Wealth Management Part 2: A Financial and Taxation Case Study Question 2: Case study You are...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

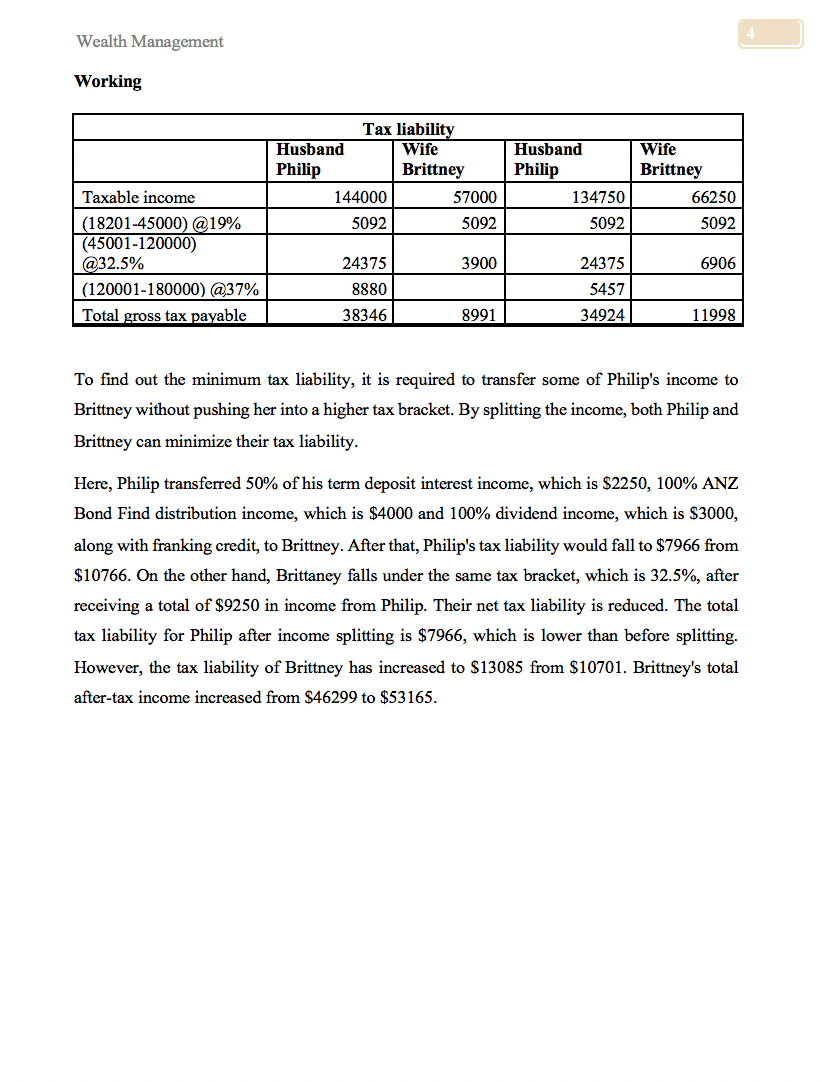

Wealth Management Part 2: A Financial and Taxation Case Study Question 2: Case study You are a financial adviser, and the following information is an extract of data you gathered as part of fact-finding during an initial client consultation for a married couple, Philip (aged 56) and Brittney (aged 55) McVey. The couple attended university together, started their careers simultaneously, and married within four years of graduating from university. Brittney left her well-established banking job upon the birth of her first child. The couple has three children. After the youngest child completed 10th grade, Brittney re-entered the workforce as a human resources administrator. All three children are now financially independent and successful in their careers. Philip is the local head of an international distribution firm. Brittney is concerned about her superannuation balance and is anxious to find ways to increase it. The couple would like advice on how to reduce their tax liability in the future. Income and Expenditure for the year ended 30th June 2024: Income type (ownership) Amount Gross Salary- (Brittney) Gross Salary- (Philip) ANZ Term Depost Interest (Philip) ANZ Bond Fund- Distribution (Philip) $57,000.00 $135,000.00 $4,500.00 $4,000.00 $2,100.00 Caltex Dividend- Dividend $1.10 per share- (Philip) $900 Imputation Credit Expenses Amount Food $13,500.00 Clothing/Haircuts/Beauty Medical/Dental Treatment Deductible gift recipient (DGR) Charity (Philip) Gifts Birthdays/Christmas Total $4,500.00 $2,500.00 $2,500.00 $5,000.00 $88,235.00 Wealth Management Asset and Liabilities as of June 30th, 2024 Assets (Ownership) Home and Contents (Joint) Cars (Two- Joint) ANZ Term Deposit (Philip) Investments: ANZ Bond Fund- (Philip) Caltex Shares (Philip) Current valuation $850,000.00 $70,000.00 $100,000.00 $80,000.00 $50,000.00 Superannuation- (Philip) Superannuation- (Brittney) Liability (Ownership) Mortgage (Join) Credit cards (Joint) (Includes the annual interest cost) PAYG (Philip) $31,000.00 $660,000.00 $135,000.00 Current valuation $330,000.00 $6,000.00 Required: A. Calculate Philip and Brittney's after-tax income for the year ended June 30th, 2024. Explain how Philip and Brittney could reduce their tax liability by splitting their income. Show the effect this strategy would have had if they had split income for the tax year ended. Wealth Management After tax income of Philip and Brittney for the year ended June 30 2024. Husband Philip Wife Brittney Assessable income Gross Salary Term deposit interest 135000 4500 57000 0 ANZ Bond Fund distribution 4000 Dividend income 3000 Less: Allowable deductions Gift Recipient (DGR) Charity 2500 Taxable Income 144000 57000 Tax rate applicable Gross tax payable 38346 8991 Plus: Medicare Levy 2880 1140 Plus: Medicare Levy Surcharge 1440 570 Less: Non-refundable tax offset Less: Refundable tax offset 900 0 Net tax expenses 41766 10701 Less: PAYG Credit 31000 0 Net tax payable (Refund) 10766 10701 After Tax Income 133234 46299 Note There is a 2% Medicare levy charged on net taxable income. The family's income is more than $186000. Therefore, Medicare levy a surcharge of 1% applied on their taxable income (Australian Taxation Office 2024). Wealth Management There is no non-refundable tax offset. Working Taxable income (18201-45000) @19% (45001-120000) @32.5% (120001-180000) @37% Total gross tax payable Tax liability Husband Philip Wife Brittney 144000 57000 5092 5092 24375 3900 8880 38346 8991 After tax income of Philip and Brittney for the year ended June 30 2024 After splinting. Before Splitting Wife After Splitting Wife Husband Husband Philip Brittney Philip Brittney Assessable income Gross Salary 135000 57000 135000 57000 Term deposit interest 4500 0 2250 2250 ANZ Bond Fund distribution 4000 0 4000 Dividend income 3000 0 3000 Less: Allowable deductions Gift Recipient (DGR) Charity 2500 2500 0 Taxable Income 3 144000 57000 134750 66250 Tax rate applicable Gross tax payable 38346 8991 34924 11998 Plus: Medicare Levy 2880 1140 2695 1325 Plus: Medicare Levy Surcharge 1440 570 1347.5 662.5 Less: Non-refundable tax offset Less: Refundable tax offset 900 0 0 Net tax expenses 41766 10701 38966 900 13085 Less: PAYG Credit 31000 0 31000 0 Net tax payable (Refund) 10766 10701 7966 13085 After Tax Income 133234 46299 126784 53165 Wealth Management Working Tax liability Husband Philip Wife Brittney Husband Philip Wife Brittney Taxable income 144000 57000 134750 66250 (18201-45000)@19% 5092 5092 5092 5092 (45001-120000) @32.5% 24375 3900 24375 6906 (120001-180000) @37% 8880 5457 Total gross tax payable 38346 8991 34924 11998 To find out the minimum tax liability, it is required to transfer some of Philip's income to Brittney without pushing her into a higher tax bracket. By splitting the income, both Philip and Brittney can minimize their tax liability. Here, Philip transferred 50% of his term deposit interest income, which is $2250, 100% ANZ Bond Find distribution income, which is $4000 and 100% dividend income, which is $3000, along with franking credit, to Brittney. After that, Philip's tax liability would fall to $7966 from $10766. On the other hand, Brittaney falls under the same tax bracket, which is 32.5%, after receiving a total of $9250 in income from Philip. Their net tax liability is reduced. The total tax liability for Philip after income splitting is $7966, which is lower than before splitting. However, the tax liability of Brittney has increased to $13085 from $10701. Brittney's total after-tax income increased from $46299 to $53165. Wealth Management Part 2: A Financial and Taxation Case Study Question 2: Case study You are a financial adviser, and the following information is an extract of data you gathered as part of fact-finding during an initial client consultation for a married couple, Philip (aged 56) and Brittney (aged 55) McVey. The couple attended university together, started their careers simultaneously, and married within four years of graduating from university. Brittney left her well-established banking job upon the birth of her first child. The couple has three children. After the youngest child completed 10th grade, Brittney re-entered the workforce as a human resources administrator. All three children are now financially independent and successful in their careers. Philip is the local head of an international distribution firm. Brittney is concerned about her superannuation balance and is anxious to find ways to increase it. The couple would like advice on how to reduce their tax liability in the future. Income and Expenditure for the year ended 30th June 2024: Income type (ownership) Amount Gross Salary- (Brittney) Gross Salary- (Philip) ANZ Term Depost Interest (Philip) ANZ Bond Fund- Distribution (Philip) $57,000.00 $135,000.00 $4,500.00 $4,000.00 $2,100.00 Caltex Dividend- Dividend $1.10 per share- (Philip) $900 Imputation Credit Expenses Amount Food $13,500.00 Clothing/Haircuts/Beauty Medical/Dental Treatment Deductible gift recipient (DGR) Charity (Philip) Gifts Birthdays/Christmas Total $4,500.00 $2,500.00 $2,500.00 $5,000.00 $88,235.00 Wealth Management Asset and Liabilities as of June 30th, 2024 Assets (Ownership) Home and Contents (Joint) Cars (Two- Joint) ANZ Term Deposit (Philip) Investments: ANZ Bond Fund- (Philip) Caltex Shares (Philip) Current valuation $850,000.00 $70,000.00 $100,000.00 $80,000.00 $50,000.00 Superannuation- (Philip) Superannuation- (Brittney) Liability (Ownership) Mortgage (Join) Credit cards (Joint) (Includes the annual interest cost) PAYG (Philip) $31,000.00 $660,000.00 $135,000.00 Current valuation $330,000.00 $6,000.00 Required: A. Calculate Philip and Brittney's after-tax income for the year ended June 30th, 2024. Explain how Philip and Brittney could reduce their tax liability by splitting their income. Show the effect this strategy would have had if they had split income for the tax year ended. Wealth Management After tax income of Philip and Brittney for the year ended June 30 2024. Husband Philip Wife Brittney Assessable income Gross Salary Term deposit interest 135000 4500 57000 0 ANZ Bond Fund distribution 4000 Dividend income 3000 Less: Allowable deductions Gift Recipient (DGR) Charity 2500 Taxable Income 144000 57000 Tax rate applicable Gross tax payable 38346 8991 Plus: Medicare Levy 2880 1140 Plus: Medicare Levy Surcharge 1440 570 Less: Non-refundable tax offset Less: Refundable tax offset 900 0 Net tax expenses 41766 10701 Less: PAYG Credit 31000 0 Net tax payable (Refund) 10766 10701 After Tax Income 133234 46299 Note There is a 2% Medicare levy charged on net taxable income. The family's income is more than $186000. Therefore, Medicare levy a surcharge of 1% applied on their taxable income (Australian Taxation Office 2024). Wealth Management There is no non-refundable tax offset. Working Taxable income (18201-45000) @19% (45001-120000) @32.5% (120001-180000) @37% Total gross tax payable Tax liability Husband Philip Wife Brittney 144000 57000 5092 5092 24375 3900 8880 38346 8991 After tax income of Philip and Brittney for the year ended June 30 2024 After splinting. Before Splitting Wife After Splitting Wife Husband Husband Philip Brittney Philip Brittney Assessable income Gross Salary 135000 57000 135000 57000 Term deposit interest 4500 0 2250 2250 ANZ Bond Fund distribution 4000 0 4000 Dividend income 3000 0 3000 Less: Allowable deductions Gift Recipient (DGR) Charity 2500 2500 0 Taxable Income 3 144000 57000 134750 66250 Tax rate applicable Gross tax payable 38346 8991 34924 11998 Plus: Medicare Levy 2880 1140 2695 1325 Plus: Medicare Levy Surcharge 1440 570 1347.5 662.5 Less: Non-refundable tax offset Less: Refundable tax offset 900 0 0 Net tax expenses 41766 10701 38966 900 13085 Less: PAYG Credit 31000 0 31000 0 Net tax payable (Refund) 10766 10701 7966 13085 After Tax Income 133234 46299 126784 53165 Wealth Management Working Tax liability Husband Philip Wife Brittney Husband Philip Wife Brittney Taxable income 144000 57000 134750 66250 (18201-45000)@19% 5092 5092 5092 5092 (45001-120000) @32.5% 24375 3900 24375 6906 (120001-180000) @37% 8880 5457 Total gross tax payable 38346 8991 34924 11998 To find out the minimum tax liability, it is required to transfer some of Philip's income to Brittney without pushing her into a higher tax bracket. By splitting the income, both Philip and Brittney can minimize their tax liability. Here, Philip transferred 50% of his term deposit interest income, which is $2250, 100% ANZ Bond Find distribution income, which is $4000 and 100% dividend income, which is $3000, along with franking credit, to Brittney. After that, Philip's tax liability would fall to $7966 from $10766. On the other hand, Brittaney falls under the same tax bracket, which is 32.5%, after receiving a total of $9250 in income from Philip. Their net tax liability is reduced. The total tax liability for Philip after income splitting is $7966, which is lower than before splitting. However, the tax liability of Brittney has increased to $13085 from $10701. Brittney's total after-tax income increased from $46299 to $53165.

Expert Answer:

Related Book For

Financial Accounting The Impact On Decision Makers

ISBN: 9781305793194

10th Edition

Authors: Gary A. Porter, Curtis L. Norton

Posted Date:

Students also viewed these finance questions

-

The following information is available for HTM Corporation's defined benefit pension plan: On January 1, 2017, HTM Corp. amended its pension plan, resulting in past service costs with a present value...

-

The Cottage Bakery sells a variety of gourmet breads, cakes, pies, and pastries. Although its wares are considerably more expensive than those available at supermarkets and other bakeries, the...

-

Posting a $800 purchase of supplies on account appears as which of the following? a. Supplies 800 Accounts Receivable 800 C. Supplies 800 Accounts Payable 800 b. Supplies Accounts Payable d. Cash...

-

At December 31, 2010, certain accounts included in the Noncurrent Operating Assets section of Salvino Companys balance sheet had the following balances: Land . . . . . . . . . . . . . . . . . . . . ....

-

Write SQL queries (do not use QBE) for the following questions and execute the queries using 'TAL_Distributors" database on MS Access. a. How many customers have a credit limit of $15000. b. How many...

-

1. As Stage Gate systems have evolved, (1) should all types of product development activity within a company follow the same Stage Gate process or should the process and stages used depend upon the...

-

Is increasing the temperature of the surroundings the only effect of this "lost" kinetic energy? If the ground is soft, a hard steel ball like this might cause the ground to deform. It does work on...

-

a) (20 p) A boy is seated on the top of a hemispherical mound of ice, of radius R. shown in the figure below. He is given a very small push and starts sliding down the ice. Show that he leaves the...

-

Bridgeport Windows Inc is in the process of setting a target price on its newly designed tinted window. Cost data relating to the window at a budgeted volume of 3,440 units are as follows. Per Unit...

-

Prepare Balance Sheet The following information is available for 2021. a. Equipment was sold for $10,000 (which originally cost $20,000 and had an accumulated depreciation balance of $8,000 at the...

-

The Applebee's buyer heard through others that Rubio Enterprises, a maker of restaurant supplies, recently invested $1.2 million in plant, property, and equipment. The investors for Rubio want an 18%...

Study smarter with the SolutionInn App