Answer the following questions. a. What is the purpose of the second and third general attestation standards

Question:

Answer the following questions.

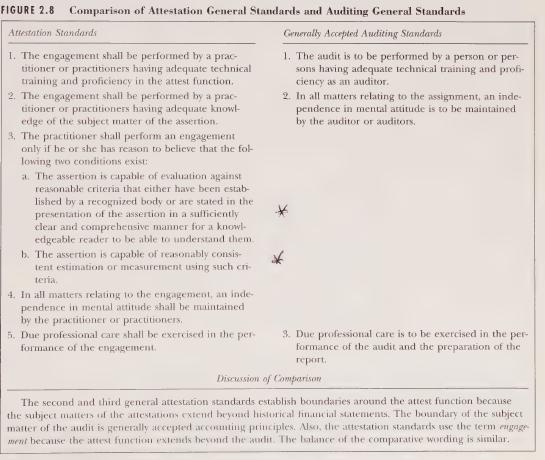

a. What is the purpose of the second and third general attestation standards shown in Figure 2.8?

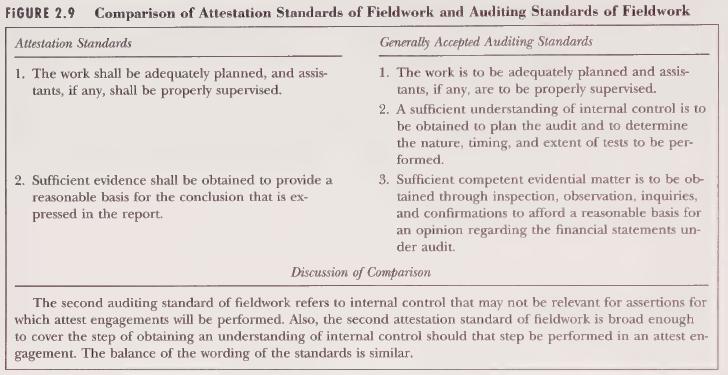

b. In Figure 2.9, why is there no attestation standard of fieldwork referring to internal control?

c. In Figure 2.10, why are there no attestation standards of reporting that refer to consistency and informative disclosures?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Amos Kiprotich

I am a wild researcher and I guarantee you a well written paper that is plagiarism free. I am a good time manager and hence you are assured that your paper will always be delivered a head of time. My services are cheap and the prices include a series of revisions, free referencing and formatting.

15+ Reviews

21+ Question Solved

Related Book For

Auditing An Assertions Approach

ISBN: 9780471134213

7th Edition

Authors: G. William Glezen, Donald H. Taylor

Question Posted: