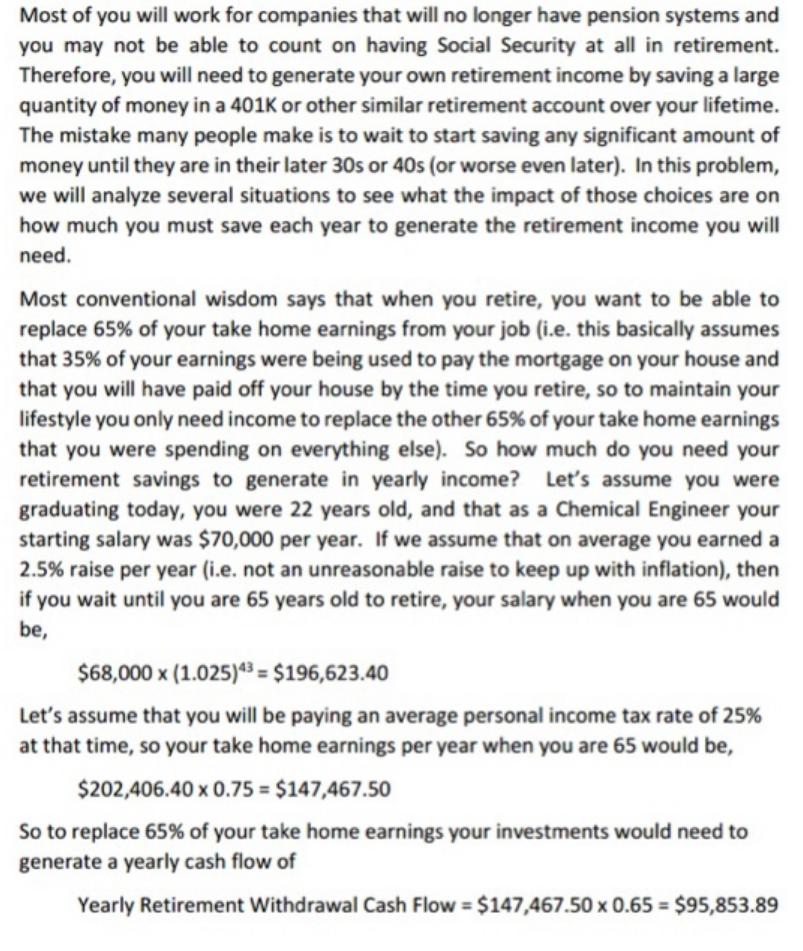

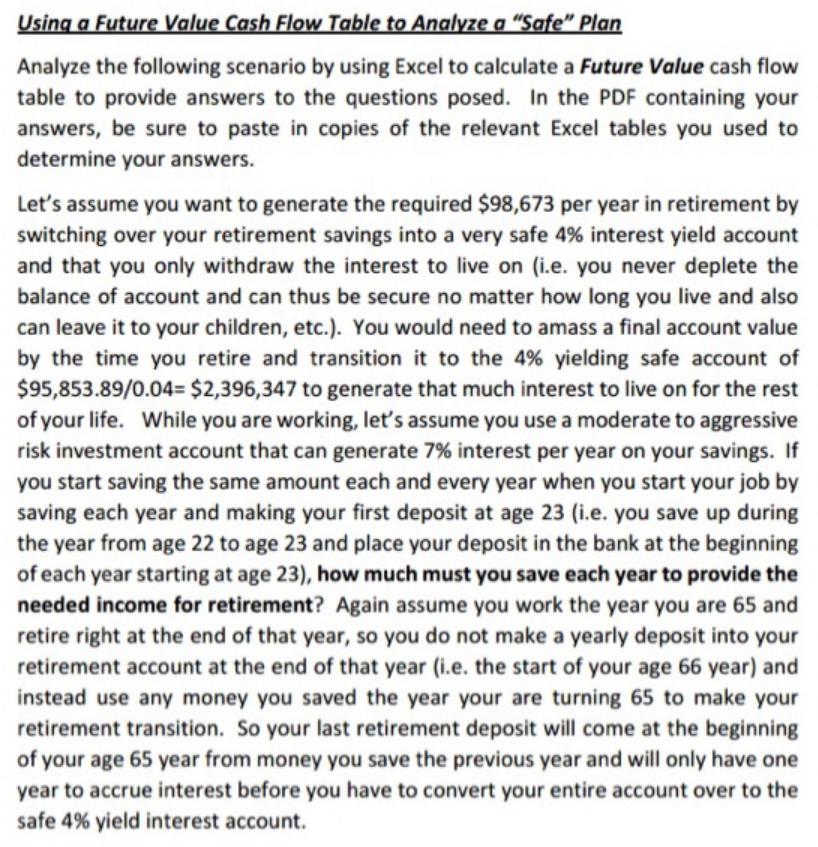

Most of you will work for companies that will no longer have pension systems and you...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Most of you will work for companies that will no longer have pension systems and you may not be able to count on having Social Security at all in retirement. Therefore, you will need to generate your own retirement income by saving a large quantity of money in a 401K or other similar retirement account over your lifetime. The mistake many people make is to wait to start saving any significant amount of money until they are in their later 30s or 40s (or worse even later). In this problem, we will analyze several situations to see what the impact of those choices are on how much you must save each year to generate the retirement income you will need. Most conventional wisdom says that when you retire, you want to be able to replace 65% of your take home earnings from your job (i.e. this basically assumes that 35% of your earnings were being used to pay the mortgage on your house and that you will have paid off your house by the time you retire, so to maintain your lifestyle you only need income to replace the other 65% of your take home earnings that you were spending on everything else). So how much do you need your retirement savings to generate in yearly income? Let's assume you were graduating today, you were 22 years old, and that as a Chemical Engineer your starting salary was $70,000 per year. If we assume that on average you earned a 2.5% raise per year (i.e. not an unreasonable raise to keep up with inflation), then if you wait until you are 65 years old to retire, your salary when you are 65 would be, $68,000 x (1.025)43 = $196,623.40 Let's assume that you will be paying an average personal income tax rate of 25% at that time, so your take home earnings per year when you are 65 would be, $202,406.40 x 0.75= $147,467.50 So to replace 65% of your take home earnings your investments would need to generate a yearly cash flow of Yearly Retirement Withdrawal Cash Flow = $147,467.50 x 0.65= $95,853.89 Using a Future Value Cash Flow Table to Analyze a "Safe" Plan Analyze the following scenario by using Excel to calculate a Future Value cash flow table to provide answers to the questions posed. In the PDF containing your answers, be sure to paste in copies of the relevant Excel tables you used to determine your answers. Let's assume you want to generate the required $98,673 per year in retirement by switching over your retirement savings into a very safe 4% interest yield account and that you only withdraw the interest to live on (i.e. you never deplete the balance of account and can thus be secure no matter how long you live and also can leave it to your children, etc.). You would need to amass a final account value by the time you retire and transition it to the 4% yielding safe account of $95,853.89/0.04= $2,396,347 to generate that much interest to live on for the rest of your life. While you are working, let's assume you use a moderate to aggressive risk investment account that can generate 7% interest per year on your savings. If you start saving the same amount each and every year when you start your job by saving each year and making your first deposit at age 23 (i.e. you save up during the year from age 22 to age 23 and place your deposit in the bank at the beginning of each year starting at age 23), how much must you save each year to provide the needed income for retirement? Again assume you work the year you are 65 and retire right at the end of that year, so you do not make a yearly deposit into your retirement account at the end of that year (i.e. the start of your age 66 year) and instead use any money you saved the year your are turning 65 to make your retirement transition. So your last retirement deposit will come at the beginning of your age 65 year from money you save the previous year and will only have one year to accrue interest before you have to convert your entire account over to the safe 4% yield interest account. Most of you will work for companies that will no longer have pension systems and you may not be able to count on having Social Security at all in retirement. Therefore, you will need to generate your own retirement income by saving a large quantity of money in a 401K or other similar retirement account over your lifetime. The mistake many people make is to wait to start saving any significant amount of money until they are in their later 30s or 40s (or worse even later). In this problem, we will analyze several situations to see what the impact of those choices are on how much you must save each year to generate the retirement income you will need. Most conventional wisdom says that when you retire, you want to be able to replace 65% of your take home earnings from your job (i.e. this basically assumes that 35% of your earnings were being used to pay the mortgage on your house and that you will have paid off your house by the time you retire, so to maintain your lifestyle you only need income to replace the other 65% of your take home earnings that you were spending on everything else). So how much do you need your retirement savings to generate in yearly income? Let's assume you were graduating today, you were 22 years old, and that as a Chemical Engineer your starting salary was $70,000 per year. If we assume that on average you earned a 2.5% raise per year (i.e. not an unreasonable raise to keep up with inflation), then if you wait until you are 65 years old to retire, your salary when you are 65 would be, $68,000 x (1.025)43 = $196,623.40 Let's assume that you will be paying an average personal income tax rate of 25% at that time, so your take home earnings per year when you are 65 would be, $202,406.40 x 0.75= $147,467.50 So to replace 65% of your take home earnings your investments would need to generate a yearly cash flow of Yearly Retirement Withdrawal Cash Flow = $147,467.50 x 0.65= $95,853.89 Using a Future Value Cash Flow Table to Analyze a "Safe" Plan Analyze the following scenario by using Excel to calculate a Future Value cash flow table to provide answers to the questions posed. In the PDF containing your answers, be sure to paste in copies of the relevant Excel tables you used to determine your answers. Let's assume you want to generate the required $98,673 per year in retirement by switching over your retirement savings into a very safe 4% interest yield account and that you only withdraw the interest to live on (i.e. you never deplete the balance of account and can thus be secure no matter how long you live and also can leave it to your children, etc.). You would need to amass a final account value by the time you retire and transition it to the 4% yielding safe account of $95,853.89/0.04= $2,396,347 to generate that much interest to live on for the rest of your life. While you are working, let's assume you use a moderate to aggressive risk investment account that can generate 7% interest per year on your savings. If you start saving the same amount each and every year when you start your job by saving each year and making your first deposit at age 23 (i.e. you save up during the year from age 22 to age 23 and place your deposit in the bank at the beginning of each year starting at age 23), how much must you save each year to provide the needed income for retirement? Again assume you work the year you are 65 and retire right at the end of that year, so you do not make a yearly deposit into your retirement account at the end of that year (i.e. the start of your age 66 year) and instead use any money you saved the year your are turning 65 to make your retirement transition. So your last retirement deposit will come at the beginning of your age 65 year from money you save the previous year and will only have one year to accrue interest before you have to convert your entire account over to the safe 4% yield interest account.

Expert Answer:

Answer rating: 100% (QA)

To determine the amount that you need to save each year in order to achieve your retirement goals yo... View the full answer

Related Book For

Federal Taxation 2018 Comprehensive

ISBN: 9780134532387

31st edition

Authors: Thomas R. Pope, Timothy J. Rupert, Kenneth E. Anderson

Posted Date:

Students also viewed these law questions

-

Many of you will work for a small business. Some of you will even own your own business. In order to operate a small business, you will need a good understanding of managerial accounting, as well as...

-

Many of you will work for a small business. As noted in the All About You feature in this chapter, some of you will even own your own business. In order to operate a small business you will need a...

-

Many of you will work for a small business. Some of you will even own your own business. In order to operate a small business, you will need a good understanding of managerial accounting, as well as...

-

This exercise shows that the multiplier may be interpreted as a rate of change in general. Assume that the maximum of (x, y) subject to g(x, y) = c occurs at a point P. Then P depends on the value...

-

Kruuk et al. (1989) used a stratified sample to estimate the number of otter (Lutra lutra) dens along the 1400-km coastline of Shetland, UK. The coastline was divided into 242 (237 that were not...

-

A life insurance company sells a term insurance policy to 21-year-old males that pays $100,000 if the insured dies within the next 5 years. The probability that a randomly chosen male will die each...

-

Identify the five steps in the application of the decision-oriented approach to ac- counting.

-

MKM International is seeking to purchase a new CNC machine in order to reduce costs. Two alternative machines are in consideration. Machine 1 costs $500,000, but yields a 15 percent savings over the...

-

Review the situations below and explain if the matters raised can affect the independence of the Auditor, showing clearly the threats involved (if any) and the safeguards and/or preventative measures...

-

Amanda Boleyn, an entrepreneur who recently sold her start-up for a multi-million-dollar sum, is looking for alternate investments for her newfound fortune. She is considering an investment in wine,...

-

Chapter 13 Homework eBook Show Me How Entries for Issuing No-Par Stock On February 12, Quality Carpet Inc., a carpet wholesaler, issued for cash 1,000,000 shares of no-par common stock (with a stated...

-

What can we learn from the ethnic group adaptations in U.S. society?

-

What species might be the earliest hominins, and what does their anatomy and environment tell us about the selective pressures that might have facilitated their evolution?

-

Keynesianism has been subject to much debate over the years. To what extent is the idea that demand management in a period of economic stagnation a recipe for stimulating economic growth once again?...

-

What role did kinship and descent play in the social structure of a chiefdom?

-

What are some methods used to reconstruct past climate, and how did that climate change from the Paleocene to present?

-

Question 43RWJ 6-8Yorba Linda Corp issued preferred stock offering 5.48 percentdividend yield.The preferred stock is currently priced at $59.30 per share.What is the amount of the annual dividend 2...

-

What is your assessment of the negotiations process, given what you have studied? What are your recommendations for Mr. Reed? You must justify your conclusions

-

Sylvia, a dentist with excellent skills as a carpenter, started the construction of a house that she planned to give to her son as a surprise when he returned from Afghanistan, where he is serving in...

-

Sometimes taxpayers may not be able to file their tax returns by the normal due date. Are extensions available? How long are the extensions? Do extensions enable taxpayers to delay paying the tax...

-

Tim retired during the current year at age 58. He purchased an annuity from American National Life Company for $40,000. The annuity pays Tim $500 per month for life. a. Compute Tims annual exclusion....

-

Take each figure in the 2001 columns and measure its percentage change over 2000. Identify where the most signifi- cant changes have occurred.

-

As with the balance sheet, compare the current-year reported figures in the profit and loss account with the information shown for the prior year. Calculate the percentage change from one year to the...

-

What two events led to the transformation and spread of accounting between the 12th and 15th centuries?

Study smarter with the SolutionInn App