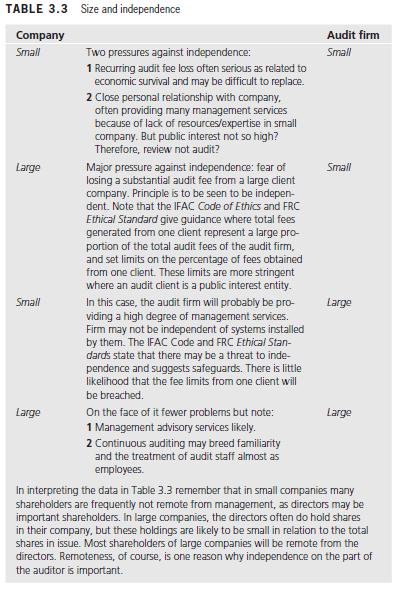

In Table 3.3 we suggested pressures against independence in respect of small audit firms and small auditees.

Question:

In Table 3.3 we suggested pressures against independence in respect of small audit firms and small auditees. To what extent do you believe that the IFAC Code and FRC Ethical Standard have been successful in dealing with the special circumstances of small audit firms and small entities?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Robert Mwendwa Nzinga

I am a professional accountant with diverse skills in different fields. I am a great academic writer and article writer. I also possess skills in website development and app development. I have over the years amassed skills in project writing, business planning, human resource administration and tutoring in all business related courses.

187+ Reviews

378+ Question Solved

Related Book For

The Audit Process Principles Practice And Cases

ISBN: 9781473760189

7th Edition

Authors: Iain Gray, Louise Crawford, Stuart Manson

Question Posted: