While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

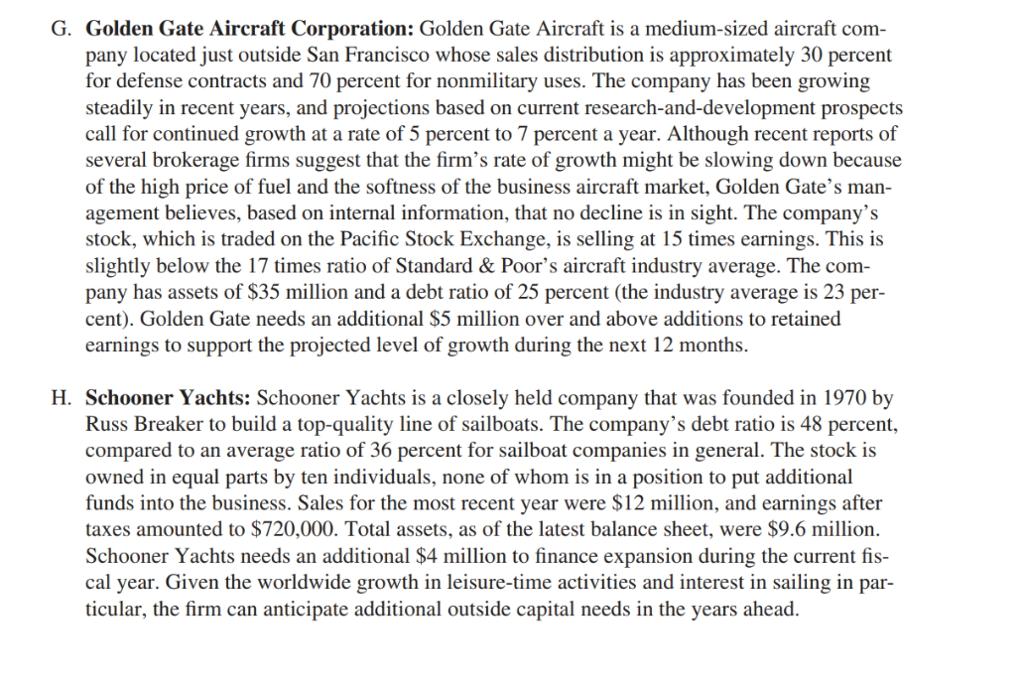

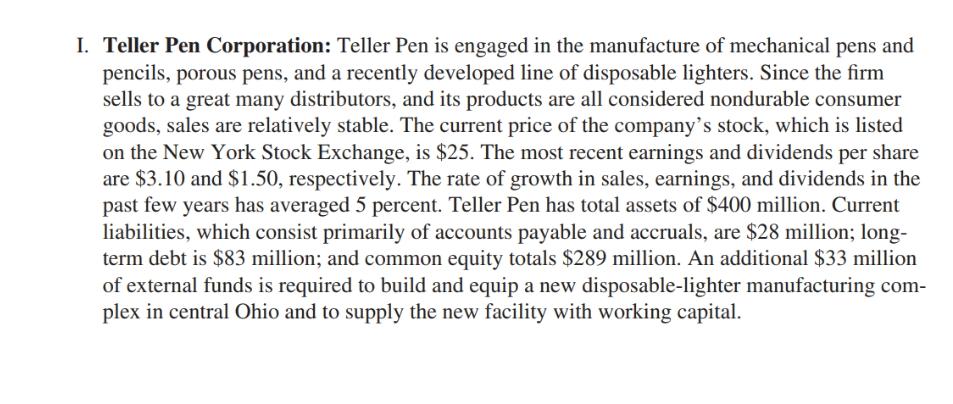

While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar” in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital. While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar" in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital. While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar" in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital. While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar” in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital. While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar" in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital. While investment banking firms traditionally hire relatively few new graduates (especially those without advanced degrees), the positions they do fill are highly sought after and are extremely lucra- tive. Prime candidates not only need to have knowledge of the financial markets, but also must have the ability to sell their firm's services to some of the most successful members of the financial community. Quite often, knowledge of oenology, a person's ancestry, and a scratch golf game have just as much persuasive power in obtaining a client's business as do the actual services pro- vided by a firm such as Julian Eastheimer and Company. Through an old family contact pulling the right strings, Parker Z. Bentley III was fortunate enough to obtain the job of assistant to Maria Talbot, a senior partner and managing director at Julian Eastheimer. Bentley received his bachelor's degree in physical education from a very expen- sive and prestigious Ivy League school only two weeks ago, and this is his first day on the job. After a rather pleasant morning spent meeting various people around the office, Bentley was given his first task-he was asked to review the financing recommendations that Talbot had recently made for nine client firms. The first thing Bentley did was to pull out the financial analyses and recommendations from the clients' folders and give them to one of the secretaries to type. When the secretary returned the typed reports, Bentley discovered that he did not know which recommendation belonged to which company! He had folders for nine different companies and financing recommendations for nine com- panies, but he could not match them up. Bentley's major was physical education, so he could not be expected to match the financing recommendations with the appropriate companies. As a finance student, you should be able to help Bentley by telling him which companies in Sec- tion B should use the financing methods listed in Section A. Section A QUESTIONS 1. Leasing arrangement 2. Long-term bonds 3. Debt with warrants 4. Friends or relatives 5. Common stock: nonrights 6. Preferred stock (nonconvertible) 7. Common stock: rights offering 8. Convertible debentures 9. Factoring (Hint: Factoring is the selling of a firm's accounts receivable.) Section B A. Boudoir's, Inc.: This company, a retail clothing store with three suburban locations in Atlanta, Georgia, is incorporated, with each of the three Boudoir sisters owning one-third of the outstanding stock. The company is profitable, but rapid growth has put it under severe financial strain. The real estate is all under mortgage to an insurance company, the inventory is being used under a blanket chattel mortgage to secure a bank line of credit, and the accounts receivable are all being factored. With total assets of $7 million, the company now needs an additional $450,000 to finance a building and fixtures for a new outlet. B. Timberland Power & Light: Since Timberland Power & Light, a major electric utility, is organized as a holding company, the Securities and Exchange Commission must approve all of its securities issues. Such approval is automatic if the company stays within conventional norms for the public utility industry. Reasonable norms call for long-term debt in the range of 45 percent to 65 percent, preferred stock in the range of 0 to 15 percent, and common equity in the range of 25 percent to 45 percent. Timberland currently has total assets of $1.5 billion financed as follows: $900 million debt, $75 million preferred stock, and $525 million common equity. The company plans to raise an additional $37 million at this time. C. Ripe and Fresh Canning Company: Ripe and Fresh Canning Company is a large operation located in Valdosta, Georgia, that purchases peaches and other fruits from farmers in Geor- gia, Florida, South Carolina, Alabama, and Kentucky. These fruits are then canned and sold on 60-day credit terms, largely to food brokers and small retail grocers in the same five-state area. The company's plant and equipment have been financed in part by a mortgage loan, and this is the only long-term debt. Raw materials (fruits) are purchased on terms calling for payment within 30 days of receipt of goods, but no discounts are offered. Because of an increase in the popularity of vegetables and fruits, canned fruit sales have increased dramati- cally. To finance a higher level of output to take advantage of this increased demand, Ripe and Fresh will need approximately $550,000. D. Piper Pickle Company: Piper Pickle Company is a major packer of pickles and pickled products (horseradish, pickled watermelon rinds, relishes, and peppers). The company's stock is widely held, actively traded, and listed on the New York Stock Exchange. Recently, it has been trading in the range of $18 to $22 a share. The latest 12 months' earn- ings were $1.70 per share. The current dividend rate is 64 cents a share, and earnings, divi- dends, and the price of the company's stock have been growing at a rate of about 7 percent over the last few years. Piper Pickle's debt ratio is currently 42 percent versus 25 percent for other large pickle packers. Other firms in the industry, on the average, have been grow- ing at a rate of about 5 percent a year, and their stocks have been selling at a price/earnings ratio of about 10. Piper Pickle has an opportunity to begin growing its own cucumbers, which would result in a substantial cost savings and reduce the risk involved in having to compete for cucumbers in the open market. This vertical integration would require $20 mil- lion in cash for the necessary farms and equipment. E. Copper Mountain Mining Company: Copper Mountain Mining needs $12 million to finance the acquisition of mineral rights to some land in south central New Mexico and to pay for some extensive surveys, core-borings, magnetic aerial surveys, and other types of analyses designed to determine whether the mineral deposits on this land warrant develop- ment. If the tests are favorable, the company will need an additional $12 million. Copper Mountain Mining's common stock is currently selling at $11, while the company is earning approximately $1 per share. Other firms in the industry sell at from 8 to 13 times earnings. Copper Mountain's debt ratio is 30 percent, compared to an industry average of 35 percent. Total assets at the last balance sheet date were $120 million. F. Bull Gator Saloon and Dance Hall: Robert Radcliffe, a professor at the University of Florida, is an avid country-and-western music fan and a square dancer. He has just learned that a recently developed downtown shopping and entertainment center still has a lease available for the original, renovated building of the First National Bank of Gainesville. The bank outgrew the building in the late 1950s, and the large open spaces and high ceilings would be ideal for a country-and-western nightclub. Radcliffe knows the market well and has often noted the lack of a real "kicker bar" in Gainesville; the closest being in Starke, about 25 miles from Gainesville. Radcliffe believes that if he can obtain approximately $50,000 for a sound system and interior decorations, he can open a small but successful operation in the old bank building. His liquid savings total $15,000, so Radcliffe needs an additional $35,000 to open the proposed nightclub. G. Golden Gate Aircraft Corporation: Golden Gate Aircraft is a medium-sized aircraft com- pany located just outside San Francisco whose sales distribution is approximately 30 percent for defense contracts and 70 percent for nonmilitary uses. The company has been growing steadily in recent years, and projections based on current research-and-development prospects call for continued growth at a rate of 5 percent to 7 percent a year. Although recent reports of several brokerage firms suggest that the firm's rate of growth might be slowing down because of the high price of fuel and the softness of the business aircraft market, Golden Gate's man- agement believes, based on internal information, that no decline is in sight. The company's stock, which is traded on the Pacific Stock Exchange, is selling at 15 times earnings. This is slightly below the 17 times ratio of Standard & Poor's aircraft industry average. The com- pany has assets of $35 million and a debt ratio of 25 percent (the industry average is 23 per- cent). Golden Gate needs an additional $5 million over and above additions to retained earnings to support the projected level of growth during the next 12 months. H. Schooner Yachts: Schooner Yachts is a closely held company that was founded in 1970 by Russ Breaker to build a top-quality line of sailboats. The company's debt ratio is 48 percent, compared to an average ratio of 36 percent for sailboat companies in general. The stock is owned in equal parts by ten individuals, none of whom is in a position to put additional funds into the business. Sales for the most recent year were $12 million, and earnings after taxes amounted to $720,000. Total assets, as of the latest balance sheet, were $9.6 million. Schooner Yachts needs an additional $4 million to finance expansion during the current fis- cal year. Given the worldwide growth in leisure-time activities and interest in sailing in par- ticular, the firm can anticipate additional outside capital needs in the years ahead. I. Teller Pen Corporation: Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its products are all considered nondurable consumer goods, sales are relatively stable. The current price of the company's stock, which is listed on the New York Stock Exchange, is $25. The most recent earnings and dividends per share are $3.10 and $1.50, respectively. The rate of growth in sales, earnings, and dividends in the past few years has averaged 5 percent. Teller Pen has total assets of $400 million. Current liabilities, which consist primarily of accounts payable and accruals, are $28 million; long- term debt is $83 million; and common equity totals $289 million. An additional $33 million of external funds is required to build and equip a new disposable-lighter manufacturing com- plex in central Ohio and to supply the new facility with working capital.

Expert Answer:

Answer rating: 100% (QA)

Matching the financing methods to the appropriate companies in Sec... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Problem C: Use the quick (approximate) travelling salesperson construction to find a tour for the cost matrix below. You may use either of the methods described. If using the textbook method, start...

-

(a) Consider the sequence {F} defined by F = 1, F2 = 1 and Fn+2 Show that = Fn (b) Find the limit of the ratio Fn+1 Fn n (1 + 5) (1 5) 2n5 = Fn+1 + Fn.

-

10. Consider the figure below depicting the Rothschild-Stiglitz model as seen in class. Sick ZPL L ZPL H B A H E Healthy a) Is (A, B) a pooling or separating equilibrium? b) Suppose the economy has...

-

What is the advantage of using computing to simulate an automobile crash test as opposed to actually staging a crash?

-

Wilens and colleagues (2008) studied the association between bipolar disorder and substance abuse. In their study, they reported at a 95% CI that "bipolar disorder was associated with an age-adjusted...

-

In a completely randomized design, describe the process of partitioning the total variation.

-

Using Google, determine the number of hits for these terms: a. Forensic accounting. b. Fraud auditing. c. Forensic auditing. d. Fraud examination.

-

Job costing, accounting for manufacturing overhead, budgeted rates. The Fasano Company uses a job-costing system at its Dover, Delaware, plant. The plant has a machining department and a finishing...

-

I need to provide answers for these questions within 35 mins. Please help me Question 1. What Do You Mean By Business Administration? Question 2. What Are The Roles Played By A Business...

-

Hot & Cold and CaldoFreddo are two European manufacturers of home appliances that have merged. Hot & Cold has plants in France, Germany, and Finland, whereas CaldoFreddo has plants in the...

-

Which of the following is an advantage of direct investing? There is no risk of devalued or restricted currency. The company maintains full control over the investment. Direct investment involves...

-

Use NPV to analyze the decision to purchase the new machine. A) Identify and label each inflows/outflow, don't just present a single inflow/outflow number for each year. B) Assuming a discount rate...

-

A company does $100 million in sales. It has some degree of pricing power in that it sells its output for $10 where it costs it $8 to make. Its advertising is highly effective. For every one percent...

-

what is the general journal entry if Unwanted goods of R 8 0 0 purchased by Mrs . Strong on account, was returned. The cost of the goods is R 5 0 0 .

-

What is the error in the given code? public class progArray { public static void main(String[] args) { double] m1 = new double[4.5]; double pgno = new int[]{2,3,4,5); m1= new double...

-

Storey Co. adds material at the start of production. February information for the company follows (SEE PICTURE BELOW): 28. What are the equivalent units for material using the weighted average...

-

2 J: 216 #. 1/1 QUESTION 1-COMPULSORY QUESTION, Must Be Answered (30 Marks) A) Your client is interested in buying a property in rural Victoria. What is the present value of an offer of $14,000 one...

-

What are bounds and what do companies do with them?

-

You have recently accepted the position of director for a full-service retirement home that has three components. The first component is for retired individuals and married couples who can still...

-

What are some of the key regulations that guide the compliance work of human resource management?

-

You have just been assigned to work with a strategy team in an organization to predict issues and opportunities that might be expected for the next 2 years. Using this chapter, explain what...

-

For the following, determine if the given point is a removable singularity, an essential singularity, or a pole (indicate its order). a. \(\frac{1-\cos z}{z^{2}}, \quad z=0\). b. \(\frac{\sin...

-

Find the Laurent series expansion for \(f(z)=\frac{\sinh z}{z^{3}}\) about \(z=0\). [You need to first do a MacLaurin series expansion for the hyperbolic sine.]

-

Find the residues at the given points: a. \(\frac{2 z^{2}+3 z}{z-1}\) at \(z=1\). b. \(\frac{\ln (1+2 z)}{z}\) at \(z=0\). c. \(\frac{\cos z}{(2 z-\pi)^{3}}\) at \(z=\frac{\pi}{2}\).

Study smarter with the SolutionInn App