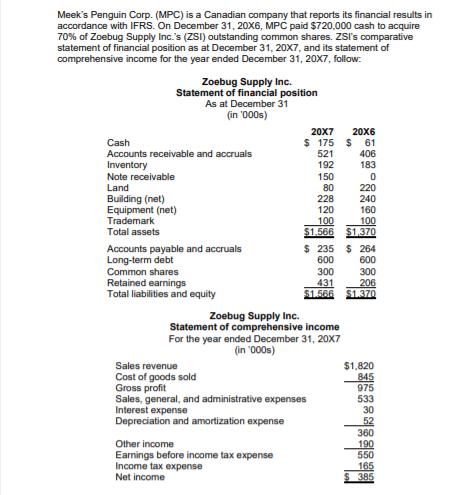

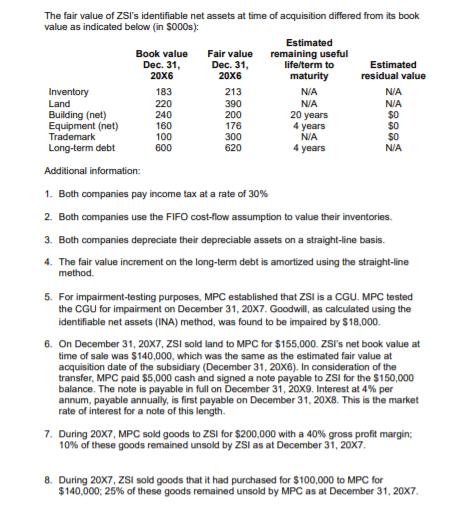

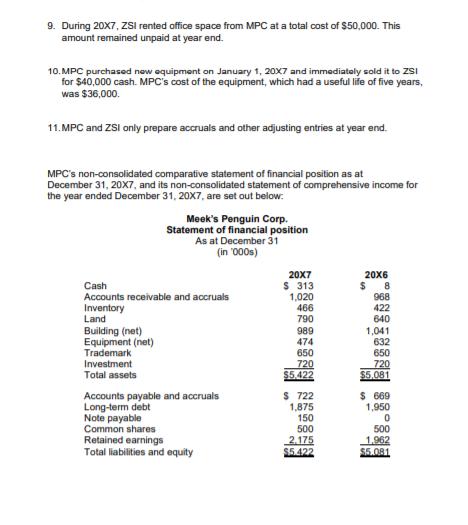

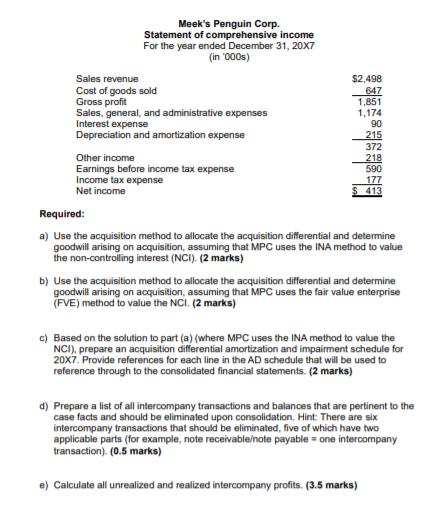

Meek's Penguin Corp. (MPC) is a Canadian company that reports its financial results in accordance with...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text: