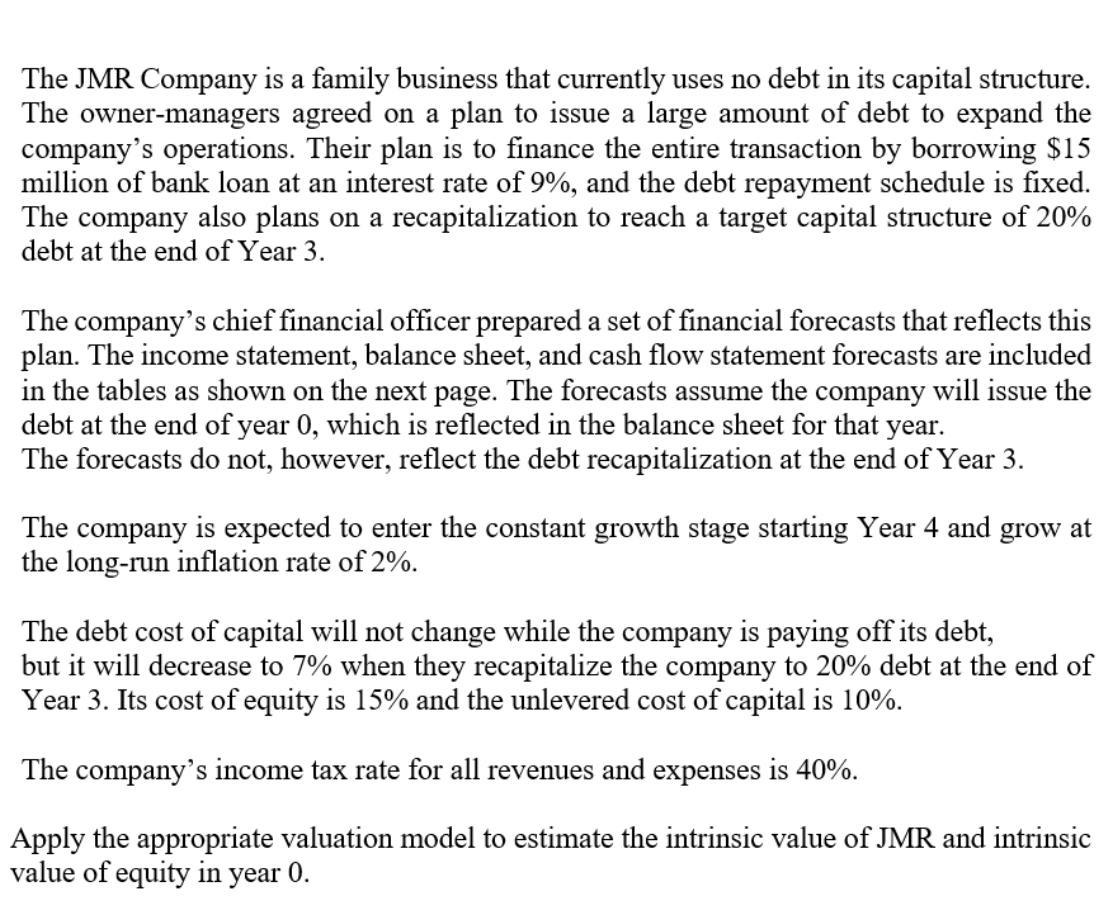

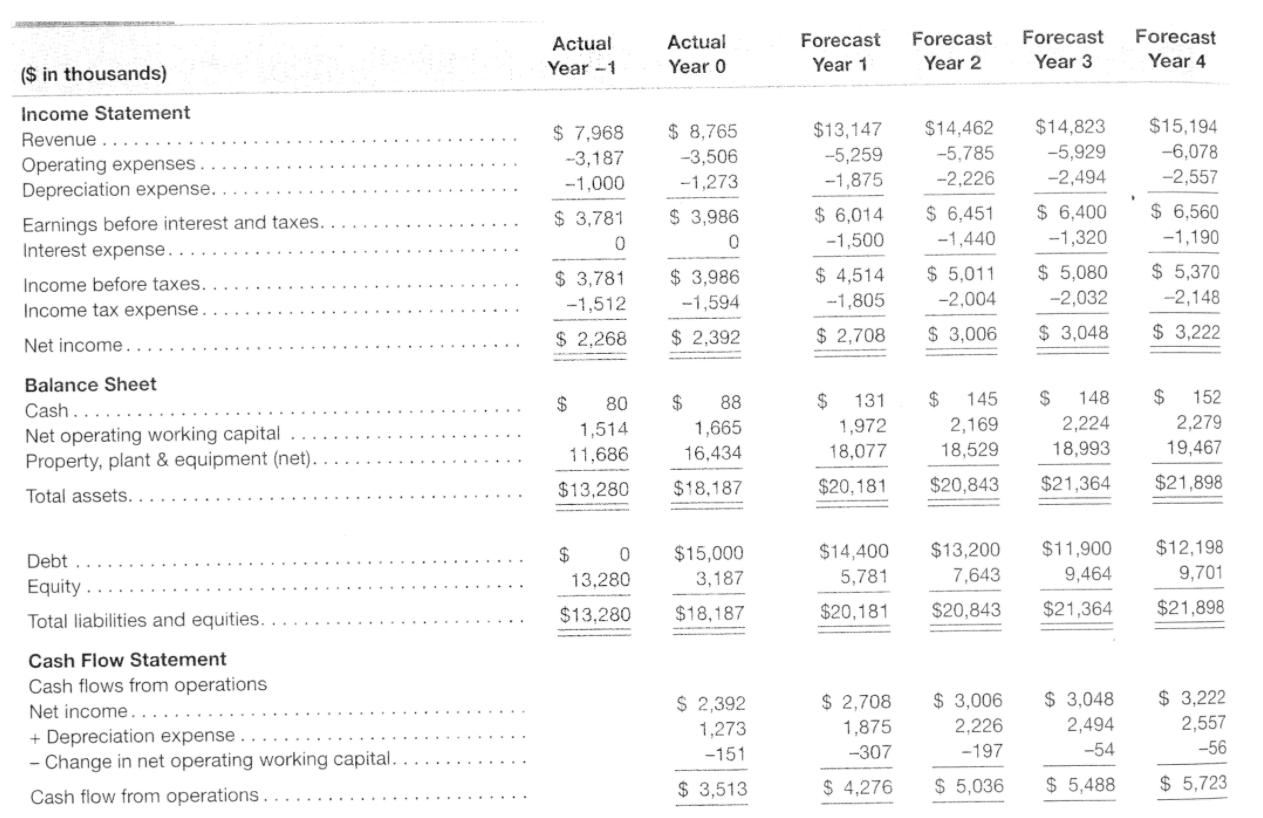

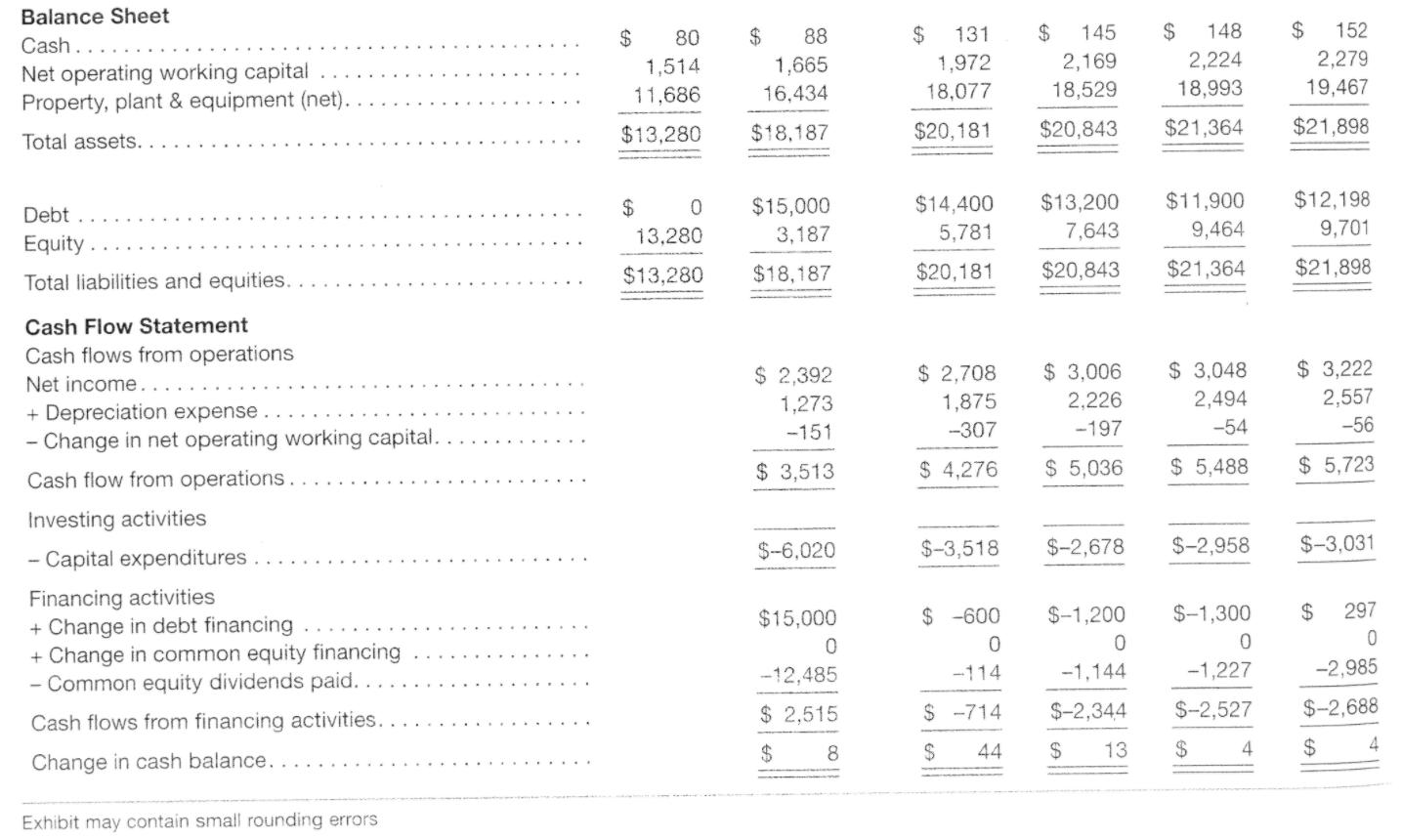

The JMR Company is a family business that currently uses no debt in its capital structure....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The JMR Company is a family business that currently uses no debt in its capital structure. The owner-managers agreed on a plan to issue a large amount of debt to expand the company's operations. Their plan is to finance the entire transaction by borrowing $15 million of bank loan at an interest rate of 9%, and the debt repayment schedule is fixed. The company also plans on a recapitalization to reach a target capital structure of 20% debt at the end of Year 3. The company's chief financial officer prepared a set of financial forecasts that reflects this plan. The income statement, balance sheet, and cash flow statement forecasts are included in the tables as shown on the next page. The forecasts assume the company will issue the debt at the end of year 0, which is reflected in the balance sheet for that year. The forecasts do not, however, reflect the debt recapitalization at the end of Year 3. The company is expected to enter the constant growth stage starting Year 4 and grow at the long-run inflation rate of 2%. The debt cost of capital will not change while the company is paying off its debt, but it will decrease to 7% when they recapitalize the company to 20% debt at the end of Year 3. Its cost of equity is 15% and the unlevered cost of capital is 10%. The company's income tax rate for all revenues and expenses is 40%. Apply the appropriate valuation model to estimate the intrinsic value of JMR and intrinsic value of equity in year 0. Actual Actual Forecast Forecast Forecast Forecast Year -1 Year 0 Year 1 Year 2 Year 3 Year 4 ($ in thousands) Income Statement $14,823 -5,929 $ 8,765 $15,194 $14,462 -5,785 $13,147 $ 7,968 -3,187 -1,000 Revenue. -6,078 -5,259 -1,875 -3,506 Operating expenses. Depreciation expense. -1,273 -2,226 -2,494 -2,557 $ 6,451 $ 6,560 $ 6,014 -1,500 $ 6,400 -1,320 $ 3,781 $ 3,986 Earnings before interest and taxes. Interest expense.... -1,440 -1,190 $ 3,781 $ 3,986 $ 4,514 $ 5,011 $ 5,080 $ 5,370 Income before taxes. -1,512 -1,594 -1,805 -2,004 -2,032 -2,148 Income tax expense. $ 2,268 $ 2,392 $ 2,708 $ 3,006 $ 3,048 $ 3,222 Net income... Balance Sheet 24 145 2$ 148 2$ 152 $ 1,972 Cash.. 24 80 2$ 88 131 1,514 1,665 2,169 2,224 2,279 Net operating working capital Property, plant & equipment (net). 11,686 16,434 18,077 18,529 18,993 19,467 $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total assets.. $ $15,000 $14,400 $13,200 $11,900 $12,198 Debt 13,280 3,187 5,781 7,643 9,464 9,701 Equity. $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total liabilities and equities. Cash Flow Statement Cash flows from operations $ 2,708 $ 3,006 $ 3,048 $ 3,222 $ 2,392 1,273 Net income. 1,875 2,226 2,494 2,557 + Depreciation expense - Change in net operating working capital. Cash flow from operations. -151 -307 -197 -54 -56 $ 3,513 $ 4,276 $ 5,036 $ 5,488 $ 5,723 Balance Sheet 2$ 80 24 88 24 131 2$ 145 2$ 148 2$ 152 Cash... 2,279 19,467 1,972 2,169 2,224 1,665 16,434 1,514 Net operating working capital Property, plant & equipment (net). 11,686 18,077 18,529 18,993 $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total assets. $14,400 $13,200 $11,900 $12,198 $15,000 3,187 Debt 24 13,280 5,781 7,643 9,464 9,701 Equity $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total liabilities and equities. Cash Flow Statement Cash flows from operations Net income.. $ 3,222 2,557 $ 3,006 $ 3,048 2,494 $ 2,708 $ 2,392 1,273 1,875 2,226 + Depreciation expense - Change in net operating working capital. -151 -307 -197 -54 -56 $ 3,513 $ 4,276 $ 5,036 $ 5,488 $ 5,723 Cash flow from operations.. Investing activities $-6,020 $-3,518 $-2,678 $-2,958 $-3,031 Capital expenditures Financing activities + Change in debt financing + Change in common equity financing - Common equity dividends paid. $15,000 $ -600 $-1,200 $-1,300 24 297 -12,485 -114 -1,144 -1,227 -2,985 $ 2,515 $ -714 $-2,344 $-2,527 $-2,688 Cash flows from financing activities. 2$ 8 2$ 44 2$ 13 2$ 24 4 Change in cash balance. Exhibit may contain small rounding errors The JMR Company is a family business that currently uses no debt in its capital structure. The owner-managers agreed on a plan to issue a large amount of debt to expand the company's operations. Their plan is to finance the entire transaction by borrowing $15 million of bank loan at an interest rate of 9%, and the debt repayment schedule is fixed. The company also plans on a recapitalization to reach a target capital structure of 20% debt at the end of Year 3. The company's chief financial officer prepared a set of financial forecasts that reflects this plan. The income statement, balance sheet, and cash flow statement forecasts are included in the tables as shown on the next page. The forecasts assume the company will issue the debt at the end of year 0, which is reflected in the balance sheet for that year. The forecasts do not, however, reflect the debt recapitalization at the end of Year 3. The company is expected to enter the constant growth stage starting Year 4 and grow at the long-run inflation rate of 2%. The debt cost of capital will not change while the company is paying off its debt, but it will decrease to 7% when they recapitalize the company to 20% debt at the end of Year 3. Its cost of equity is 15% and the unlevered cost of capital is 10%. The company's income tax rate for all revenues and expenses is 40%. Apply the appropriate valuation model to estimate the intrinsic value of JMR and intrinsic value of equity in year 0. Actual Actual Forecast Forecast Forecast Forecast Year -1 Year 0 Year 1 Year 2 Year 3 Year 4 ($ in thousands) Income Statement $14,823 -5,929 $ 8,765 $15,194 $14,462 -5,785 $13,147 $ 7,968 -3,187 -1,000 Revenue. -6,078 -5,259 -1,875 -3,506 Operating expenses. Depreciation expense. -1,273 -2,226 -2,494 -2,557 $ 6,451 $ 6,560 $ 6,014 -1,500 $ 6,400 -1,320 $ 3,781 $ 3,986 Earnings before interest and taxes. Interest expense.... -1,440 -1,190 $ 3,781 $ 3,986 $ 4,514 $ 5,011 $ 5,080 $ 5,370 Income before taxes. -1,512 -1,594 -1,805 -2,004 -2,032 -2,148 Income tax expense. $ 2,268 $ 2,392 $ 2,708 $ 3,006 $ 3,048 $ 3,222 Net income... Balance Sheet 24 145 2$ 148 2$ 152 $ 1,972 Cash.. 24 80 2$ 88 131 1,514 1,665 2,169 2,224 2,279 Net operating working capital Property, plant & equipment (net). 11,686 16,434 18,077 18,529 18,993 19,467 $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total assets.. $ $15,000 $14,400 $13,200 $11,900 $12,198 Debt 13,280 3,187 5,781 7,643 9,464 9,701 Equity. $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total liabilities and equities. Cash Flow Statement Cash flows from operations $ 2,708 $ 3,006 $ 3,048 $ 3,222 $ 2,392 1,273 Net income. 1,875 2,226 2,494 2,557 + Depreciation expense - Change in net operating working capital. Cash flow from operations. -151 -307 -197 -54 -56 $ 3,513 $ 4,276 $ 5,036 $ 5,488 $ 5,723 Balance Sheet 2$ 80 24 88 24 131 2$ 145 2$ 148 2$ 152 Cash... 2,279 19,467 1,972 2,169 2,224 1,665 16,434 1,514 Net operating working capital Property, plant & equipment (net). 11,686 18,077 18,529 18,993 $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total assets. $14,400 $13,200 $11,900 $12,198 $15,000 3,187 Debt 24 13,280 5,781 7,643 9,464 9,701 Equity $13,280 $18,187 $20,181 $20,843 $21,364 $21,898 Total liabilities and equities. Cash Flow Statement Cash flows from operations Net income.. $ 3,222 2,557 $ 3,006 $ 3,048 2,494 $ 2,708 $ 2,392 1,273 1,875 2,226 + Depreciation expense - Change in net operating working capital. -151 -307 -197 -54 -56 $ 3,513 $ 4,276 $ 5,036 $ 5,488 $ 5,723 Cash flow from operations.. Investing activities $-6,020 $-3,518 $-2,678 $-2,958 $-3,031 Capital expenditures Financing activities + Change in debt financing + Change in common equity financing - Common equity dividends paid. $15,000 $ -600 $-1,200 $-1,300 24 297 -12,485 -114 -1,144 -1,227 -2,985 $ 2,515 $ -714 $-2,344 $-2,527 $-2,688 Cash flows from financing activities. 2$ 8 2$ 44 2$ 13 2$ 24 4 Change in cash balance. Exhibit may contain small rounding errors

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The norm of a linear transformation TA: Rn Rn can be defined by where the maximum is taken over all nonzero x in Rn. (The subscript indicates that the norm of the linear transformation on the left is...

-

Suppose that f: Rn R and g: Rn Rn are differentiable on Rn and that there exist r > 0 and a Rn such that Dg(x) is the identity matrix, I, for all x Br(a). Prove that there is a function h: Br(a) {a}...

-

Let 5: Rn Rn and T: Rn Rn be linear transformations with matrices A and B respectively. [Theorem 3.] (a) Show that B2 = B if and only if T2 = 7 (where T2 means T o T). (b) Show that B2 = 1 if and...

-

Builder Products, Incorporated, uses the weighted-average method in its process costing system. It manufactures a caulking compound that goes through three processing stages prior to completion....

-

Consider Figure 1-14. Explain the meaning of the line that connects CUSTOMER to ORDER and the line that connects ORDER to INVOICE. What does this say about how Pine Valley Furniture Company does...

-

Prepare in journal form the entries necessary to record the following stock transactions of the Seoul Company during 2010: Oct. 1 Purchased 2,000 shares of its own $2 par value common stock for $20...

-

7. Which of these might be valid consideration? a. A promise to do something. b. A promise to refrain from doing something. c. An action. d. All of the above.

-

On January 1, 2019, Sharon Matthews established Tri-City Realty, which completed the following transactions during the month: a. Sharon Matthews transferred cash from a personal bank account to an...

-

please answer quickly. 5. a. The following transactions were completed during June in Ocean Bookstore. June 01 Purchased books on account for $1,500 from Bluemart Publishers, FOB destination, terms...

-

4. (Chapter 3) Skycell, a major European cell phone manufacturer, is making production plans for the coming year. Skycell has worked with its customers (the service providers) to come up with...

-

Explain the concept of capacity planning and how businesses can effectively align their production capabilities with market demands.

-

Price = $25 Variable Cost= $15 Fixed Cost= $130 000 Tax Rate= 30% Compute cm Compute cm ratio Compute be in units assume that the company was able to reduce the VC per unit by $3. What selling price...

-

In contrast, futures contracts, with their liquidity and transparent pricing, provide an efficient means for traders and investors to hedge against market fluctuations. The requirement for margin...

-

A 4.33 kilogram object is 286.75 meters above the ground. What is the object potential energy in joules at this height? Round up to two decimal places

-

If a group of angel investors invests $7,750,000 now, they will receive 27% of the exit value given the expected rate of return is 33% on their investment. What is the firm's exit value at the end of...

-

Bandar Industries manufactures sporting equipment. One of the company's products is a football helmet that requires special plastic. During the quarter ending June 30, the company manufactured 3,100...

-

2. Could Canada Revenue Agency make an argument to deny ASCI's small business deduction ? Briefly explain why there is a risk and what steps can be taken to reduce the exposure 3. Jacob would like...

-

Write the expression in radical notation. Then evaluate the expression when the result is an integer. 23 -1/2

-

What if the last two decades had been normal? Download the spreadsheet from MyFinanceLab containing the data for Figure 10.1. a. Calculate the arithmetic average return on the S&P 500 from 1926 to...

-

Suppose the option in Example 21.1 actually sold in the market for $8. Describe a trading strategy that yields arbitrage profits.

-

How can proxy contests be used to overcome a captured board?

-

Explain why the amount of cash salaries paid to employees does not equal salaries expense for the employer.

-

Why are most current liabilities recognized at maturity value at the beginning of their term?

-

Differentiate between secured and unsecured liabilities. Explain the reporting procedures for each.

Study smarter with the SolutionInn App