Lois Griffon, 36 years old, is a senior IT programmer with the Calgary Board of Education...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

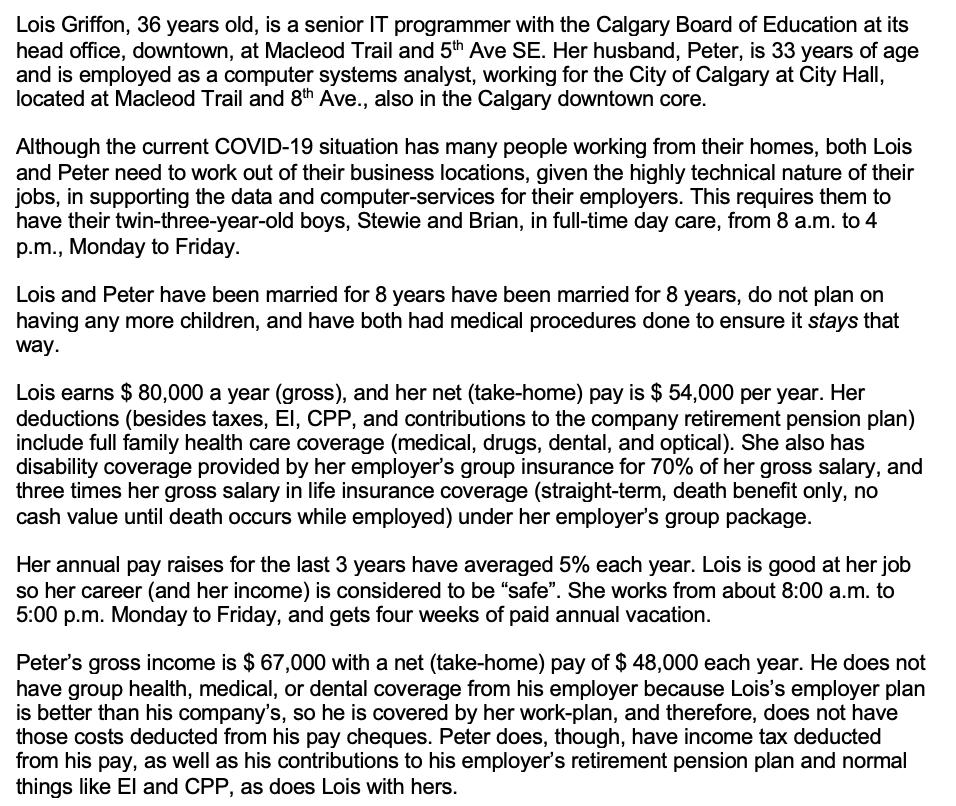

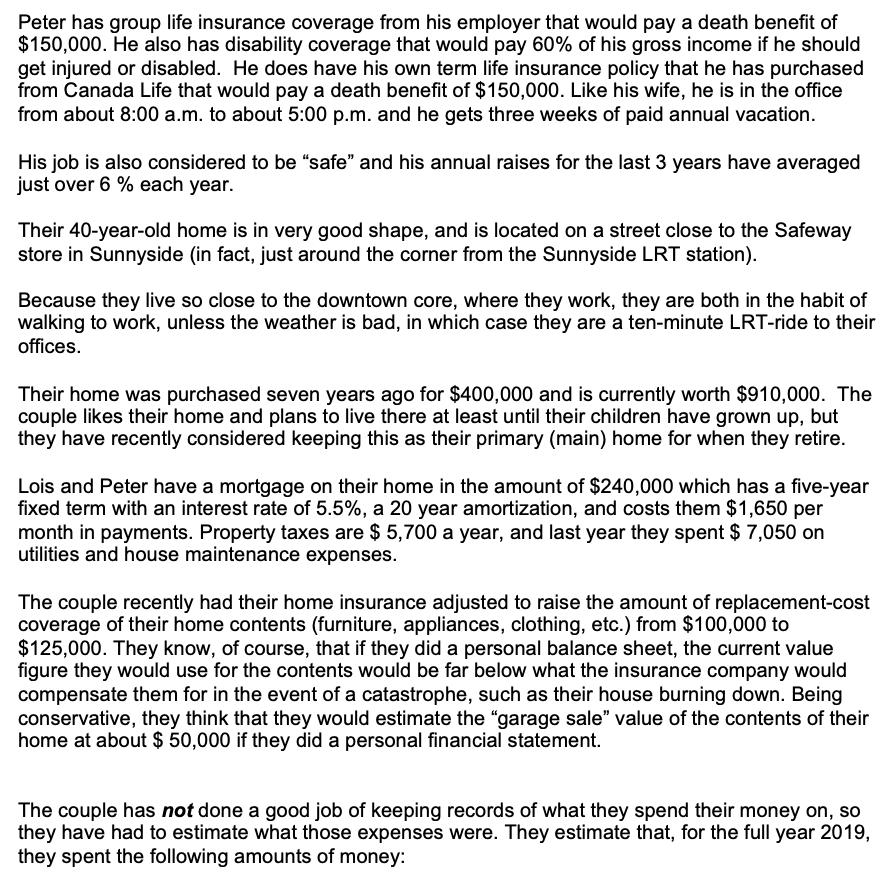

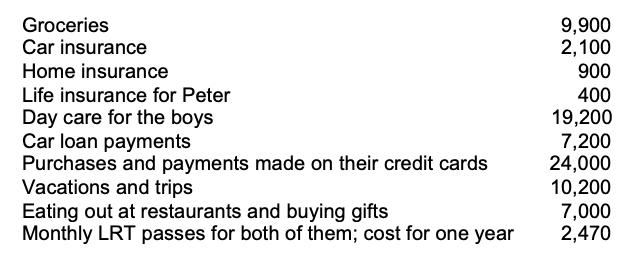

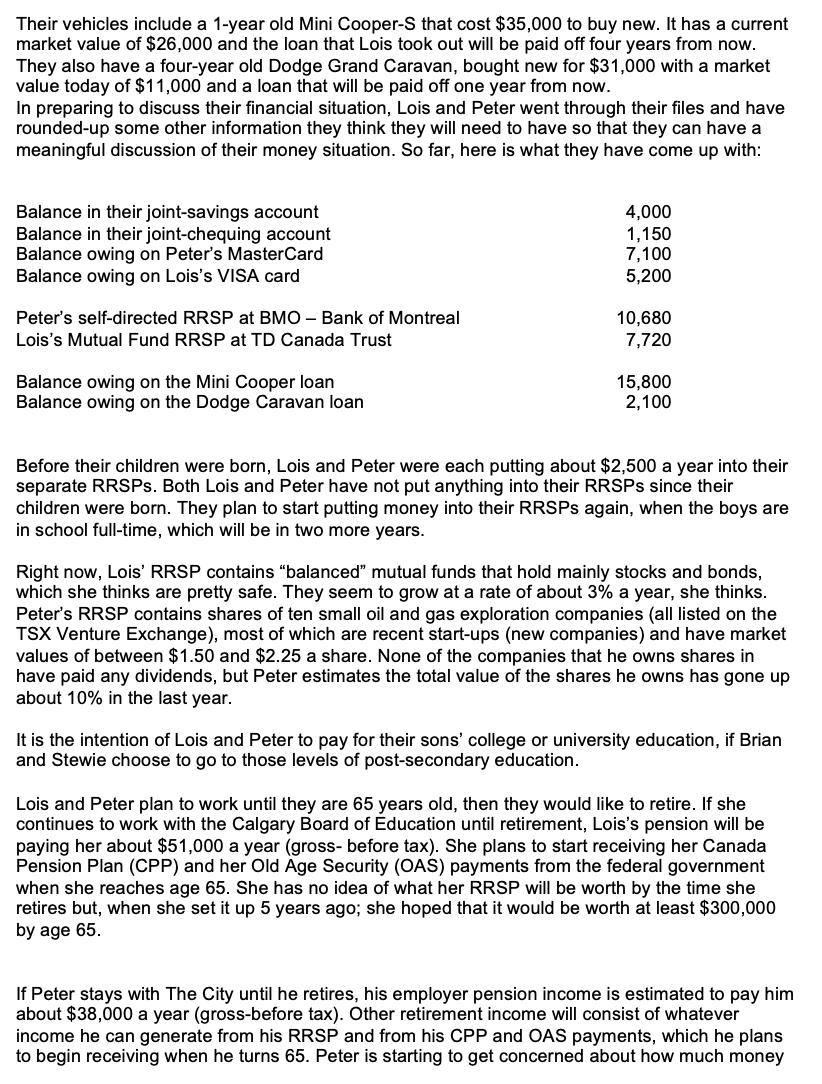

Lois Griffon, 36 years old, is a senior IT programmer with the Calgary Board of Education at its head office, downtown, at Macleod Trail and 5th Ave SE. Her husband, Peter, is 33 years of age and is employed as a computer systems analyst, working for the City of Calgary at City Hall, located at Macleod Trail and 8th Ave., also in the Calgary downtown core. Although the current COVID-19 situation has many people working from their homes, both Lois and Peter need to work out of their business locations, given the highly technical nature of their jobs, in supporting the data and computer-services for their employers. This requires them to have their twin-three-year-old boys, Stewie and Brian, in full-time day care, from 8 a.m. to 4 p.m., Monday to Friday. Lois and Peter have been married for 8 years have been married for 8 years, do not plan on having any more children, and have both had medical procedures done to ensure it stays that way. Lois earns $ 80,000 a year (gross), and her net (take-home) pay is $ 54,000 per year. Her deductions (besides taxes, El, CPP, and contributions to the company retirement pension plan) include full family health care coverage (medical, drugs, dental, and optical). She also has disability coverage provided by her employer's group insurance for 70% of her gross salary, and three times her gross salary in life insurance coverage (straight-term, death benefit only, no cash value until death occurs while employed) under her employer's group package. Her annual pay raises for the last 3 years have averaged 5% each year. Lois is good at her job so her career (and her income) is considered to be "safe". She works from about 8:00 a.m. to 5:00 p.m. Monday to Friday, and gets four weeks of paid annual vacation. Peter's gross income is $ 67,000 with a net (take-home) pay of $ 48,000 each year. He does not have group health, medical, or dental coverage from his employer because Lois's employer plan is better than his company's, so he is covered by her work-plan, and therefore, does not have those costs deducted from his pay cheques. Peter does, though, have income tax deducted from his pay, as well as his contributions to his employer's retirement pension plan and normal things like El and CPP, as does Lois with hers. Peter has group life insurance coverage from his employer that would pay a death benefit of $150,000. He also has disability coverage that would pay 60% of his gross income if he should get injured or disabled. He does have his own term life insurance policy that he has purchased from Canada Life that would pay a death benefit of $150,000. Like his wife, he is in the office from about 8:00 a.m. to about 5:00 p.m. and he gets three weeks of paid annual vacation. His job is also considered to be "safe" and his annual raises for the last 3 years have averaged just over 6 % each year. Their 40-year-old home is in very good shape, and is located on a street close to the Safeway store in Sunnyside (in fact, just around the corner from the Sunnyside LRT station). Because they live so close to the downtown core, where they work, they are both in the habit of walking to work, unless the weather is bad, in which case they are a ten-minute LRT-ride to their offices. Their home was purchased seven years ago for $400,000 and is currently worth $910,000. The couple likes their home and plans to live there at least until their children have grown up, but they have recently considered keeping this as their primary (main) home for when they retire. Lois and Peter have a mortgage on their home in the amount of $240,000 which has a five-year fixed term with an interest rate of 5.5%, a 20 year amortization, and costs them $1,650 per month in payments. Property taxes are $ 5,700 a year, and last year they spent $ 7,050 on utilities and house maintenance expenses. The couple recently had their home insurance adjusted to raise the amount of replacement-cost coverage of their home contents (furniture, appliances, clothing, etc.) from $100,000 to $125,000. They know, of course, that if they did a personal balance sheet, the current value figure they would use for the contents would be far below what the insurance company would compensate them for in the event of a catastrophe, such as their house burning down. Being conservative, they think that they would estimate the "garage sale" value of the contents of their home at about $ 50,000 if they did a personal financial statement. The couple has not done a good job of keeping records of what they spend their money on, so they have had to estimate what those expenses were. They estimate that, for the full year 2019, they spent the following amounts of money: Groceries 9,900 2,100 900 Car insurance Home insurance Life insurance for Peter Day care for the boys Car loan payments Purchases and payments made on their credit cards Vacations and trips Eating out at restaurants and buying gifts Monthly LRT passes for both of them; cost for one year 400 19,200 7,200 24,000 10,200 7,000 2,470 Their vehicles include a 1-year old Mini Cooper-S that cost $35,000 to buy new. It has a current market value of $26,000 and the loan that Lois took out will be paid off four years from now. They also have a four-year old Dodge Grand Caravan, bought new for $31,000 with a market value today of $11,000 and a loan that will be paid off one year from now. In preparing to discuss their financial situation, Lois and Peter went through their files and have rounded-up some other information they think they will need to have so that they can have a meaningful discussion of their money situation. So far, here is what they have come up with: Balance in their joint-savings account Balance in their joint-chequing account Balance owing on Peter's MasterCard Balance owing on Lois's VISA card 4,000 1,150 7,100 5,200 10,680 7,720 Peter's self-directed RRSP at BMO - Bank of Montreal Lois's Mutual Fund RRSP at TD Canada Trust Balance owing on the Mini Cooper loan Balance owing on the Dodge Caravan loan 15,800 2,100 Before their children were born, Lois and Peter were each putting about $2,500 a year into their separate RRSPS. Both Lois and Peter have not put anything into their RRSPS since their children were born. They plan to start putting money into their RRSPS again, when the boys are in school full-time, which will be in two more years. Right now, Lois' RRSP contains "balanced" mutual funds that hold mainly stocks and bonds, which she thinks are pretty safe. They seem to grow at a rate of about 3% a year, she thinks. Peter's RRSP contains shares of ten small oil and gas exploration companies (all listed on the TSX Venture Exchange), most of which are recent start-ups (new companies) and have market values of between $1.50 and $2.25 a share. None of the companies that he owns shares in have paid any dividends, but Peter estimates the total value of the shares he owns has gone up about 10% in the last year. It is the intention of Lois and Peter to pay for their sons' college or university education, if Brian and Stewie choose to go to those levels of post-secondary education. Lois and Peter plan to work until they are 65 years old, then they would like to retire. If she continues to work with the Calgary Board of Education until retirement, Lois's pension will be paying her about $51,000 a year (gross- before tax). She plans to start receiving her Canada Pension Plan (CPP) and her Old Age Security (OAS) payments from the federal government when she reaches age 65. She has no idea of what her RRSP will be worth by the time she retires but, when she set it up 5 years ago; she hoped that it would be worth at least $300,000 by age 65. If Peter stays with The City until he retires, his employer pension income is estimated to pay him about $38,000 a year (gross-before tax). Other retirement income will consist of whatever income he can generate from his RRSP and from his CPP and OAS payments, which he plans to begin receiving when he turns 65. Peter is starting to get concerned about how much money he will actually be able to build into his RRSP by the time he reaches age 65 but, like his wife, originally thought he could have about $300,000 in his RRSP by the time he hits age 65. When they do retire, Lois and Peter would like to spend at least 3 months each winter in either Arizona or Mexico. With this being part of their plan, they believe they will need to have a joint (combined) gross-annual income, at retirement, of at least $125,000 per year. Lois and Peter are not good at saving money, and even worse at knowing where the money goes. They use their credit cards to buy almost everything so they can build-up the Air Miles and other travel-points to take vacations on. Some months they pay large amounts of money against their credit card balances, other months they make only the minimum payments. 1) Using the concept that is contained in Exhibit 2 – 3 from the course textbook (a copy of which is attached at the back), create a joint personal balance sheet as at Dec. 31, 2019 and provide your conclusions about what you see in their balance sheet. (5 marks for the balance sheet, and 5 marks for your commentary) 2) Using the concept that is contained in Exhibit 2 – 4 from the course textbook (a copy of which is attached at the back) create a joint cash-flow statement as at Dec. 31, 2019 and provide your conclusions about what that cash-flow statement seems to indicate. (5 marks for the cash flow statement and 5 marks for the commentary) Lois Griffon, 36 years old, is a senior IT programmer with the Calgary Board of Education at its head office, downtown, at Macleod Trail and 5th Ave SE. Her husband, Peter, is 33 years of age and is employed as a computer systems analyst, working for the City of Calgary at City Hall, located at Macleod Trail and 8th Ave., also in the Calgary downtown core. Although the current COVID-19 situation has many people working from their homes, both Lois and Peter need to work out of their business locations, given the highly technical nature of their jobs, in supporting the data and computer-services for their employers. This requires them to have their twin-three-year-old boys, Stewie and Brian, in full-time day care, from 8 a.m. to 4 p.m., Monday to Friday. Lois and Peter have been married for 8 years have been married for 8 years, do not plan on having any more children, and have both had medical procedures done to ensure it stays that way. Lois earns $ 80,000 a year (gross), and her net (take-home) pay is $ 54,000 per year. Her deductions (besides taxes, El, CPP, and contributions to the company retirement pension plan) include full family health care coverage (medical, drugs, dental, and optical). She also has disability coverage provided by her employer's group insurance for 70% of her gross salary, and three times her gross salary in life insurance coverage (straight-term, death benefit only, no cash value until death occurs while employed) under her employer's group package. Her annual pay raises for the last 3 years have averaged 5% each year. Lois is good at her job so her career (and her income) is considered to be "safe". She works from about 8:00 a.m. to 5:00 p.m. Monday to Friday, and gets four weeks of paid annual vacation. Peter's gross income is $ 67,000 with a net (take-home) pay of $ 48,000 each year. He does not have group health, medical, or dental coverage from his employer because Lois's employer plan is better than his company's, so he is covered by her work-plan, and therefore, does not have those costs deducted from his pay cheques. Peter does, though, have income tax deducted from his pay, as well as his contributions to his employer's retirement pension plan and normal things like El and CPP, as does Lois with hers. Peter has group life insurance coverage from his employer that would pay a death benefit of $150,000. He also has disability coverage that would pay 60% of his gross income if he should get injured or disabled. He does have his own term life insurance policy that he has purchased from Canada Life that would pay a death benefit of $150,000. Like his wife, he is in the office from about 8:00 a.m. to about 5:00 p.m. and he gets three weeks of paid annual vacation. His job is also considered to be "safe" and his annual raises for the last 3 years have averaged just over 6 % each year. Their 40-year-old home is in very good shape, and is located on a street close to the Safeway store in Sunnyside (in fact, just around the corner from the Sunnyside LRT station). Because they live so close to the downtown core, where they work, they are both in the habit of walking to work, unless the weather is bad, in which case they are a ten-minute LRT-ride to their offices. Their home was purchased seven years ago for $400,000 and is currently worth $910,000. The couple likes their home and plans to live there at least until their children have grown up, but they have recently considered keeping this as their primary (main) home for when they retire. Lois and Peter have a mortgage on their home in the amount of $240,000 which has a five-year fixed term with an interest rate of 5.5%, a 20 year amortization, and costs them $1,650 per month in payments. Property taxes are $ 5,700 a year, and last year they spent $ 7,050 on utilities and house maintenance expenses. The couple recently had their home insurance adjusted to raise the amount of replacement-cost coverage of their home contents (furniture, appliances, clothing, etc.) from $100,000 to $125,000. They know, of course, that if they did a personal balance sheet, the current value figure they would use for the contents would be far below what the insurance company would compensate them for in the event of a catastrophe, such as their house burning down. Being conservative, they think that they would estimate the "garage sale" value of the contents of their home at about $ 50,000 if they did a personal financial statement. The couple has not done a good job of keeping records of what they spend their money on, so they have had to estimate what those expenses were. They estimate that, for the full year 2019, they spent the following amounts of money: Groceries 9,900 2,100 900 Car insurance Home insurance Life insurance for Peter Day care for the boys Car loan payments Purchases and payments made on their credit cards Vacations and trips Eating out at restaurants and buying gifts Monthly LRT passes for both of them; cost for one year 400 19,200 7,200 24,000 10,200 7,000 2,470 Their vehicles include a 1-year old Mini Cooper-S that cost $35,000 to buy new. It has a current market value of $26,000 and the loan that Lois took out will be paid off four years from now. They also have a four-year old Dodge Grand Caravan, bought new for $31,000 with a market value today of $11,000 and a loan that will be paid off one year from now. In preparing to discuss their financial situation, Lois and Peter went through their files and have rounded-up some other information they think they will need to have so that they can have a meaningful discussion of their money situation. So far, here is what they have come up with: Balance in their joint-savings account Balance in their joint-chequing account Balance owing on Peter's MasterCard Balance owing on Lois's VISA card 4,000 1,150 7,100 5,200 10,680 7,720 Peter's self-directed RRSP at BMO - Bank of Montreal Lois's Mutual Fund RRSP at TD Canada Trust Balance owing on the Mini Cooper loan Balance owing on the Dodge Caravan loan 15,800 2,100 Before their children were born, Lois and Peter were each putting about $2,500 a year into their separate RRSPS. Both Lois and Peter have not put anything into their RRSPS since their children were born. They plan to start putting money into their RRSPS again, when the boys are in school full-time, which will be in two more years. Right now, Lois' RRSP contains "balanced" mutual funds that hold mainly stocks and bonds, which she thinks are pretty safe. They seem to grow at a rate of about 3% a year, she thinks. Peter's RRSP contains shares of ten small oil and gas exploration companies (all listed on the TSX Venture Exchange), most of which are recent start-ups (new companies) and have market values of between $1.50 and $2.25 a share. None of the companies that he owns shares in have paid any dividends, but Peter estimates the total value of the shares he owns has gone up about 10% in the last year. It is the intention of Lois and Peter to pay for their sons' college or university education, if Brian and Stewie choose to go to those levels of post-secondary education. Lois and Peter plan to work until they are 65 years old, then they would like to retire. If she continues to work with the Calgary Board of Education until retirement, Lois's pension will be paying her about $51,000 a year (gross- before tax). She plans to start receiving her Canada Pension Plan (CPP) and her Old Age Security (OAS) payments from the federal government when she reaches age 65. She has no idea of what her RRSP will be worth by the time she retires but, when she set it up 5 years ago; she hoped that it would be worth at least $300,000 by age 65. If Peter stays with The City until he retires, his employer pension income is estimated to pay him about $38,000 a year (gross-before tax). Other retirement income will consist of whatever income he can generate from his RRSP and from his CPP and OAS payments, which he plans to begin receiving when he turns 65. Peter is starting to get concerned about how much money he will actually be able to build into his RRSP by the time he reaches age 65 but, like his wife, originally thought he could have about $300,000 in his RRSP by the time he hits age 65. When they do retire, Lois and Peter would like to spend at least 3 months each winter in either Arizona or Mexico. With this being part of their plan, they believe they will need to have a joint (combined) gross-annual income, at retirement, of at least $125,000 per year. Lois and Peter are not good at saving money, and even worse at knowing where the money goes. They use their credit cards to buy almost everything so they can build-up the Air Miles and other travel-points to take vacations on. Some months they pay large amounts of money against their credit card balances, other months they make only the minimum payments. 1) Using the concept that is contained in Exhibit 2 – 3 from the course textbook (a copy of which is attached at the back), create a joint personal balance sheet as at Dec. 31, 2019 and provide your conclusions about what you see in their balance sheet. (5 marks for the balance sheet, and 5 marks for your commentary) 2) Using the concept that is contained in Exhibit 2 – 4 from the course textbook (a copy of which is attached at the back) create a joint cash-flow statement as at Dec. 31, 2019 and provide your conclusions about what that cash-flow statement seems to indicate. (5 marks for the cash flow statement and 5 marks for the commentary)

Expert Answer:

Answer rating: 100% (QA)

answer A disability is any scientific circumstance that makes it greater tough for someone to do sur... View the full answer

Related Book For

Canadian Income Taxation planning and decision making

ISBN: 9781259094330

17th edition 2014-2015 version

Authors: Joan Kitunen, William Buckwold

Posted Date:

Students also viewed these economics questions

-

Anu aged 39 years old is a Singaporean Citizen and is a lecturer in an institution. She is married and has 2 Singapore citizen children aged 10 and 12 years old respectively. Her husband, Rajis a...

-

Calculate cost of giving up discounts, and whether to take/reject the discount for the following data: Cost of financing Terms of credit Cash If paid Suppliers discount within ... net 10 5...

-

Peter and Lois are a married couple with one child, Brian. Peter is a member of a group extended health insurance plan that covers his whole family. For dental claims, the plan has a $100 individual...

-

In a popular carnival ride called The Centrifuge, shown above, riders stand against the inside wall of a large cylinder, which starts spinning. The radius of the circle traveled by the riders is 4 ....

-

The table in Exercise 24 shows the maximum weights (in kilograms) for which one repetition of a half squat can be performed and the jump heights (in centimeters) for 12 international soccer players....

-

EYs analysis of the accounts of 16 European utilities reveals that almost 17.7 billion (US$23.4 billion) was written off balance sheets between 2010 and 2011. A large proportion (58 per cent) of this...

-

Which of the following assertions is inaccurate may challenge the auditors independence in fact or/and the perceived independence? (a) An independent auditor auditing a company in which he was also a...

-

A new accounting intern at Gibson Corporation lost the only copy of this periods master budget. The CFO wants to evaluate performance for this period but needs the master budget to do so. Actual...

-

Great Pyramids.?? Inspired by his recent trip to the Great? Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars? (LYD) and S...

-

MAQ Corporation, a major producer of consumer electronics equipment, is currently faced with a rapidly growing product line and its associated inventory problems. MAQ's president, Mary Semerod, has...

-

In the text a three element model for muscle was presented, consisting of a linear spring (constant ko), a dashpot (constant no), and a contractile element that generates a tension To for a period C...

-

Your company Tesla Energy sells back-up battery power systems for medium- and large size companies. Several of your customers in Mexico and Colombia have asked Tesla Energy to provide financing of up...

-

Tin - Can, Inc. Aircraft ( TCAI ) R&D Project Management Problem Your group is hired to help TCAI Project Manager to solve the following problem. Using the activity time estimates and activity...

-

The Antarctic petrel is an important indicator bird species, and researchers are interested in determining its abundance in the Shetland Islands in Antarctica to measure the effects of global...

-

The following information was available for the year ended December 31, 2022: Cost of goods sold Average inventory for the year Inventory at year-end Required: a. Calculate the inventory turnover for...

-

Put yourself in the role of a CEO of a health care facility and evaluate two proposals recently made to you: The Creation of a Cardiac Catheterization Laboratory and an On-site Daycare free to...

-

Personajes importantesCada medida es una aproximacin. Ninguna medida fsica de masa,longitud, tiempo o cualquier otra propiedad es absolutamenteprecisa (exacta). La precisin de una medicin e 1 answer

-

Discuss the information available from the following techniques in the analysis of inorganic pigments used in antique oil paintings: (i) Powder X-ray diffraction, (ii) Infrared and Raman...

-

Profits of a partnership are included in the income of the partners only when those profits are distributed to them. Is this statement true? Explain.

-

Victoria had income for tax purposes for the current year as follows: Salary $65,000 Taxable benefits 5,000 Registered pension plan deduction (3,000) Employment income for tax purposes 67,000 Loss...

-

Certain indirect forms of compensation are deductible by the employer but not taxable to the employee. Does this special tax treatment provide a benefit to the employee or to the employer? Explain.

-

On January 1, 2020, Sharp Company purchased \(\$ 50,000\) of Sox Company \(5 \%\) bonds, at a time when the market rate was \(6 \%\). The bonds mature on December 31, 2024, and pay interest...

-

Assume the same facts as in Brief Exercise 14-16, except that Sharp Company does not intend to trade the bonds or to hold them until maturity. a. Prepare the entry for the purchase of the debt...

-

Tracking Co. holds an AFS bond investment in Fields Corp. The carrying value of the investment is \(\$ 4,500\) at December 31, 2020. Tracking Co. determines the fair value of the investment at the...

Study smarter with the SolutionInn App