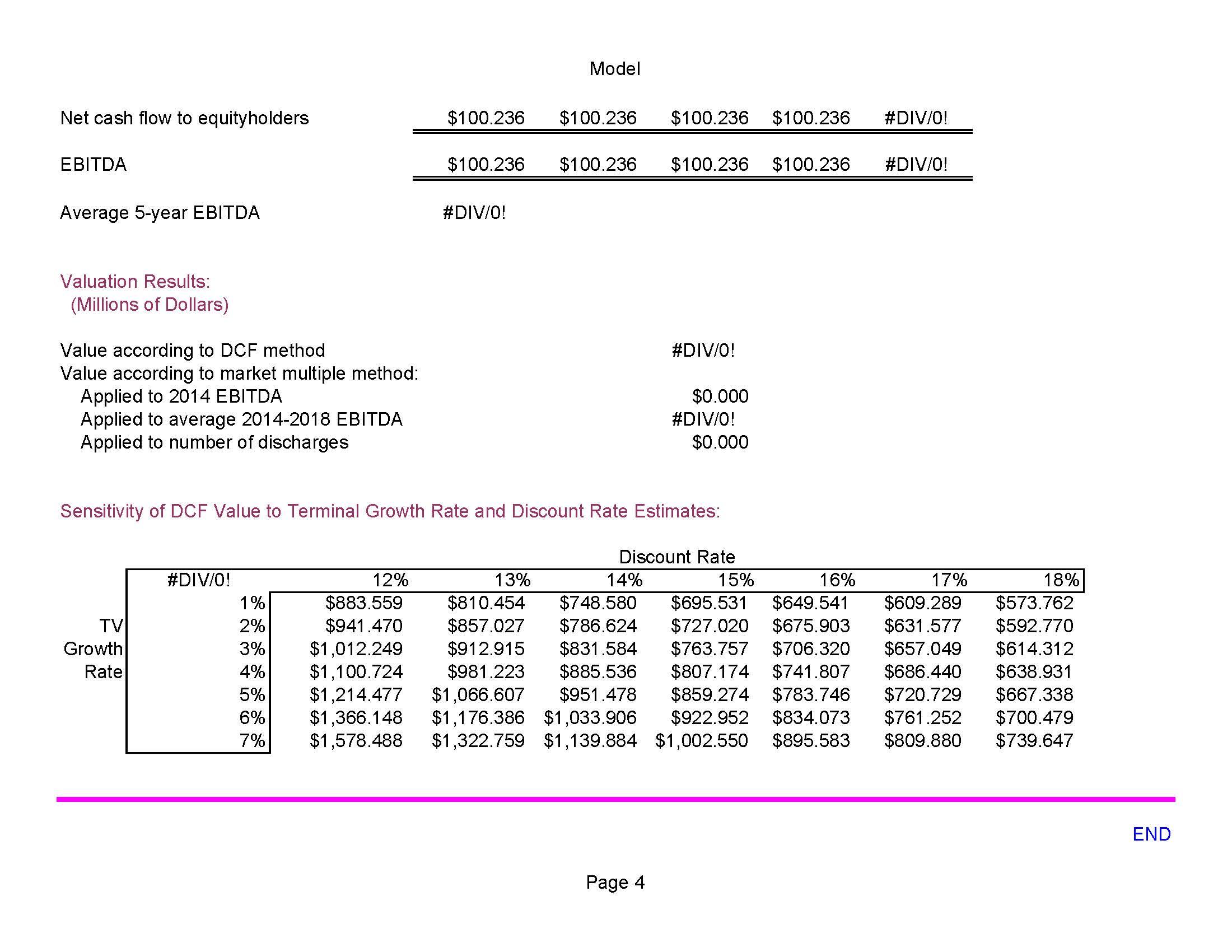

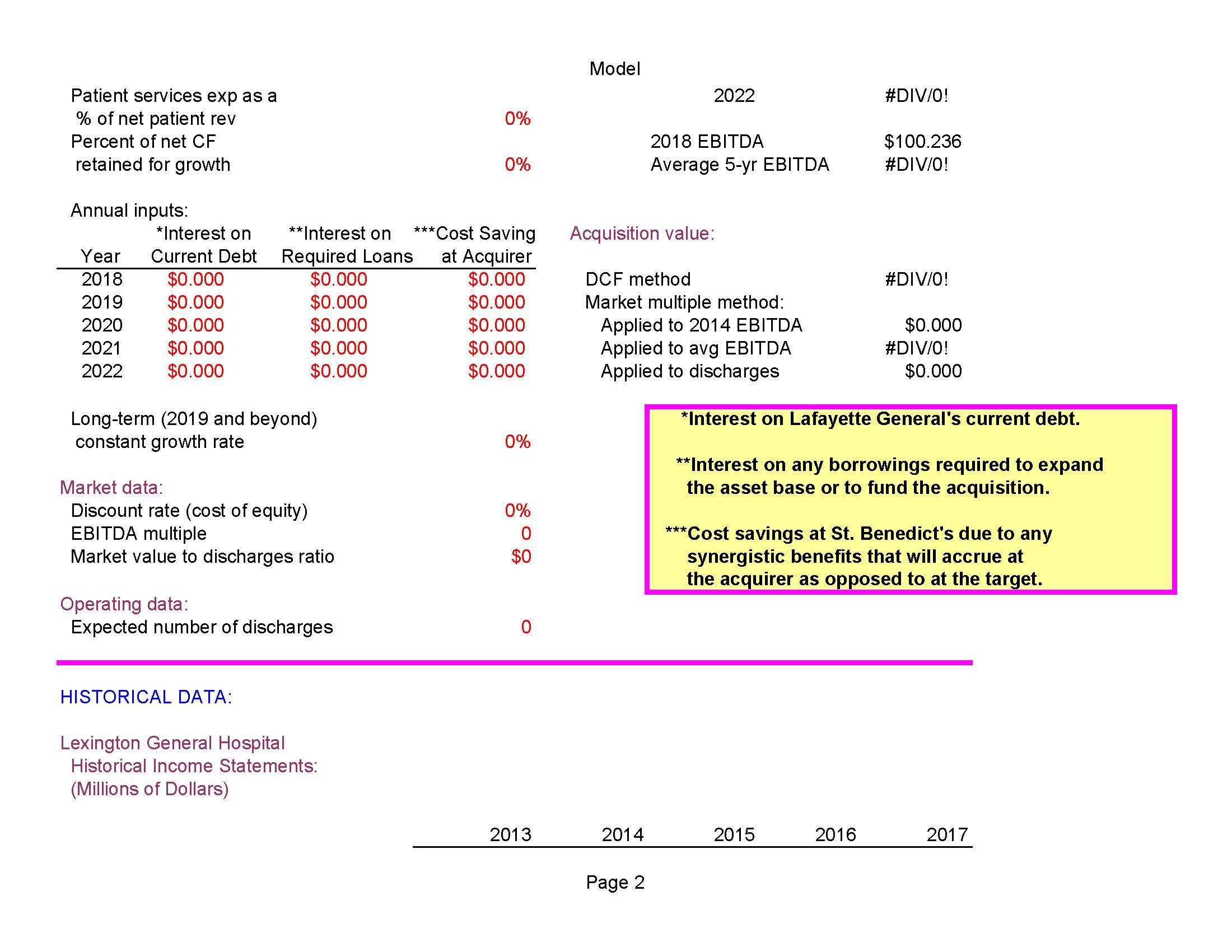

Use the data contained in the case to estimate the postmerger cash flows for 2018 through 2022 assuming that Lafayette General Hospital is acquired by St. Benedict's Teaching Hospital. You have very limited data on which to base your forecasts. The key is to make supportable assumptions about the potential synergies that can be obtained from the merger. Also, any cost savings to St. Benedict's that result from the merger must be included in the analysis. (Hint: Use embedded interest expense in your forecast, but do not include any interest to fund the acquisition.) Net cash flow to equityholders EBITDA Average 5-year EBITDA Valuation Results: (Millions of Dollars) Value according to DCF method Value according to market multiple method: Applied to 2014 EBITDA Applied to average 2014-2018 EBITDA Applied to number of discharges TV Growth Rate #DIV/0! 1% 2% 3% 4% 5% 6% 7% Model $100.236 $100.236 $100.236 $100.236 #DIV/0! $100.236 $100.236 $100.236 $100.236 #DIV/0! #DIV/0! Sensitivity of DCF Value to Terminal Growth Rate and Discount Rate Estimates: #DIV/0! $0.000 #DIV/0! $0.000 Page 4 17% 18% $573.762 12% $883.559 $941.470 $1,012.249 Discount Rate 13% 14% 15% 16% $810.454 $748.580 $695.531 $649.541 $609.289 $857.027 $786.624 $727.020 $675.903 $631.577 $912.915 $831.584 $763.757 $706.320 $657.049 $614.312 $885.536 $686.440 $638.931 $1,214.477 $1,066.607 $951.478 $859.274 $783.746 $720.729 $667.338 $1,366.148 $1,176.386 $1,033.906 $922.952 $834.073 $761.252 $700.479 $1,578.488 $1,322.759 $1,139.884 $1,002.550 $895.583 $809.880 $739.647 $592.770 $1,100.724 $981.223 $807.174 $741.807 END Inpatient revenue Outpatient revenue Net patient service revenue Nonoperating revenue Total revenues Patient services expenses Interest expense Depreciation Total expenses Net income MODEL-GENERATED DATA: Inpatient revenue Outpatient revenue Net patient service revenue Nonoperating revenue $42.472 28.314 $70.786 1.922 $72.708 $60.245 3.045 3.466 $66.756 Lexington General Hospital Pro Forma (Forecasted) Cash Flow Statements: (Millions of Dollars) Total revenues Patient services expenses Interest expense Total expenses Net operating cash flow Cost savings at teaching (other) hospital Growth retentions Terminal value $5.952 2018 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 Model $46.014 30.676 $76.690 1.515 $78.205 $73.858 3.147 3.689 $80.694 ($2.489) 2019 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 Page 3 $53.410 $58.650 35.606 39.100 $89.016 $97.750 1.367 1.725 $90.383 $99.475 $81.525 $90.645 3.093 4.395 $89.013 $1.370 2020 3.002 4.258 $97.905 2021 $59.513 $59.513 39.675 39.675 $99.188 $99.188 1.048 1.048 $100.236 $100.236 $0.00 $0.00 0.000 0.000 $0.000 $0.000 $100.236 $100.236 0.000 0.000 $1.570 0.000 0.000 $59.513 39.675 $99.188 1.048 $100.236 $89.505 2.980 6.031 $98.516 $1.720 2022 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 #DIV/0! Patient services exp as a % of net patient rev Percent of net CF retained for growth Annual inputs: *Interest on Year Current Debt 2018 2019 2020 2021 2022 $0.000 $0.000 $0.000 $0.000 $0.000 **Interest on Required Loans $0.000 $0.000 $0.000 $0.000 $0.000 Long-term (2019 and beyond) constant growth rate Market data: Discount rate (cost of equity) EBITDA multiple Market value to discharges ratio HISTORICAL DATA: Operating data: Expected number of discharges Lexington General Hospital Historical Income Statements: (Millions of Dollars) 0% *** 0% *Cost Saving at Acquirer $0.000 $0.000 $0.000 $0.000 $0.000 0% 0% 0 $0 0 2013 Model Acquisition value: 2014 2022 2018 EBITDA Average 5-yr EBITDA DCF method Market multiple method: Applied to 2014 EBITDA Applied to avg EBITDA Applied to discharges Page 2 *** #DIV/0! 2015 $100.236 #DIV/0! 2016 #DIV/0! $0.000 *Interest on Lafayette General's current debt. **Interest on any borrowings required to expand the asset base or to fund the acquisition. #DIV/0! $0.000 *Cost savings at St. Benedict's due to any synergistic benefits that will accrue at the acquirer as opposed to at the target. 2017 Model CASE 30 ST. JOSEPH'S TEACHING HOSPITAL: Merger Analysis Model with Questions, Student Version This case consists of a valuation analysis on a 400-bed acute care hospital. The model uses both discounted cash flow (DCF) and market multiple methodologies for the valuation. The DCF method focuses on cash flows to equityholders. The INPUT DATA section of the model contains key assumptions needed to generate the pro forma (forecasted) cash flow statements. In addition, historical data used in the forecasting process is contained in its own section. The model consists of a complete base case analysis--no changes need to be made to the existing MODEL-GENERATED DATA section. However, values in the INPUT DATA section of the student spreadsheet have been replaced by zeros. Students must select appropriate input values and enter them into the cells with values colored red. After this is done, any error cells will be corrected and the base case solution will appear. The KEY OUTPUT section includes the most important output from the MODEL-GENERATED DATA section. INPUT DATA: (millions of $) Cash flow data: Growth in revenues (2018-2022): Inpatient Outpatient Nonoperating 0% 0% 0% KEY OUTPUT: (millions of $) Pro forma (forecasted) net cash flows: 2018 2019 2020 2021 Page 1 $100.236 $100.236 $100.236 $100.236 Use the data contained in the case to estimate the postmerger cash flows for 2018 through 2022 assuming that Lafayette General Hospital is acquired by St. Benedict's Teaching Hospital. You have very limited data on which to base your forecasts. The key is to make supportable assumptions about the potential synergies that can be obtained from the merger. Also, any cost savings to St. Benedict's that result from the merger must be included in the analysis. (Hint: Use embedded interest expense in your forecast, but do not include any interest to fund the acquisition.) Net cash flow to equityholders EBITDA Average 5-year EBITDA Valuation Results: (Millions of Dollars) Value according to DCF method Value according to market multiple method: Applied to 2014 EBITDA Applied to average 2014-2018 EBITDA Applied to number of discharges TV Growth Rate #DIV/0! 1% 2% 3% 4% 5% 6% 7% Model $100.236 $100.236 $100.236 $100.236 #DIV/0! $100.236 $100.236 $100.236 $100.236 #DIV/0! #DIV/0! Sensitivity of DCF Value to Terminal Growth Rate and Discount Rate Estimates: #DIV/0! $0.000 #DIV/0! $0.000 Page 4 17% 18% $573.762 12% $883.559 $941.470 $1,012.249 Discount Rate 13% 14% 15% 16% $810.454 $748.580 $695.531 $649.541 $609.289 $857.027 $786.624 $727.020 $675.903 $631.577 $912.915 $831.584 $763.757 $706.320 $657.049 $614.312 $885.536 $686.440 $638.931 $1,214.477 $1,066.607 $951.478 $859.274 $783.746 $720.729 $667.338 $1,366.148 $1,176.386 $1,033.906 $922.952 $834.073 $761.252 $700.479 $1,578.488 $1,322.759 $1,139.884 $1,002.550 $895.583 $809.880 $739.647 $592.770 $1,100.724 $981.223 $807.174 $741.807 END Inpatient revenue Outpatient revenue Net patient service revenue Nonoperating revenue Total revenues Patient services expenses Interest expense Depreciation Total expenses Net income MODEL-GENERATED DATA: Inpatient revenue Outpatient revenue Net patient service revenue Nonoperating revenue $42.472 28.314 $70.786 1.922 $72.708 $60.245 3.045 3.466 $66.756 Lexington General Hospital Pro Forma (Forecasted) Cash Flow Statements: (Millions of Dollars) Total revenues Patient services expenses Interest expense Total expenses Net operating cash flow Cost savings at teaching (other) hospital Growth retentions Terminal value $5.952 2018 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 Model $46.014 30.676 $76.690 1.515 $78.205 $73.858 3.147 3.689 $80.694 ($2.489) 2019 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 Page 3 $53.410 $58.650 35.606 39.100 $89.016 $97.750 1.367 1.725 $90.383 $99.475 $81.525 $90.645 3.093 4.395 $89.013 $1.370 2020 3.002 4.258 $97.905 2021 $59.513 $59.513 39.675 39.675 $99.188 $99.188 1.048 1.048 $100.236 $100.236 $0.00 $0.00 0.000 0.000 $0.000 $0.000 $100.236 $100.236 0.000 0.000 $1.570 0.000 0.000 $59.513 39.675 $99.188 1.048 $100.236 $89.505 2.980 6.031 $98.516 $1.720 2022 $59.513 39.675 $99.188 1.048 $100.236 $0.00 0.000 $0.000 $100.236 0.000 0.000 #DIV/0! Patient services exp as a % of net patient rev Percent of net CF retained for growth Annual inputs: *Interest on Year Current Debt 2018 2019 2020 2021 2022 $0.000 $0.000 $0.000 $0.000 $0.000 **Interest on Required Loans $0.000 $0.000 $0.000 $0.000 $0.000 Long-term (2019 and beyond) constant growth rate Market data: Discount rate (cost of equity) EBITDA multiple Market value to discharges ratio HISTORICAL DATA: Operating data: Expected number of discharges Lexington General Hospital Historical Income Statements: (Millions of Dollars) 0% *** 0% *Cost Saving at Acquirer $0.000 $0.000 $0.000 $0.000 $0.000 0% 0% 0 $0 0 2013 Model Acquisition value: 2014 2022 2018 EBITDA Average 5-yr EBITDA DCF method Market multiple method: Applied to 2014 EBITDA Applied to avg EBITDA Applied to discharges Page 2 *** #DIV/0! 2015 $100.236 #DIV/0! 2016 #DIV/0! $0.000 *Interest on Lafayette General's current debt. **Interest on any borrowings required to expand the asset base or to fund the acquisition. #DIV/0! $0.000 *Cost savings at St. Benedict's due to any synergistic benefits that will accrue at the acquirer as opposed to at the target. 2017 Model CASE 30 ST. JOSEPH'S TEACHING HOSPITAL: Merger Analysis Model with Questions, Student Version This case consists of a valuation analysis on a 400-bed acute care hospital. The model uses both discounted cash flow (DCF) and market multiple methodologies for the valuation. The DCF method focuses on cash flows to equityholders. The INPUT DATA section of the model contains key assumptions needed to generate the pro forma (forecasted) cash flow statements. In addition, historical data used in the forecasting process is contained in its own section. The model consists of a complete base case analysis--no changes need to be made to the existing MODEL-GENERATED DATA section. However, values in the INPUT DATA section of the student spreadsheet have been replaced by zeros. Students must select appropriate input values and enter them into the cells with values colored red. After this is done, any error cells will be corrected and the base case solution will appear. The KEY OUTPUT section includes the most important output from the MODEL-GENERATED DATA section. INPUT DATA: (millions of $) Cash flow data: Growth in revenues (2018-2022): Inpatient Outpatient Nonoperating 0% 0% 0% KEY OUTPUT: (millions of $) Pro forma (forecasted) net cash flows: 2018 2019 2020 2021 Page 1 $100.236 $100.236 $100.236 $100.236

Expert Answer:

Answer rating: 100% (QA)

ANSWER To estimate the postmerger cash flows for 2018 through 2022 we need to make several assumptions about the potential synergies that can be obtained from the merger and any cost savings that can ... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

The patient base of Lexington County, South Carolina, is currently served by three hospitals: (1) St. Josephs Teaching Hospital, a not-for-profit, university- related hospital with 525 beds; (2)...

-

List three specific parts of the Case Guide, Objectives and Strategy Section (See below) that you had the most difficulty understanding. Describe your current understanding of these parts. Provide...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

What future directions may be interesting for comparative studies in corporate governance?

-

Assume a cyclic machine that exchanges 6 kW with a 250oC reservoir and has a. Q.L = 0 kW, W. = 6 kW b. Q.L = 6 kW, W. = 0 kW and Q.L is exchanged with a 30oC ambient. What can you say about the...

-

Whilst preparing its financial statements for the year to 30 June 2018, a company discovers that (owing to an accounting error) the sales figure for the year to 30 June 2017 had been understated by...

-

Many groups have treasury policies that use hedging of net positions. They would look at their group-wide exposure in, e.g. foreign currency and then take forward contracts to cover the position....

-

When gas expands in a cylinder with radius r, the pressure at any given time is a function of the volume: P = P(V) . The force exerted by the gas on the piston (see the figure) is the product of the...

-

If the radius of a circle is 6 Inches, then the area of a sector bounded by a 100 arc is Round the answer to the nearest tenth of a square Inch. square Inches

-

Brian and Corrine Lee are married taxpayers filing jointly. They live in the home they own, located at 3301 Pacific Coast Hwy., Laguna Beach, CA 92651. Brian is an optometrist who owns his business;...

-

In the context of consumer goods, match the different percentages of debt owed by a debtor (left column) to the actions a creditor can take based on them (right column). Drag and drop application. If...

-

Wear Ever is expanding and needs $12.6 million to help fund this growth. The firm estimates it can sell new shares of stock for $32.50 a share. It also estimates it will cost an additional $340,000...

-

Pilgrim Corporation processes frozen turkeys. The company has not been pleased with its profit margin per product because it appears that the high value items have too few costs assigned to them,...

-

Darrell Porter was the manager of a professional minor-league baseball team. During the past season, the team had a won-lost record of 71-60. At the end of the season Porter wondered what he could...

-

A spring-mass system consists of a spring of stiffness 350 N/m. The mass is 0.35 kg. The mass is displaced 20 mm beyond the equilibrium position and released. The damping coefficient is 14 Ns/m....

-

Pappy's Toys makes two models of a metal toyStandard and DeLuxe. Both models are produced on a single machine. The price and costs of the two models appear as follows. StandardDeLuxePrice per...

-

Mountain, Inc., purchased a new automobile on October 1 of the 2020 at a cost of $145,000. The automobile's estimated useful life at the time of the purchase was 4 years, and its residual value was...

-

What is the role of business risk analysis in the audit planning process?

-

Apply the economic attributes framework discussed in the chapter to the specialty retailing apparel industry, which includes such firms as Gap, Limited Brands, and Abercrombie & Fitch.

-

Prime Contractors (Prime) is a privately owned company that contracts with the U.S. government to provide various services under multiyear (usually five-year) contracts. Its principal services are as...

-

Assume Walmart acquires a tract of land on January 1, 2016, for $100,000 cash. On December 31, 2016, the current market value of the land is $150,000. On December 31, 2017, the current market value...

-

A retailer purchases a can of soup for 24 cents and sells it for 36 cents. Calculate the markup as a percentage of cost and as a percentage of selling price.

-

The characteristics of services affect the development of marketing mixes for services. Choose a specific service and explain how each marketing mix element could be affected by these service...

-

Identify a familiar product that recently was modified, categorize the modification (quality, functional, or aesthetic), and describe how you would have modified it differently.

Study smarter with the SolutionInn App