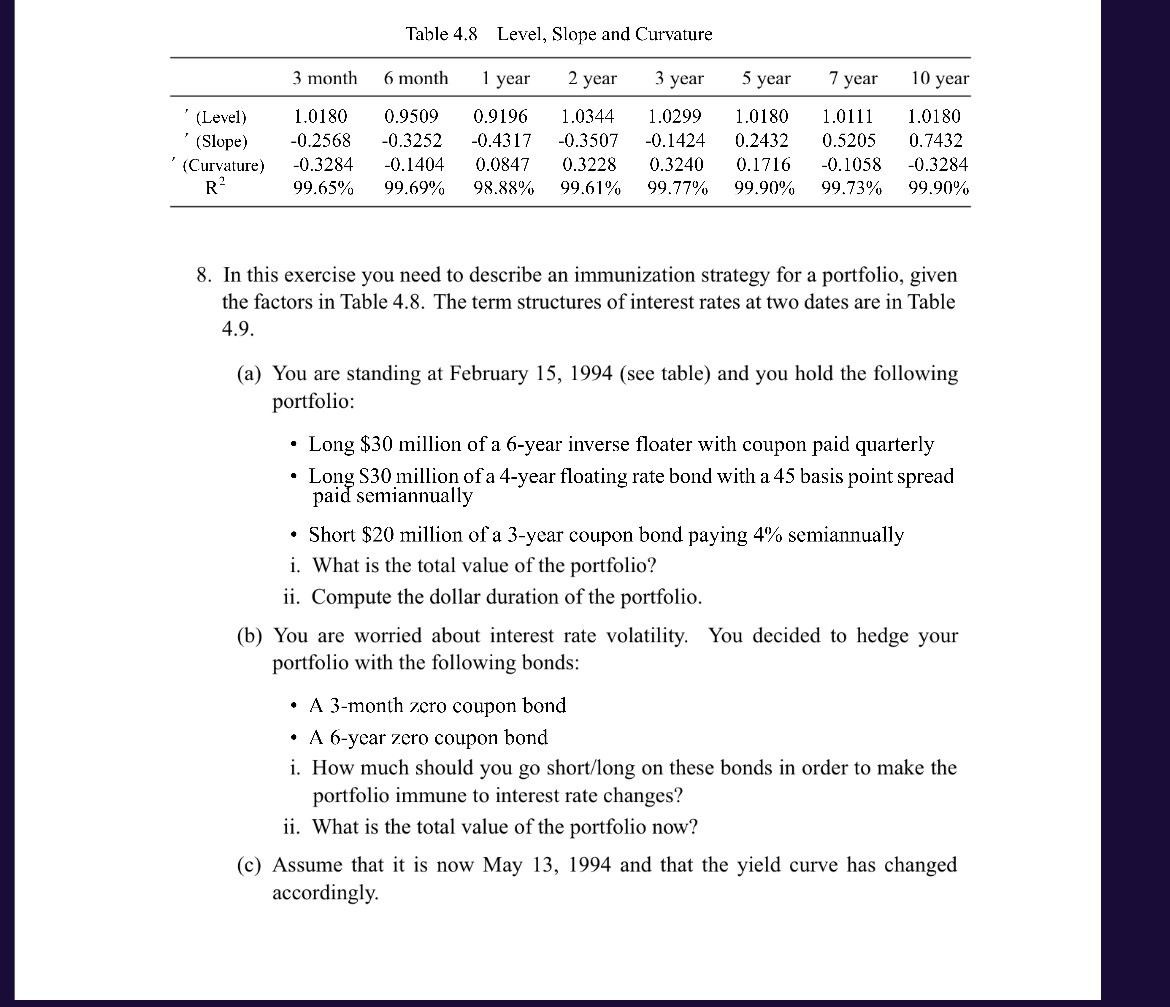

Table 4.8 Level, Slope and Curvature 3 month 6 month 1 year 2 year 7 year...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

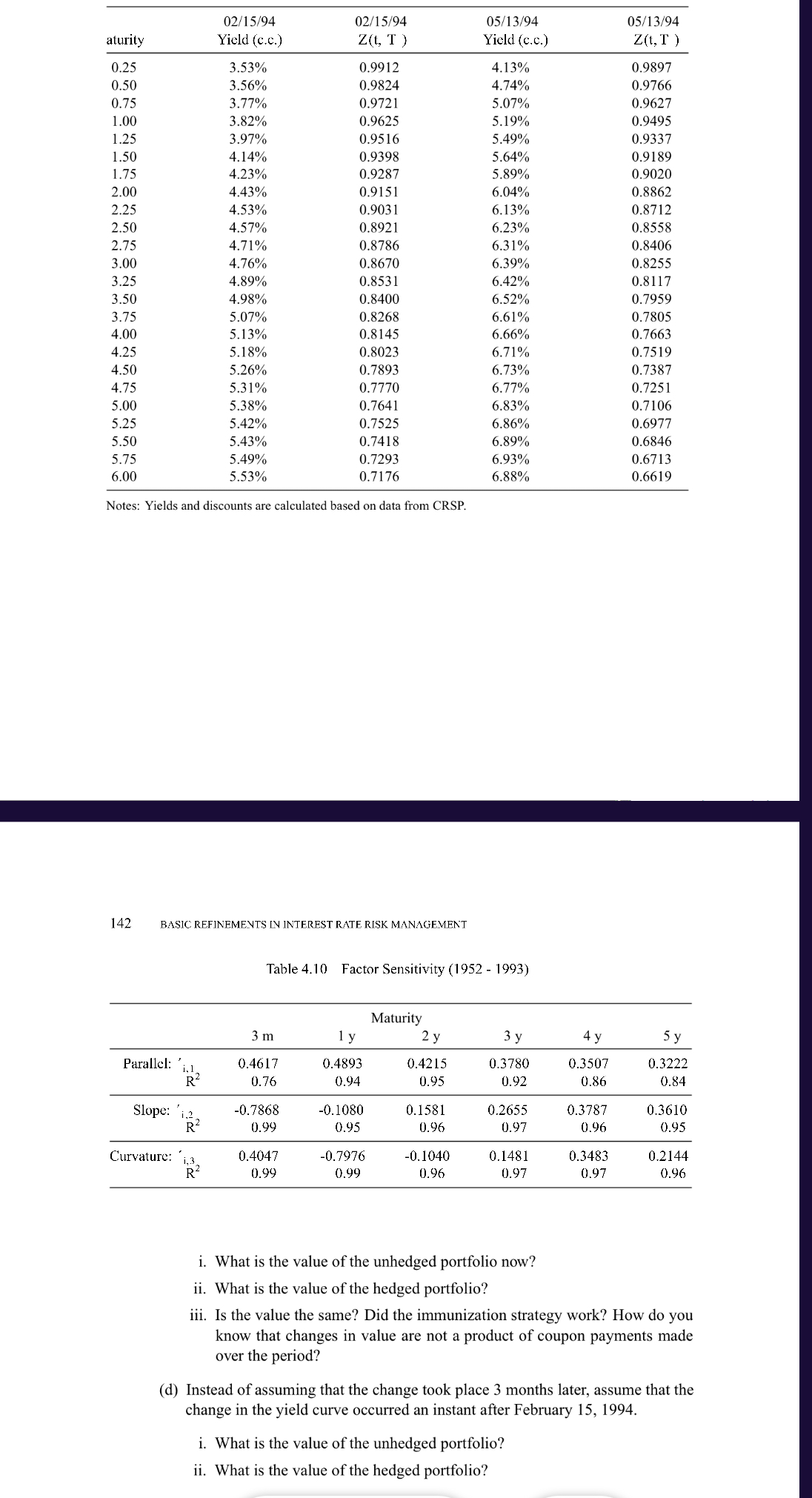

Table 4.8 Level, Slope and Curvature 3 month 6 month 1 year 2 year 7 year 10 year 1.0111 1.0180 ' (Level) 1.0344 1.0299 -0.3507 -0.1424 1.0180 0.2432 0.5205 0.7432 1.0180 0.9509 0.9196 (Slope) -0.2568 -0.3252 -0.4317 (Curvature) -0.3284 -0.1404 0.0847 0.3228 0.3240 0.1716 -0.1058 -0.3284 R 99.65% 99.69% 98.88% 99.61% 99.77% 99.90% 99.73% 99.90% 3 year 5 year 8. In this exercise you need to describe an immunization strategy for a portfolio, given the factors in Table 4.8. The term structures of interest rates at two dates are in Table 4.9. (a) You are standing at February 15, 1994 (see table) and you hold the following portfolio: Long $30 million of a 6-year inverse floater with coupon paid quarterly Long $30 million of a 4-year floating rate bond with a 45 basis point spread paid semiannually Short $20 million of a 3-year coupon bond paying 4% semiannually i. What is the total value of the portfolio? ii. Compute the dollar duration of the portfolio. (b) You are worried about interest rate volatility. You decided to hedge your portfolio with the following bonds: A 3-month zero coupon bond A 6-year zero coupon bond i. How much should you go short/long on these bonds in order to make the portfolio immune to interest rate changes? ii. What is the total value of the portfolio now? (c) Assume that it is now May 13, 1994 and that the yield curve has changed accordingly. aturity 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50 4.75 5.00 5.25 Parallel: ' i.l Curvature: R Slope: 2 R 02/15/94 Yield (c.c.) 5.50 5.75 6.00 Notes: Yields and discounts are calculated based on data from CRSP. 3.53% 3.56% i,3. 3.77% 3.82% 3.97% 4.14% 4.23% 4.43% 4.53% 4.57% 4.71% 4.76% 4.89% 4.98% 5.07% 5.13% 5.18% 5.26% 5.31% 5.38% 142 BASIC REFINEMENTS IN INTEREST RATE RISK MANAGEMENT 5.42% 5.43% 5.49% 5.53% 02/15/94 Z(t, T) 3 m 0.4617 0.76 0.9912 0.9824 0.9721 0.9625 0.9516 0.9398 0.9287 0.9151 0.9031 0.8921 0.8786 0.8670 0.8531 0.8400 0.8268 0.8145 0.8023 0.7893 0.7770 0.7641 0.7525 0.7418 0.7293 0.7176 -0.7868 0.99 0.4047 0.99 Table 4.10 Factor Sensitivity (1952 - 1993) 1 y 0.4893 0.94 -0.1080 0.95 -0.7976 0.99 Maturity 2 y 0.4215 0.95 0.1581 0.96 05/13/94 Yield (c.c.) -0.1040 0.96 4.13% 4.74% 5.07% 5.19% 5.49% 5.64% 5.89% 6.04% 6.13% 6.23% 6.31% 6.39% 6.42% 6.52% 6.61% 6.66% 6.71% 6.73% 6.77% 6.83% 6.86% 6.89% 6.93% 6.88% 3 y 0.3780 0.92 0.2655 0.97 0.1481 0.97 4 y 0.3507 0.86 0.3787 0.96 i. What is the value of the unhedged portfolio? ii. What is the value of the hedged portfolio? 0.3483 0.97 05/13/94 Z(t, T) 0.9897 0.9766 0.9627 0.9495 0.9337 0.9189 0.9020 0.8862 0.8712 0.8558 0.8406 0.8255 0.8117 0.7959 0.7805 0.7663 0.7519 0.7387 0.7251 0.7106 0.6977 0.6846 0.6713 0.6619 5 y 0.3222 0.84 0.3610 0.95 0.2144 0.96 i. What is the value of the unhedged portfolio now? ii. What is the value of the hedged portfolio? iii. Is the value the same? Did the immunization strategy work? How do you know that changes in value are not a product of coupon payments made over the period? (d) Instead of assuming that the change took place 3 months later, assume that the change in the yield curve occurred an instant after February 15, 1994. Table 4.8 Level, Slope and Curvature 3 month 6 month 1 year 2 year 7 year 10 year 1.0111 1.0180 ' (Level) 1.0344 1.0299 -0.3507 -0.1424 1.0180 0.2432 0.5205 0.7432 1.0180 0.9509 0.9196 (Slope) -0.2568 -0.3252 -0.4317 (Curvature) -0.3284 -0.1404 0.0847 0.3228 0.3240 0.1716 -0.1058 -0.3284 R 99.65% 99.69% 98.88% 99.61% 99.77% 99.90% 99.73% 99.90% 3 year 5 year 8. In this exercise you need to describe an immunization strategy for a portfolio, given the factors in Table 4.8. The term structures of interest rates at two dates are in Table 4.9. (a) You are standing at February 15, 1994 (see table) and you hold the following portfolio: Long $30 million of a 6-year inverse floater with coupon paid quarterly Long $30 million of a 4-year floating rate bond with a 45 basis point spread paid semiannually Short $20 million of a 3-year coupon bond paying 4% semiannually i. What is the total value of the portfolio? ii. Compute the dollar duration of the portfolio. (b) You are worried about interest rate volatility. You decided to hedge your portfolio with the following bonds: A 3-month zero coupon bond A 6-year zero coupon bond i. How much should you go short/long on these bonds in order to make the portfolio immune to interest rate changes? ii. What is the total value of the portfolio now? (c) Assume that it is now May 13, 1994 and that the yield curve has changed accordingly. aturity 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50 4.75 5.00 5.25 Parallel: ' i.l Curvature: R Slope: 2 R 02/15/94 Yield (c.c.) 5.50 5.75 6.00 Notes: Yields and discounts are calculated based on data from CRSP. 3.53% 3.56% i,3. 3.77% 3.82% 3.97% 4.14% 4.23% 4.43% 4.53% 4.57% 4.71% 4.76% 4.89% 4.98% 5.07% 5.13% 5.18% 5.26% 5.31% 5.38% 142 BASIC REFINEMENTS IN INTEREST RATE RISK MANAGEMENT 5.42% 5.43% 5.49% 5.53% 02/15/94 Z(t, T) 3 m 0.4617 0.76 0.9912 0.9824 0.9721 0.9625 0.9516 0.9398 0.9287 0.9151 0.9031 0.8921 0.8786 0.8670 0.8531 0.8400 0.8268 0.8145 0.8023 0.7893 0.7770 0.7641 0.7525 0.7418 0.7293 0.7176 -0.7868 0.99 0.4047 0.99 Table 4.10 Factor Sensitivity (1952 - 1993) 1 y 0.4893 0.94 -0.1080 0.95 -0.7976 0.99 Maturity 2 y 0.4215 0.95 0.1581 0.96 05/13/94 Yield (c.c.) -0.1040 0.96 4.13% 4.74% 5.07% 5.19% 5.49% 5.64% 5.89% 6.04% 6.13% 6.23% 6.31% 6.39% 6.42% 6.52% 6.61% 6.66% 6.71% 6.73% 6.77% 6.83% 6.86% 6.89% 6.93% 6.88% 3 y 0.3780 0.92 0.2655 0.97 0.1481 0.97 4 y 0.3507 0.86 0.3787 0.96 i. What is the value of the unhedged portfolio? ii. What is the value of the hedged portfolio? 0.3483 0.97 05/13/94 Z(t, T) 0.9897 0.9766 0.9627 0.9495 0.9337 0.9189 0.9020 0.8862 0.8712 0.8558 0.8406 0.8255 0.8117 0.7959 0.7805 0.7663 0.7519 0.7387 0.7251 0.7106 0.6977 0.6846 0.6713 0.6619 5 y 0.3222 0.84 0.3610 0.95 0.2144 0.96 i. What is the value of the unhedged portfolio now? ii. What is the value of the hedged portfolio? iii. Is the value the same? Did the immunization strategy work? How do you know that changes in value are not a product of coupon payments made over the period? (d) Instead of assuming that the change took place 3 months later, assume that the change in the yield curve occurred an instant after February 15, 1994.

Expert Answer:

Answer rating: 100% (QA)

Answer From the First Image a You are holding a portfolio consisting of Long 30 million of a 6year inverse floater with quarterly payments Long 30 mil... View the full answer

Related Book For

Fixed Income Securities Valuation Risk and Risk Management

ISBN: 978-0470109106

1st edition

Authors: Pietro Veronesi

Posted Date:

Students also viewed these finance questions

-

A1/ A15 my ape My x Dashbo LU ENC Q ChatGF New ta New ta a exprep ExPre a outle C https://www.myopenmath.com/assess2/?cid=214054&aid=15138198#/skip/8 A A group of kinesiology researchers were...

-

A researcher wanted to find out if there was difference between older movie goers and younger movie goers with respect to their estimates of a successful actors income. The researcher first...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

The pilot of a small boat charts a course such that the boat will always be equidistant from an upcoming rock and the shoreline. Describe the path of the boat. If the rock is 2 miles offshore, write...

-

An equilateral triangle has a point charge + q at each of the three vertices (A, B, C). Another point charge Q is placed at D, the midpoint of the side BC. Solve for Q if the total electric force on...

-

Milletin, egemenlik hakkn kimseyi arac yapmadan bizzat kulland ynetim ekli hangisidir?

-

Lola Stroud invests \($30,000.00\) in a partnership. Her partner, Juan Santo, invests \($50,000.00\). Miss Stroud has 10 years' experience in a similar business; Mr. Santo has no experience. Miss...

-

Formetal Engineering submitted to Presto a sample and specifications for precut polyurethane pads to be used in making air-conditioning units. Formetal paid for the goods as soon as they were...

-

If in performing data analytic procedures over payroll, you seek to obtain pay rate information. What would be the best source for this information? Question options: 1) employees' personnel files 2)...

-

Launched in 1937, Krispy Kreme Doughnuts is a branded specialty retailer of premium doughnuts. Its Original Glazed doughnut is the firm's most recognizable product. However, Krispy Kreme's commitment...

-

Describe the transformations on the logarithmic function g ( x ) = 2 1 l o g [ 7 1 ( x 2 ) ] + 9 Write the equation of a logarithmic function that has been vertically stretched by 4, reflected in the...

-

Elaborate how is the compensation of expatriate employees be more complicated and different than of domestic employees. How can we prepare expatriates and their families for new overseas assignment?...

-

How would you explain to your staff and/or coworkers the value and benefit of understand affective empathy and cognitive empathy, why that is valuable and how it will help in your...

-

Could you elaborate on the concept of transactional leadership, delineating its reliance on contingent rewards and corrective measures to motivate and manage followership within hierarchical...

-

A company operates a job costing system. Job number 6789 will require $345 of direct materials and $210 of direct labour, which is paid $14 per hour. Production overheads are absorbed at the rate of...

-

how can Sergeants Major in the army plan and implement a staff ride to assess and address performance gaps, and develop the workforce within their organization? ensure we address how the preliminary...

-

b) Given the IR spectrum of 2-methylcyclohexan-1-one, indicate (using the appropriate symbol) the bond vibrations occurring at 2965, 1712, and 1376 cm-1 as well as the specific groups they are...

-

Halley's comet travels in an ellipti- cal orbit with a = 17.95 and b = 4.44 and passes by Earth roughly every 76 years. Note that each unit represents one astronomical unit, or 93 million miles. The...

-

Today is September 25, 2008. Table 15.4 in Chapter 15 contains the STRIPS data today. According to the Vasicek model, is there any trading opportunity? Fit the Vasicek model to the data, find pricing...

-

Today is November 3, 2008, and the 3-month LIBOR and (interpolated) swap rates are as in Table 19.4. (a) Obtain the LIBOR yield curve from the swap rates.7 (b) Let be the historical volatility of...

-

Equation 15.28 reports the pricing formula for the Vasicek zero coupon bond (with $1 principal). Check that it satisfies the fundamental pricing equation (Equation 15.24). That is, take the partial...

-

Indicate whether each of the following costs related to inventory, a through I, would be considered (1) a purchasing cost, (2) an ordering cost, (3) a carrying cost, or (4) a cost of not carrying...

-

New automobiles are often equipped with artificial intelligence capabilities that support the driver up to the point of allowing fully autonomous operations. The inspection process of these vehicles...

-

Part One: Backflush Costing Urban Fit Inc. uses backflush costing to account for production costs of its clothing. During June, the company produced 45,000 units and sold 40,000 units. The standard...

Study smarter with the SolutionInn App