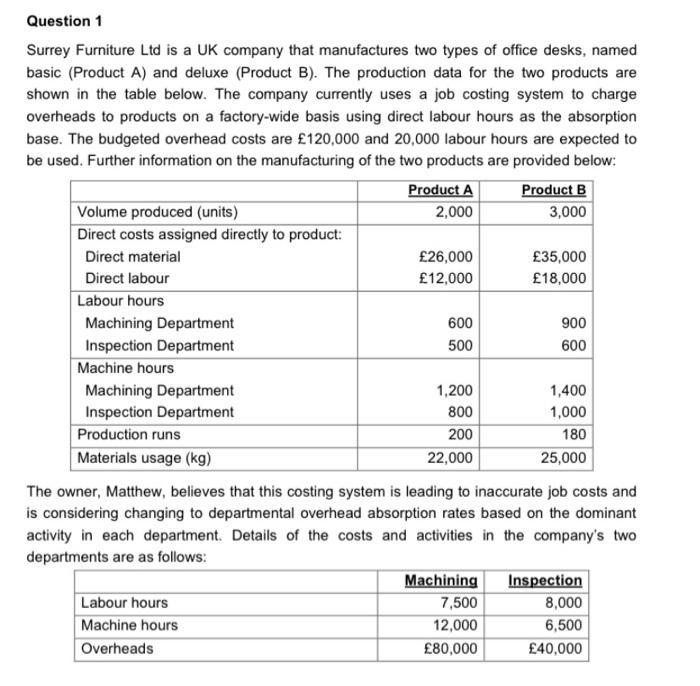

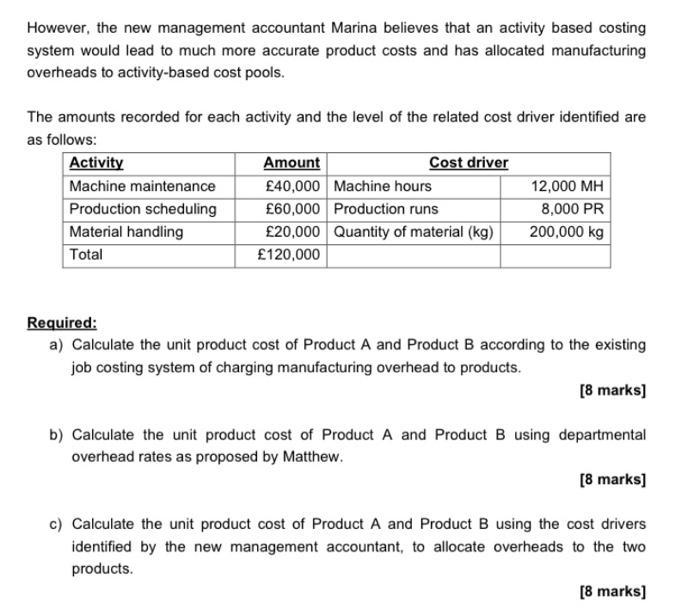

Question 1 Surrey Furniture Ltd is a UK company that manufactures two types of office desks,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

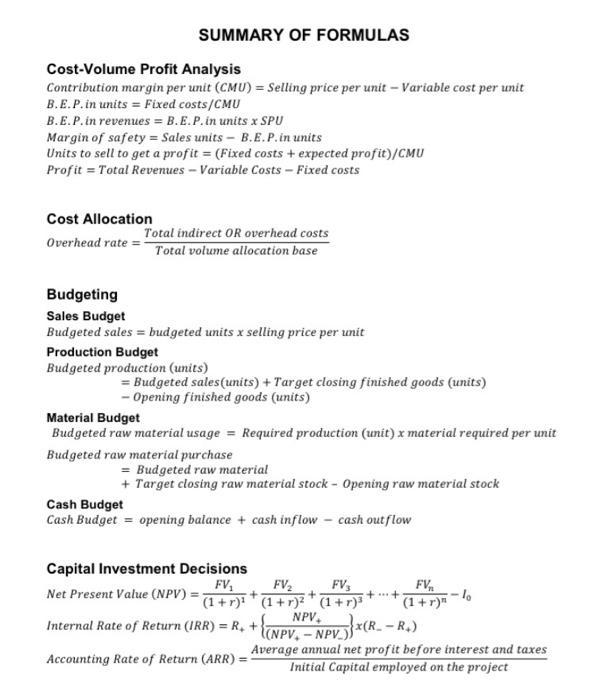

Question 1 Surrey Furniture Ltd is a UK company that manufactures two types of office desks, named basic (Product A) and deluxe (Product B). The production data for the two products are shown in the table below. The company currently uses a job costing system to charge overheads to products on a factory-wide basis using direct labour hours as the absorption base. The budgeted overhead costs are £120,000 and 20,000 labour hours are expected to be used. Further information on the manufacturing of the two products are provided below: Product A Product B Volume produced (units) 2,000 3,000 Direct costs assigned directly to product: Direct material £26,000 £35,000 Direct labour £12,000 £18,000 Labour hours Machining Department 600 900 Inspection Department 500 600 Machine hours Machining Department 1,200 1,400 800 1,000 Inspection Department Production runs 200 180 Materials usage (kg) 22,000 25,000 The owner, Matthew, believes that this costing system is leading to inaccurate job costs and is considering changing to departmental overhead absorption rates based on the dominant activity in each department. Details of the costs and activities in the company's two departments are as follows: Inspection Machining 7,500 Labour hours 8,000 Machine hours 12,000 6,500 Overheads £80,000 £40,000 However, the new management accountant Marina believes that an activity based costing system would lead to much more accurate product costs and has allocated manufacturing overheads to activity-based cost pools. The amounts recorded for each activity and the level of the related cost driver identified are as follows: Activity Amount Cost driver Machine maintenance 12,000 MH £40,000 Machine hours £60,000 Production runs Production scheduling 8,000 PR 200,000 kg Material handling £20,000 Quantity of material (kg) Total £120,000 Required: a) Calculate the unit product cost of Product A and Product B according to the existing job costing system of charging manufacturing overhead to products. [8 marks] b) Calculate the unit product cost of Product A and Product B using departmental overhead rates as proposed by Matthew. [8 marks] c) Calculate the unit product cost of Product A and Product B using the cost drivers identified by the new management accountant, to allocate overheads to the two products. [8 marks] SUMMARY OF FORMULAS Cost-Volume Profit Analysis Contribution margin per unit (CMU) = Selling price per unit - Variable cost per unit B.E.P. in units = Fixed costs/CMU B.E.P. in revenues = B.E.P. in units x SPU Margin of safety = Sales units - B.E.P. in units Units to sell to get a profit = (Fixed costs + expected profit)/CMU Profit = Total Revenues-Variable Costs - Fixed costs Cost Allocation Overhead rate=1 Total indirect OR overhead costs Total volume allocation base Budgeting Sales Budget Budgeted sales = budgeted units x selling price per unit Production Budget Budgeted production (units) = Budgeted sales (units) + Target closing finished goods (units) - Opening finished goods (units) Material Budget Budgeted raw material usage = Required production (unit) x material required per unit Budgeted raw material purchase = Budgeted raw material + Target closing raw material stock - Opening raw material stock Cash Budget Cash Budget = opening balance + cash inflow - cash out flow Capital Investment Decisions FV₁ Net Present Value (NPV) = + FV₂ FV3 (1+r)² (1+r)³ ++ FV₂ (1+r)" lo (1+r)¹ NPV, Internal Rate of Return (IRR) = R₁ + {x(R_ -R₂) (NPV-NPV)}*(R. Accounting Rate of Return (ARR) = Average annual net profit before interest and taxes Initial Capital employed on the project Question 1 Surrey Furniture Ltd is a UK company that manufactures two types of office desks, named basic (Product A) and deluxe (Product B). The production data for the two products are shown in the table below. The company currently uses a job costing system to charge overheads to products on a factory-wide basis using direct labour hours as the absorption base. The budgeted overhead costs are £120,000 and 20,000 labour hours are expected to be used. Further information on the manufacturing of the two products are provided below: Product A Product B Volume produced (units) 2,000 3,000 Direct costs assigned directly to product: Direct material £26,000 £35,000 Direct labour £12,000 £18,000 Labour hours Machining Department 600 900 Inspection Department 500 600 Machine hours Machining Department 1,200 1,400 800 1,000 Inspection Department Production runs 200 180 Materials usage (kg) 22,000 25,000 The owner, Matthew, believes that this costing system is leading to inaccurate job costs and is considering changing to departmental overhead absorption rates based on the dominant activity in each department. Details of the costs and activities in the company's two departments are as follows: Inspection Machining 7,500 Labour hours 8,000 Machine hours 12,000 6,500 Overheads £80,000 £40,000 However, the new management accountant Marina believes that an activity based costing system would lead to much more accurate product costs and has allocated manufacturing overheads to activity-based cost pools. The amounts recorded for each activity and the level of the related cost driver identified are as follows: Activity Amount Cost driver Machine maintenance 12,000 MH £40,000 Machine hours £60,000 Production runs Production scheduling 8,000 PR 200,000 kg Material handling £20,000 Quantity of material (kg) Total £120,000 Required: a) Calculate the unit product cost of Product A and Product B according to the existing job costing system of charging manufacturing overhead to products. [8 marks] b) Calculate the unit product cost of Product A and Product B using departmental overhead rates as proposed by Matthew. [8 marks] c) Calculate the unit product cost of Product A and Product B using the cost drivers identified by the new management accountant, to allocate overheads to the two products. [8 marks] SUMMARY OF FORMULAS Cost-Volume Profit Analysis Contribution margin per unit (CMU) = Selling price per unit - Variable cost per unit B.E.P. in units = Fixed costs/CMU B.E.P. in revenues = B.E.P. in units x SPU Margin of safety = Sales units - B.E.P. in units Units to sell to get a profit = (Fixed costs + expected profit)/CMU Profit = Total Revenues-Variable Costs - Fixed costs Cost Allocation Overhead rate=1 Total indirect OR overhead costs Total volume allocation base Budgeting Sales Budget Budgeted sales = budgeted units x selling price per unit Production Budget Budgeted production (units) = Budgeted sales (units) + Target closing finished goods (units) - Opening finished goods (units) Material Budget Budgeted raw material usage = Required production (unit) x material required per unit Budgeted raw material purchase = Budgeted raw material + Target closing raw material stock - Opening raw material stock Cash Budget Cash Budget = opening balance + cash inflow - cash out flow Capital Investment Decisions FV₁ Net Present Value (NPV) = + FV₂ FV3 (1+r)² (1+r)³ ++ FV₂ (1+r)" lo (1+r)¹ NPV, Internal Rate of Return (IRR) = R₁ + {x(R_ -R₂) (NPV-NPV)}*(R. Accounting Rate of Return (ARR) = Average annual net profit before interest and taxes Initial Capital employed on the project

Expert Answer:

Answer rating: 100% (QA)

According to the data Any Survey furniture Ltd is a uk company d The Summary of unmit c... View the full answer

Related Book For

Practical Management Science

ISBN: 978-1305250901

5th edition

Authors: Wayne L. Winston, Christian Albright

Posted Date:

Students also viewed these general management questions

-

A large firm of solicitors uses a job costing system to identify costs with individual clients. Hours worked by professional staff are used as the basis for charging overhead costs to client...

-

A company manufactures two types of trucks. Each truck must go through the painting shop and the assembly shop. If the painting shop were completely devoted to painting type 1 trucks, 800 per day...

-

A company manufactures two types of electric hedge trimmers, one of which is cordless. The cord-type trimmer requires 2 hours to make, and the cordless model requires 4 hours. The company has only...

-

Write a program that takes an integer command-line argument n and prints all the positive powers of 2 less than or equal to n. Make sure that your program works properly for all values of n.

-

Who pays the social security taxes that are levied by the Federal Insurance Contributions Act?

-

A pump is required for a U.S. fie ld application with the following specifications: a flow rate of I 2.5 cfs (ft 3/ sec) against a head of 95 ft. To design the pump, a model is built with a 6 in....

-

Think of a time when you have been very satisfied with a job you have held. What made that job satisfying? Also think of a time when you have been dissatisfied with a job you have held. What made...

-

The unadjusted trial balance of World Enterprises for the year ending December 31, 2014, follows: Additional information: 1. There is $750 of supplies on hand on December 31, 2014. 2. The one-year...

-

When preparing a business report it is essential to keep in mind that

-

Let us consider the a small village. The power network of the village is shown in Figure 1. Load demands at Zone A, Zone B and Zone C, are 5MVA (0.95pf lagging), 7MVA (0.94pf lagging) and 7MVA...

-

a. Present a cost-profit-volume analysis that shows the effect of adding the $8,500 annual premium to the companys fixed costs by showing current and revised CVP Income Statements. Include a column...

-

The project manager always involves the team in the creation of the work breakdown structure. What is the most significant benefit derived from this approach? a. Generation of a more accurate...

-

What are three input controls?

-

What is the difference between spur and helical gear ?

-

Explain the purpose of the input file definition feature of ACL.

-

Of the following, which is the most comprehensive definition of project risk? a. Risk is a positive or negative event that may or may not have occurred b. Risk is a negative event that may or may not...

-

Sampling rate conversion by a rational factor The sampling rate of a digital signal can be changed through a sequence of upsamping, lowpass filtering, and downsampling. In this problem we consider...

-

6 (a) Briefly develop a mathematical model of the behaviour of a copper-twisted pair cable (b) Derive the magnetic energy from: w given that: K + w, where the - - k symbols have their usual meaning...

-

A European put option allows an investor to sell a share of stock at the exercise price on the exercise data. For example, if the exercise price is $48, and the stock price is $45 on the exercise...

-

Continuing the previous problem, perform a sensitivity analysis on the selling price of VXPs. Let this price vary from $500 to $650 in increments of $10, and keep track of the values in the changing...

-

Sometimes a "single-stage" decision can be broken down into a sequence of decisions, with no uncertainty resolved between these decisions. Similarly, uncertainty can sometimes be broken down into a...

-

For Example 16-1, estimate an average \(\mathrm{H}_{\mathrm{OG}}\) in the stripping section. Then calculate \(\mathrm{n}_{\mathrm{OG}}\) and \(\mathrm{h}_{\mathrm{E}}=\mathrm{H}_{\mathrm{OG}, \text {...

-

In part E of Example 16-2, a HETP value of \(2.15 \mathrm{ft}\) is calculated for the top of the enriching section. Since the average error in individual mass transfer coefficients...

-

A distillation column at \(101.3 \mathrm{kPa}\) is separating a two-phase feed that is \(60.0 \%\) liquid, \(40.0 \mathrm{~mol} \%\) methanol, and \(60.0 \mathrm{~mol} \%\) water. Distillate product...

Study smarter with the SolutionInn App