Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

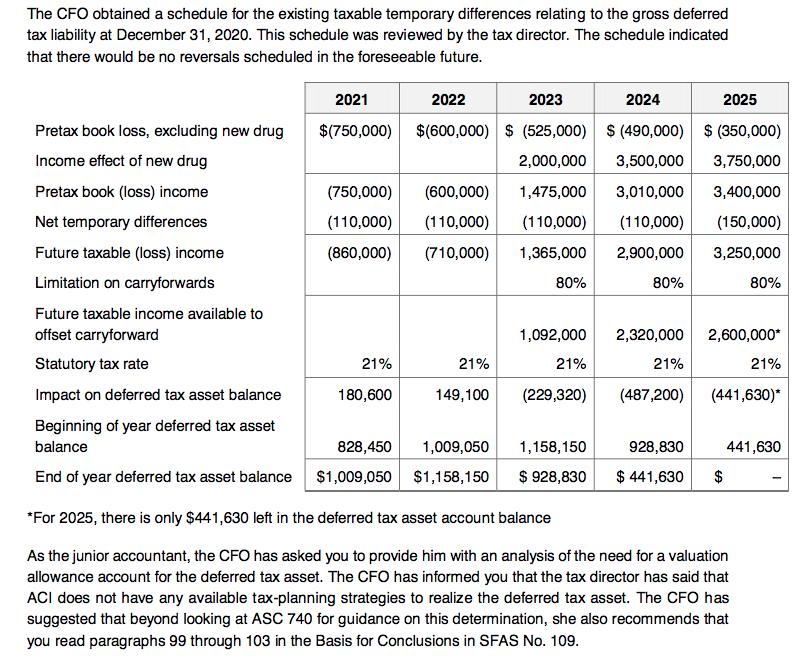

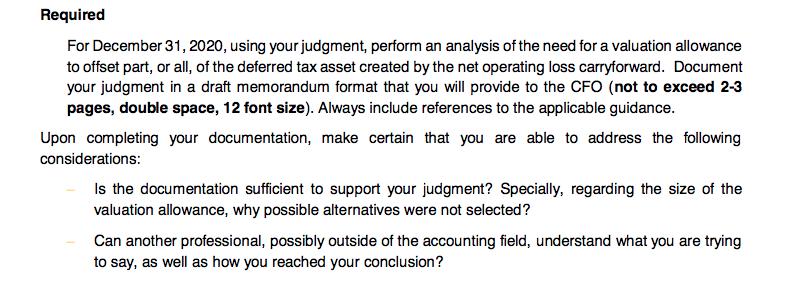

Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion? Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion?

Expert Answer:

Answer rating: 100% (QA)

Based on my analysis I recommend that the CFO should not establish a valuation allowance to offset the deferred tax asset balance because ACI is antic... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

Asbat Pharmaceuticals (Asbat) is a leading pharmaceutical company that has been in existence for 22 years. Asbat has a calendar year-end and is audited annually. Asbat only operates in the United...

-

The Company classifies its investments in both fixed income securities and publicly traded equity securities as available- for- sale investments. Fixed income securities primarily consist of U. S....

-

Lehman Brothers Holdings Inc. was originally founded in Montgomery, Alabama, in 1850 by three brothers. The company began as a small retailer that took cotton as payment for goods. The company...

-

Find the antiderivative for each function when C equals 0. a. f(x) = 1 7 b. g(x)== 11 +/- 150 is a. The antiderivative of 5 c. h(x)=4 -- X Part 1 of 3

-

Multiple Choice Questions 1. United First Bank, the nationwide banking company, owns many types of investments. Assume that United First Bank paid $700,000 for trading securities on December 3. Two...

-

Use the data from Problem 19 to rebalance the line with a cycle time of 90 seconds. How does the number of workstations change? What happens to the output and the lines efficiency?

-

The balance sheets and additional information relating to Pennylane Ltd are given below. Prepare a cash flow statement for Pennylane Ltd for the year ended 31 December 2003 as required under FRS 1...

-

Roebuck Industries produces two electronic decoders, P and Q. Decoder P is more sophisticated and requires more programming and testing than does Decoder Q. Because of these product differences, the...

-

Can someone please help me out with this question? Kingbird Corp. is planning to replace an old asset with new equipment that will operate more efficiently. The following amounts may be relevant to...

-

1. Compare and contrast the various segments of Chinese luxury consumers and customers profiled in the case. 2. How have luxury goods brands responded to President Xi Jinpings crackdown on...

-

Cheyenne Vision Inc. opened for business on Jan 1, and uses a perpetual inventory system. During January, the company had the following purchases and sales for one of its products: Purchases Sales...

-

Cylindrical cookies (radius: 1 cm and height 0.5 cm) are cooled on a conveyer belt after exiting an oven. The cookies enter the conveyer belt at 200 C. The goal is for the cookies to exit the...

-

Identify the current main issues of leadership and employees stress in hospitality and tourism industry. Explain a set of organizational and HR strategies and tactics to address the crisis or issues...

-

1. Consider the market for Colonoscopy at the beginning of 2019(15 points) a. Show the changes using a standard diagram. i. An increase in the number of people turning age 50 this year. ii. A...

-

Premier Corporation has an ROE of 14.1 percent and a payout ratio of 25 percent. What is its sustainable growth rate? (Do not round intermediate calculations and enter your answer as a percent...

-

What are some of the issues you see in current events, especially in criminal justice and security, that relate to organizational behavior?

-

What advice or recommendations would you offer to parents considering adopting preschool-aged children from unstable environments, based on your understanding of the potential challenges and...

-

Find the radius of convergence in two ways: (a) Directly by the CauchyHadamard formula in Sec. 15.2. (b) From a series of simpler terms by using Theorem 3 or Theorem 4.

-

Canadian National Railway Company (CN) spans Canada and mid-America and provides freight transport services from the Atlantic Ocean to the Pacific Ocean and to the Gulf of Mexico. It is currently the...

-

Using the following key, identify the effects of the following transactions or conditions on the various financial statement elements: I = increases; D = decreases; NE = no effect. Note that the...

-

Massachusetts Stove Company manufactures wood-burning stoves for the heating of homes and businesses. The company has approached you, as chief lending officer for the Massachusetts Regional Bank,...

-

According to the SEC, which is not a sign of a possible fraudulent company a. Insiders having greater than 50 percent control of the BOD. b. CEO also being chairman of the BOD. c. CEO being the...

-

Prepare a one-hour action pack T.V. episode with the main character a forensic accountant or auditor. The main character should be called Dane Striker or Sloane Striker. Your project can include a...

-

SAS No. 99 gives what ways assets may be misappropriated?

Study smarter with the SolutionInn App