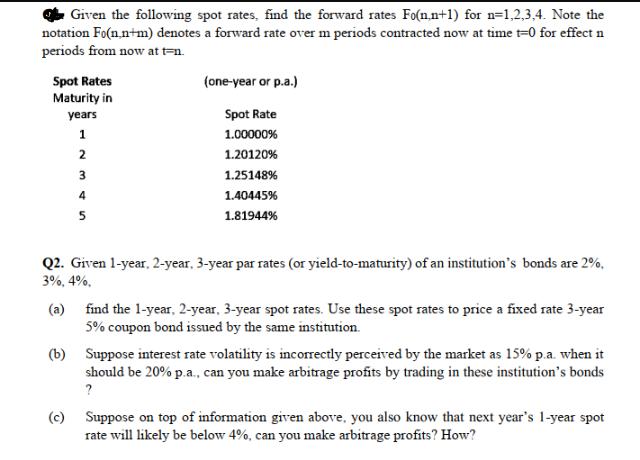

Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m)...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

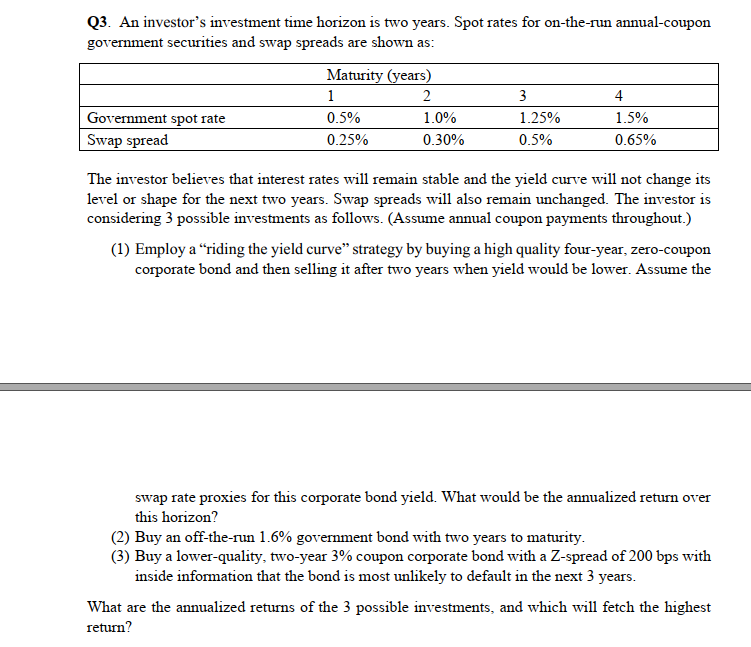

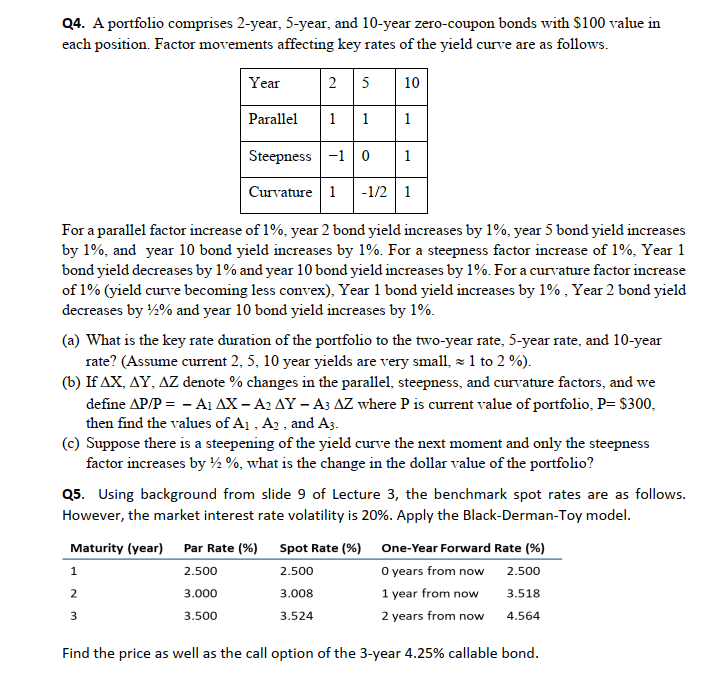

Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m) denotes a forward rate over m periods contracted now at time t=0 for effect n periods from now at t=n. Spot Rates Maturity in years 1 2 3 4 5 (one-year or p.a.) Spot Rate 1.00000% 1.20120% 1.25148% 1.40445% 1.81944% Q2. Given 1-year, 2-year, 3-year par rates (or yield-to-maturity) of an institution's bonds are 2%. 3%, 4%, (a) (c) find the 1-year, 2-year, 3-year spot rates. Use these spot rates to price a fixed rate 3-year 5% coupon bond issued by the same institution. (b) Suppose interest rate volatility is incorrectly perceived by the market as 15% p.a. when it should be 20% p.a., can you make arbitrage profits by trading in these institution's bonds ? Suppose on top of information given above, you also know that next year's 1-year spot rate will likely be below 4%, can you make arbitrage profits? How? Q3. An investor's investment time horizon is two years. Spot rates for on-the-run annual-coupon government securities and swap spreads are shown as: Government spot rate Swap spread Maturity (years) 2 1.0% 0.30% 1 0.5% 0.25% 3 1.25% 0.5% 4 1.5% 0.65% The investor believes that interest rates will remain stable and the yield curve will not change its level or shape for the next two years. Swap spreads will also remain unchanged. The investor is considering 3 possible investments as follows. (Assume annual coupon payments throughout.) (1) Employ a "riding the yield curve" strategy by buying a high quality four-year, zero-coupon corporate bond and then selling it after two years when yield would be lower. Assume the swap rate proxies for this corporate bond yield. What would be the annualized return over this horizon? (2) Buy an off-the-run 1.6% government bond with two years to maturity. (3) Buy a lower-quality, two-year 3% coupon corporate bond with a Z-spread of 200 bps with inside information that the bond is most unlikely to default in the next 3 years. What are the annualized returns of the 3 possible investments, and which will fetch the highest return? Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $100 value in each position. Factor movements affecting key rates of the yield curve are as follows. 25 Year 1 1 Steepness -1 0 Curvature Parallel For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1%, Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. 1 10 (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - A1 AX-A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of A1, A2, and A3. 2 1 1 1-1/2 1 (c) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by %, what is the change in the dollar value of the portfolio? 3 Q5. Using background from slide 9 of Lecture 3, the benchmark spot rates are as follows. However, the market interest rate volatility is 20%. Apply the Black-Derman-Toy model. Maturity (year) Par Rate (%) Spot Rate (%) 2.500 2.500 3.000 3.008 3.500 3.524 One-Year Forward Rate (%) 0 years from now 2.500 1 year from now 3.518 2 years from now 4.564 Find the price as well as the call option of the 3-year 4.25% callable bond. Given the following spot rates, find the forward rates Fo(n.n+1) for n=1,2,3,4. Note the notation Fo(n.n+m) denotes a forward rate over m periods contracted now at time t=0 for effect n periods from now at t=n. Spot Rates Maturity in years 1 2 3 4 5 (one-year or p.a.) Spot Rate 1.00000% 1.20120% 1.25148% 1.40445% 1.81944% Q2. Given 1-year, 2-year, 3-year par rates (or yield-to-maturity) of an institution's bonds are 2%. 3%, 4%, (a) (c) find the 1-year, 2-year, 3-year spot rates. Use these spot rates to price a fixed rate 3-year 5% coupon bond issued by the same institution. (b) Suppose interest rate volatility is incorrectly perceived by the market as 15% p.a. when it should be 20% p.a., can you make arbitrage profits by trading in these institution's bonds ? Suppose on top of information given above, you also know that next year's 1-year spot rate will likely be below 4%, can you make arbitrage profits? How? Q3. An investor's investment time horizon is two years. Spot rates for on-the-run annual-coupon government securities and swap spreads are shown as: Government spot rate Swap spread Maturity (years) 2 1.0% 0.30% 1 0.5% 0.25% 3 1.25% 0.5% 4 1.5% 0.65% The investor believes that interest rates will remain stable and the yield curve will not change its level or shape for the next two years. Swap spreads will also remain unchanged. The investor is considering 3 possible investments as follows. (Assume annual coupon payments throughout.) (1) Employ a "riding the yield curve" strategy by buying a high quality four-year, zero-coupon corporate bond and then selling it after two years when yield would be lower. Assume the swap rate proxies for this corporate bond yield. What would be the annualized return over this horizon? (2) Buy an off-the-run 1.6% government bond with two years to maturity. (3) Buy a lower-quality, two-year 3% coupon corporate bond with a Z-spread of 200 bps with inside information that the bond is most unlikely to default in the next 3 years. What are the annualized returns of the 3 possible investments, and which will fetch the highest return? Q4. A portfolio comprises 2-year, 5-year, and 10-year zero-coupon bonds with $100 value in each position. Factor movements affecting key rates of the yield curve are as follows. 25 Year 1 1 Steepness -1 0 Curvature Parallel For a parallel factor increase of 1%, year 2 bond yield increases by 1%, year 5 bond yield increases by 1%, and year 10 bond yield increases by 1%. For a steepness factor increase of 1%, Year 1 bond yield decreases by 1% and year 10 bond yield increases by 1%. For a curvature factor increase of 1% (yield curve becoming less convex), Year 1 bond yield increases by 1%, Year 2 bond yield decreases by 12% and year 10 bond yield increases by 1%. 1 10 (a) What is the key rate duration of the portfolio to the two-year rate, 5-year rate, and 10-year rate? (Assume current 2, 5, 10 year yields are very small, 1 to 2 %). (b) If AX, AY, AZ denote % changes in the parallel, steepness, and curvature factors, and we define AP/P = - A1 AX-A2 AY - A3 AZ where P is current value of portfolio, P= $300, then find the values of A1, A2, and A3. 2 1 1 1-1/2 1 (c) Suppose there is a steepening of the yield curve the next moment and only the steepness factor increases by %, what is the change in the dollar value of the portfolio? 3 Q5. Using background from slide 9 of Lecture 3, the benchmark spot rates are as follows. However, the market interest rate volatility is 20%. Apply the Black-Derman-Toy model. Maturity (year) Par Rate (%) Spot Rate (%) 2.500 2.500 3.000 3.008 3.500 3.524 One-Year Forward Rate (%) 0 years from now 2.500 1 year from now 3.518 2 years from now 4.564 Find the price as well as the call option of the 3-year 4.25% callable bond.

Expert Answer:

Answer rating: 100% (QA)

Q1 Forward rates F012 120120 F023 125148 F034 140445 Q2 a Spot rates 1Y 2 2Y 1 305 1 15 3Y 1 403 1 1... View the full answer

Related Book For

Fundamentals of Investments

ISBN: 978-0132926171

3rd edition

Authors: Gordon J. Alexander, William F. Sharpe, Jeffery V. Bailey

Posted Date:

Students also viewed these finance questions

-

Quiz 3.3: Price changes Consider the following bonds (same as before) trading at a yield to maturity of 8% for a principal of $1,000 1. 2-year 8% coupon bond 2. 5-year 9% coupon bond Task: Compute...

-

KYC's stock price can go up by 15 percent every year, or down by 10 percent. Both outcomes are equally likely. The risk free rate is 5 percent, and the current stock price of KYC is 100. (a) Price a...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Consider a set of documents. Assume that all documents have been normalized to have unit length of 1. What is the "shape" of a cluster that consists of all documents whose cosine similarity to a...

-

A planar steady state fluid flow has velocity vector v = (2x - 3y, x - y)T. The motion of the fluid is described by the differential equation dx/dt = v. A floating object starts out at the point (1....

-

The ASX200 Share Price Index (SPI) stands at 7,300 and has a volatility (standard deviation) of 20% per annum. The risk-free rate of interest is 3% p.a. and the index provides a dividend yield of 4%...

-

On December 31, 2016, Clarke, Inc. borrowed \(\$ 900,000\) on a seven percent, 10 -year mortgage note payable. The note is to be repaid in equal annual installments of \(\$ 128,140\) (payable on...

-

What are the auditors responsibilities to communicate information to the audit committee under AICPA and PCAOB standards? If the auditor discovers that the audit committee routinely ignores such...

-

Explain the concept of managing up and the tactics that could be used to accomplish this. Why is managing up important in organizations? Describe a time when you had to manage your supervisor....

-

Pension data for Barry Financial Services Inc., include the following: Required: 1. Determine pension expense for 2021.2. Prepare the journal entries to record? (a) Pension expense (b) Gains and...

-

1. Determine each of the following for the given matrix A, if possible. 2. If possible, find values for x and y so that the matrices A and B are equal. 3. Let a ij and b ij be general elements for...

-

Define and explain environmental sociology.? What is the name of the subdiscipline that studies the social causes and consequences of environmental problems?

-

Many ionic compounds are water soluble, so, for example, we canmake solutions of sodium iodide, NaI, and lead(II) nitrate,Pb(NO3)2, by simply dissolving the ionic solids in water. In theprocess of...

-

Barker Manufacturing uses a standard cost system. The allocation base for overhead costs is direct labor hours. Actual variable manufacturing overhead costs were $34,000 and actual fixed overhead...

-

Preble Company manufactures one product. Its variable manufacturing overhead is applied to production based on direct labor-hours and its standard cost card per unit is as follows: Direct materials:...

-

a man who is 5ft 10 in. tall weighs 160lb. what is his height incentimeters and his mass in kilograms?

-

Vicky is explaining to her Spanish-speaking friend how various holidays are celebrated in the United States. To complete the descriptions, choose the most logical words from the list and write them...

-

In Exercises delete part of the domain so that the function that remains is one-to-one. Find the inverse function of the remaining function and give the domain of the inverse function. f(x) = 16x4 -3...

-

Given the following information, calculate the three-month price of a call that is consistent with the Black-Scholes model: Ps = $47, E = $45, R = .05. = .40

-

What factors might an individual investor take into account in determining his or her investment policy?

-

Nellie Fox acquired at par a bond for $1,000 that offered a 9% coupon rate. At the time of purchase, the bond had four years to maturity. Assuming annual interest payments, calculate Nellie's actual...

-

A crystal particle of pure \(\mathrm{NaCl}\) is dissolving in an aqueous liquid (water) solution at \(18^{\circ} \mathrm{C}\). The dissolution of the particle is controlled by mass transfer. The...

-

A \(2 \mathrm{~cm}\)-diameter, \(19 \mathrm{~cm}\)-long tube is placed touching a pool of liquid. The end away from the liquid pool \((\mathrm{z}=0.19 \mathrm{~m})\) is in an air stream (component C)...

-

\(\mathrm{NaCl}\) is crystallizing from an aqueous (water) liquid solution onto a crystal particle of pure \(\mathrm{NaCl}\) at \(18^{\circ} \mathrm{C}\). Assume particle growth is controlled by mass...

Study smarter with the SolutionInn App