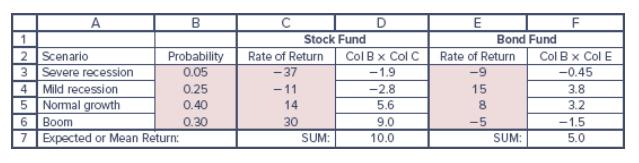

Suppose the rates of return of the bond portfolio in the four scenarios of Spreadsheet 6.1 are

Question:

Suppose the rates of return of the bond portfolio in the four scenarios of Spreadsheet 6.1 are −10% in a severe recession, 10% in a mild recession, 7% in a normal period, and 2% in a boom. The stock returns in the four scenarios are −37%, −11%, 14%, and 30%. What are the covariance and correlation coefficient between the rates of return on the two portfolios?

Spreadsheet 6.1

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Recalculation of Spreadsheets 61 and 64 shows that the covariance is now 5...View the full answer

Answered By

Surojit Das

I have vast knowledge in the field of Mathematics, Business Management and Marketing. Besides, I have been teaching on the topics Management leadership, Business Administration, Human Resource Management, Business Communication, Accounting, Auditing, Organizer Behaviours, Business Writing, Essay Writing, Copy Writing, Blog Writing since 2020. It is my personality to act quickly in any emergency situations when students need my services. I am very professional and serious in every questions students asked me at the time of dealing any projects. I have been serving detailed, quality, properly analysed research paper through the years.

91+ Reviews

278+ Question Solved

Related Book For

ISE Essentials Of Investments

ISBN: 9781265450090

12th International Edition

Authors: Zvi Bodie, Alex Kane, Alan Marcus

Question Posted: