As VP Finance (Europe) at GE Capital, you manage GEs European exposures to currency risk. GEs light

Question:

As VP Finance (Europe) at GE Capital, you manage GE’s European exposures to currency risk. GE’s light bulb plant in Poland generates Polish zloty (Z) after-tax operating cash inflows of Z10 million per year. Your treasury management team decides to hedge one-half of the expected future cash flow from operations (i.e., 5 million zlotys per year) for each of the next five years. Goldman Sachs quotes the following pricing schedule for currency coupon swaps of zlotys and dollars.

Deduct 20 bps if the bank is paying a fixed rate. Add 20 bps if the bank is receiving a fixed rate. All quotes are against 1-year LIBOR Eurodollar flat. The spot rate of exchange is Z2.80∕$. The dollar and zloty yield curves are flat, with the dollar selling at a forward premium of 3.8 percent per year. Assume bonds in Poland are quoted as a 365-day bond equivalent yield with annual compounding.

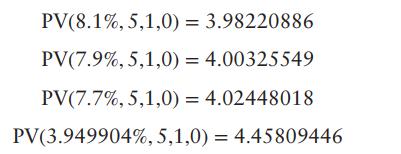

To assist in your calculations, here are present value factors for 5-year annuities at various interest rates from Excel’s PV(RATE,NPER,PMT,FV) function.

a. GE has 5-year floating rate dollar debt at 1-year LIBOR + 32 bps. Describe a fully covered dollar-for-zloty swap using the swap pricing schedule. Calculate the all-in cost of GE’s floating rate zloty debt.

b. Solidarity Partners (SP) has Z 19,811,044 of 5-year zloty debt at 10.24 percent compounded annually. SP wants floating rate dollar debt—with interest payments reset annually— to fund its U.S. operations. Calculate the all-in cost of SP’s fully covered zloty-for-dollar swap.

c. What does the swap bank gain from these transactions?

Step by Step Answer: