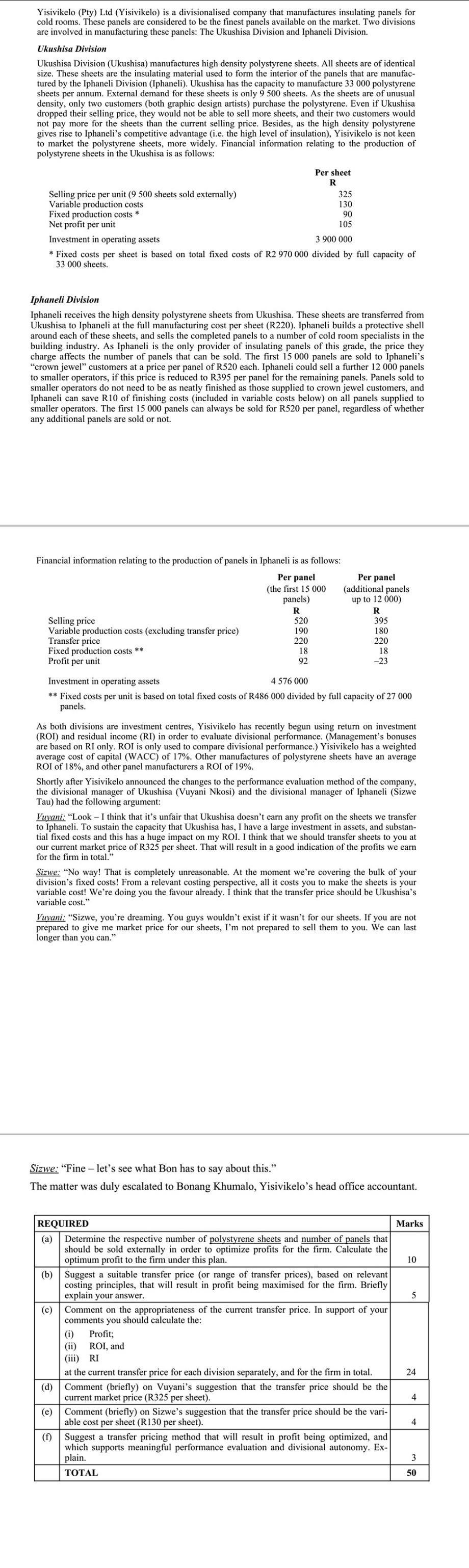

Yisivikelo (Pty) Ltd (Yisivikelo) is a divisionalised company that manufactures insulating panels for cold rooms. These...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Yisivikelo (Pty) Ltd (Yisivikelo) is a divisionalised company that manufactures insulating panels for cold rooms. These panels are considered to be the finest panels available on the market. Two divisions are involved in manufacturing these panels: The Ukushisa Division and Iphaneli Division. Ukushisa Division Ukushisa Division (Ukushisa) manufactures high density polystyrene sheets. All sheets are of identical size. These sheets are the insulating material used to form the interior of the panels that are manufac- tured by the Iphaneli Division (Iphaneli). Ukushisa has the capacity to manufacture 33 000 polystyrene sheets per annum. External demand for these sheets is only 9 500 sheets. As the sheets are of unusual density, only two customers (both graphic design artists) purchase the polystyrene. Even if Ukushisa dropped their selling price, they would not be able to sell more sheets, and their two customers would not pay more for the sheets than the current selling price. Besides, as the high density polystyrene gives rise to Iphaneli's competitive advantage (i.e. the high level of insulation), Yisivikelo is not keen to market the polystyrene sheets, more widely. Financial information relating to the production of polystyrene sheets in the Ukushisa is as follows: Selling price per unit (9 500 sheets sold externally) Variable production costs Fixed production costs * Net profit per unit Investment in operating assets 325 130 90 105 3 900 000 * Fixed costs per sheet is based on total fixed costs of R2 970 000 divided by full capacity of 33 000 sheets. Iphaneli Division Iphaneli receives the high density polystyrene sheets from Ukushisa. These sheets are transferred from Ukushisa to Iphaneli at the full manufacturing cost per sheet (R220). Iphaneli builds a protective shell around each of these sheets, and sells the completed panels to a number of cold room specialists in the building industry. As Iphaneli is the only provider of insulating panels of this grade, the price they charge affects the number of panels that can be sold. The first 15 000 panels are sold to Iphaneli's "crown jewel" customers at a price per panel of R520 each. Iphaneli could sell a further 12 000 panels to smaller operators, if this price is reduced to R395 per panel for the remaining panels. Panels sold to smaller operators do not need to be as neatly finished as those supplied to crown jewel customers, and Iphaneli can save R10 of finishing costs (included in variable costs below) on all panels supplied to smaller operators. The first 15 000 panels can always be sold for R520 per panel, regardless of whether any additional panels are sold or not. Financial information relating to the production of panels in Iphaneli is as follows: Per panel (the first 15 000 panels) R Selling price Variable production costs (excluding transfer price) Transfer price Fixed production costs ** Profit per unit Per sheet R 520 190 220 18 92 Per panel (additional panels up to 12 000) R Investment in operating assets 4 576 000 ** Fixed costs per unit is based on total fixed costs of R486 000 divided by full capacity of 27 000 panels. 395 180 220 18 -23 As both divisions are investment centres, Yisivikelo has recently begun using return on investment (ROI) and residual income (RI) in order to evaluate divisional performance. (Management's bonuses are based on RI only. ROI is only used to compare divisional performance.) Yisivikelo has a weighted average cost of capital (WACC) of 17%. Other manufactures of polystyrene sheets have an average ROI of 18%, and other panel manufacturers a ROI of 19%. Shortly after Yisivikelo announced the changes to the performance evaluation method of the company, the divisional manager of Ukushisa (Vuyani Nkosi) and the divisional manager of Iphaneli (Sizwe Tau) had the following argument: Vuyani: "Look - I think that it's unfair that Ukushisa doesn't earn any profit on the sheets we transfer to Iphaneli. To sustain the capacity that Ukushisa has, I have a large investment in assets, and substan- tial fixed costs and this has a huge impact on my ROI. I think that we should transfer sheets to you at our current market price of R325 per sheet. That will result in a good indication of the profits we earn for the firm in total." Sizwe: "No way! That is completely unreasonable. At the moment we're covering the bulk of your division's fixed costs! From a relevant costing perspective, all it costs you to make the sheets is your variable cost! We're doing you the favour already. I think that the transfer price should be Ukushisa's variable cost." Vuyani: "Sizwe, you're dreaming. You guys wouldn't exist if it wasn't for our sheets. If you are not prepared to give me market price for our sheets, I'm not prepared to sell them to you. We can last longer than you can." Sizwe: "Fine - let's see what Bon has to say about this." The matter was duly escalated to Bonang Khumalo, Yisivikelo's head office accountant. REQUIRED (a) Determine the respective number of polystyrene sheets and number of panels that should be sold externally in order to optimize profits for the firm. Calculate the optimum profit to the firm under this plan. (i) Profit; ROI, and (iii) RI (f) (b) Suggest a suitable transfer price (or range of transfer prices), based on relevant costing principles, that will result in profit being maximised for the firm. Briefly explain your answer. (c) Comment on the appropriateness of the current transfer price. In support of your comments you should calculate the: at the current transfer price for each division separately, and for the firm in total. (d) Comment (briefly) on Vuyani's suggestion that the transfer price should be the current market price (R325 per sheet). (e) Comment (briefly) on Sizwe's suggestion that the transfer price should be the vari- able cost per sheet (R130 per sheet). Suggest a transfer pricing method that will result in profit being optimized, and which supports meaningful performance evaluation and divisional autonomy. Ex- plain. TOTAL Marks 10 5 24 4 4 3 50 Yisivikelo (Pty) Ltd (Yisivikelo) is a divisionalised company that manufactures insulating panels for cold rooms. These panels are considered to be the finest panels available on the market. Two divisions are involved in manufacturing these panels: The Ukushisa Division and Iphaneli Division. Ukushisa Division Ukushisa Division (Ukushisa) manufactures high density polystyrene sheets. All sheets are of identical size. These sheets are the insulating material used to form the interior of the panels that are manufac- tured by the Iphaneli Division (Iphaneli). Ukushisa has the capacity to manufacture 33 000 polystyrene sheets per annum. External demand for these sheets is only 9 500 sheets. As the sheets are of unusual density, only two customers (both graphic design artists) purchase the polystyrene. Even if Ukushisa dropped their selling price, they would not be able to sell more sheets, and their two customers would not pay more for the sheets than the current selling price. Besides, as the high density polystyrene gives rise to Iphaneli's competitive advantage (i.e. the high level of insulation), Yisivikelo is not keen to market the polystyrene sheets, more widely. Financial information relating to the production of polystyrene sheets in the Ukushisa is as follows: Selling price per unit (9 500 sheets sold externally) Variable production costs Fixed production costs * Net profit per unit Investment in operating assets 325 130 90 105 3 900 000 * Fixed costs per sheet is based on total fixed costs of R2 970 000 divided by full capacity of 33 000 sheets. Iphaneli Division Iphaneli receives the high density polystyrene sheets from Ukushisa. These sheets are transferred from Ukushisa to Iphaneli at the full manufacturing cost per sheet (R220). Iphaneli builds a protective shell around each of these sheets, and sells the completed panels to a number of cold room specialists in the building industry. As Iphaneli is the only provider of insulating panels of this grade, the price they charge affects the number of panels that can be sold. The first 15 000 panels are sold to Iphaneli's "crown jewel" customers at a price per panel of R520 each. Iphaneli could sell a further 12 000 panels to smaller operators, if this price is reduced to R395 per panel for the remaining panels. Panels sold to smaller operators do not need to be as neatly finished as those supplied to crown jewel customers, and Iphaneli can save R10 of finishing costs (included in variable costs below) on all panels supplied to smaller operators. The first 15 000 panels can always be sold for R520 per panel, regardless of whether any additional panels are sold or not. Financial information relating to the production of panels in Iphaneli is as follows: Per panel (the first 15 000 panels) R Selling price Variable production costs (excluding transfer price) Transfer price Fixed production costs ** Profit per unit Per sheet R 520 190 220 18 92 Per panel (additional panels up to 12 000) R Investment in operating assets 4 576 000 ** Fixed costs per unit is based on total fixed costs of R486 000 divided by full capacity of 27 000 panels. 395 180 220 18 -23 As both divisions are investment centres, Yisivikelo has recently begun using return on investment (ROI) and residual income (RI) in order to evaluate divisional performance. (Management's bonuses are based on RI only. ROI is only used to compare divisional performance.) Yisivikelo has a weighted average cost of capital (WACC) of 17%. Other manufactures of polystyrene sheets have an average ROI of 18%, and other panel manufacturers a ROI of 19%. Shortly after Yisivikelo announced the changes to the performance evaluation method of the company, the divisional manager of Ukushisa (Vuyani Nkosi) and the divisional manager of Iphaneli (Sizwe Tau) had the following argument: Vuyani: "Look - I think that it's unfair that Ukushisa doesn't earn any profit on the sheets we transfer to Iphaneli. To sustain the capacity that Ukushisa has, I have a large investment in assets, and substan- tial fixed costs and this has a huge impact on my ROI. I think that we should transfer sheets to you at our current market price of R325 per sheet. That will result in a good indication of the profits we earn for the firm in total." Sizwe: "No way! That is completely unreasonable. At the moment we're covering the bulk of your division's fixed costs! From a relevant costing perspective, all it costs you to make the sheets is your variable cost! We're doing you the favour already. I think that the transfer price should be Ukushisa's variable cost." Vuyani: "Sizwe, you're dreaming. You guys wouldn't exist if it wasn't for our sheets. If you are not prepared to give me market price for our sheets, I'm not prepared to sell them to you. We can last longer than you can." Sizwe: "Fine - let's see what Bon has to say about this." The matter was duly escalated to Bonang Khumalo, Yisivikelo's head office accountant. REQUIRED (a) Determine the respective number of polystyrene sheets and number of panels that should be sold externally in order to optimize profits for the firm. Calculate the optimum profit to the firm under this plan. (i) Profit; ROI, and (iii) RI (f) (b) Suggest a suitable transfer price (or range of transfer prices), based on relevant costing principles, that will result in profit being maximised for the firm. Briefly explain your answer. (c) Comment on the appropriateness of the current transfer price. In support of your comments you should calculate the: at the current transfer price for each division separately, and for the firm in total. (d) Comment (briefly) on Vuyani's suggestion that the transfer price should be the current market price (R325 per sheet). (e) Comment (briefly) on Sizwe's suggestion that the transfer price should be the vari- able cost per sheet (R130 per sheet). Suggest a transfer pricing method that will result in profit being optimized, and which supports meaningful performance evaluation and divisional autonomy. Ex- plain. TOTAL Marks 10 5 24 4 4 3 50

Expert Answer:

Answer rating: 100% (QA)

a To optimize profits for the firm we need to determine the respective number of polystyrene sheets and panels that should be sold externally Lets calculate the optimum profit to the firm under this p... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

The Duke Corporation bottles and sells various vegetable oils and preparations. It recently acquired a bottling plant and has been operating it as a separate division within Duke. So far, the Bottle...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Erin McQueen purchased 50 shares of BMW, a German stock traded on the Frankfurt Exchange, for 64.5 euros () per share exactly 1 year ago when the exchange rate was 0.67 /US$. Today the stock is...

-

A firm reports $3,721 million of net operating assets and $560 million of net financial obligations at the end of 2008. Its 105 million shares outstanding trade at $53 each. You expect its current...

-

The file lists the calorics and sugar, in grams, in one serving of seven breakfast cereals: a. Compute the covariance. b. Compute the coefficient of correlation. c. Which do you think is more...

-

The template for this exercise gives price information and market cap for 10 companies. Compute the stock returns and the individual regressions of returns on the S&P 500. Use this data to construct...

-

Your pharmaceutical firm is seeking to open up new international markets by partnering with various local distributors. The different distributors within a country are stronger with different market...

-

[6 Let f(x) = 3x2 - 2 and let g(x) = 5x + 1. Find the given value. 9( - 1)] * c:> g( 1)] = E (Type an integer or a decimai.)

-

One technique for limiting fault current is to place reactance in series with the generators. Such reactance can be modeled in PowerWorld Simulator by increasing the value of the generator's positive...

-

Given that simple interest on a certain sum of money is Rs. 4016.25 at 9% per annum in 5 years. Find the sum of money.

-

Describe four of the five general forms of analytical procedures. For each form describe a typical source of the information for the form. For each source, include any questions or concerns an...

-

A given polyhedron is the Feasible Region of a linear programming problem inside, and the indicating variable on each side is as follows. a) Reveal both basic and non-basic variables at point A b)...

-

Why have PepsiCo and The Coca-Cola companies spent so much money on product differentiation? Give at least three (3) reasons.

-

Aslan Inc. is a new company and it is experiencing rapid growth. Dividends are expected to grow at 32% per year during the next three years, 20% over the following year, and then 8% per year...

-

Workout and explain intertemporal optimization and portfolio optimization conditions for a two period consumption model in which an individual has fixed endowment in the first period. After meeting...

-

what is Mysticism based on lectures and chapters 16 & 17. The Varieties of Religious Experience by William James

-

An Atomic Energy Commission nuclear facility was established in Hanford, Washington, in 1943. Over the years, a significant amount of strontium 90 and cesium 137 leaked into the Columbia River. In a...

-

Suntrek in Problem 28 supplies its finished denim jeans to its customers' distribution centers in the United States in New York and New Orleans, and in Europe in Bristol and Marseilles. Denim jeans...

-

Solve the linear programming model for WeeMow Lawn Service in Problem 63 using the computer. a. Which resources constrain how many jobs the service can contract for? b. If WeeMow could increase its...

-

In the "Forecasting Airport Passenger Arrivals" case problem in Chapter 15, the objective is to develop a forecasting model to predict daily airline passenger arrivals for 2-hour time segments from...

-

Bank Reconciliation} Shortly after July 31, Towanda Corporation received a bank statement containing the following information: July cash transactions and balances on Towanda's records are shown in...

-

Quality Review. Charalambos Viachoutsicos is assigned the responsibility of setting up a quality review programme at his St Petersburg, Russia, audit firm, Levenchuk. Required A. What should the...

-

Bank Reconciliation} Darjeeling Corporation received the bank statement shown below for the month of October: The cash records of Darjeeling Corporation provide the following information: The items...

Study smarter with the SolutionInn App