Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

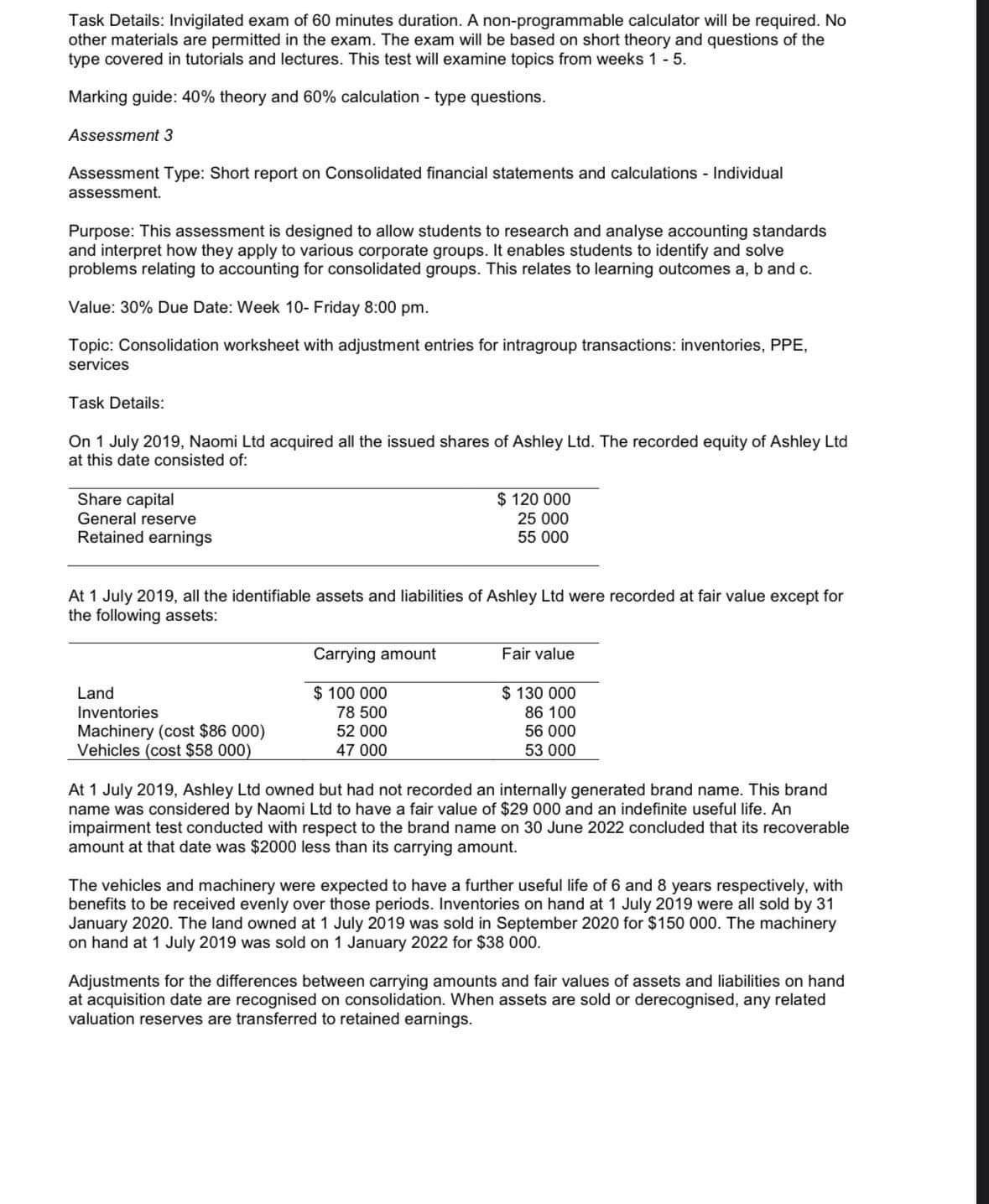

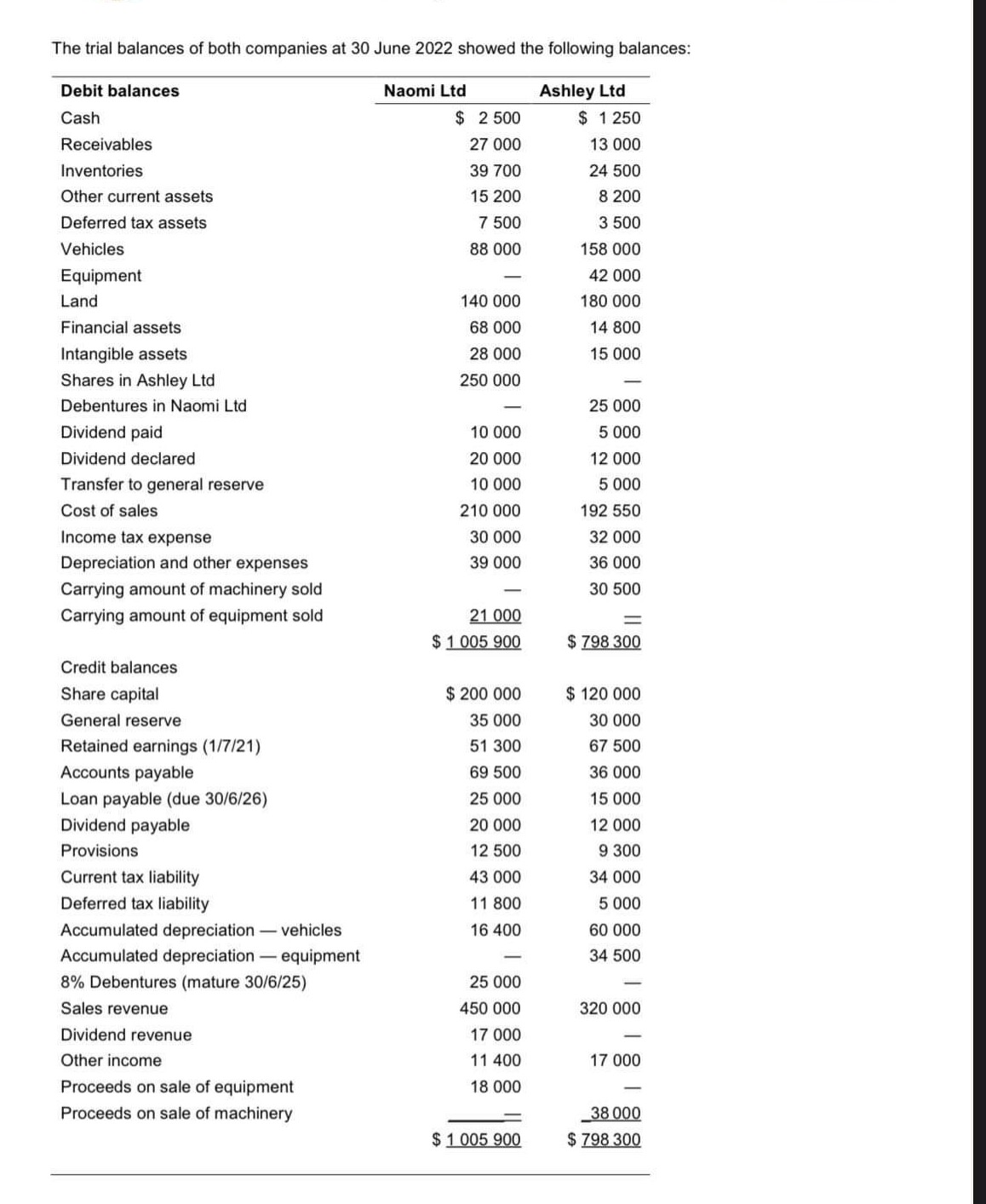

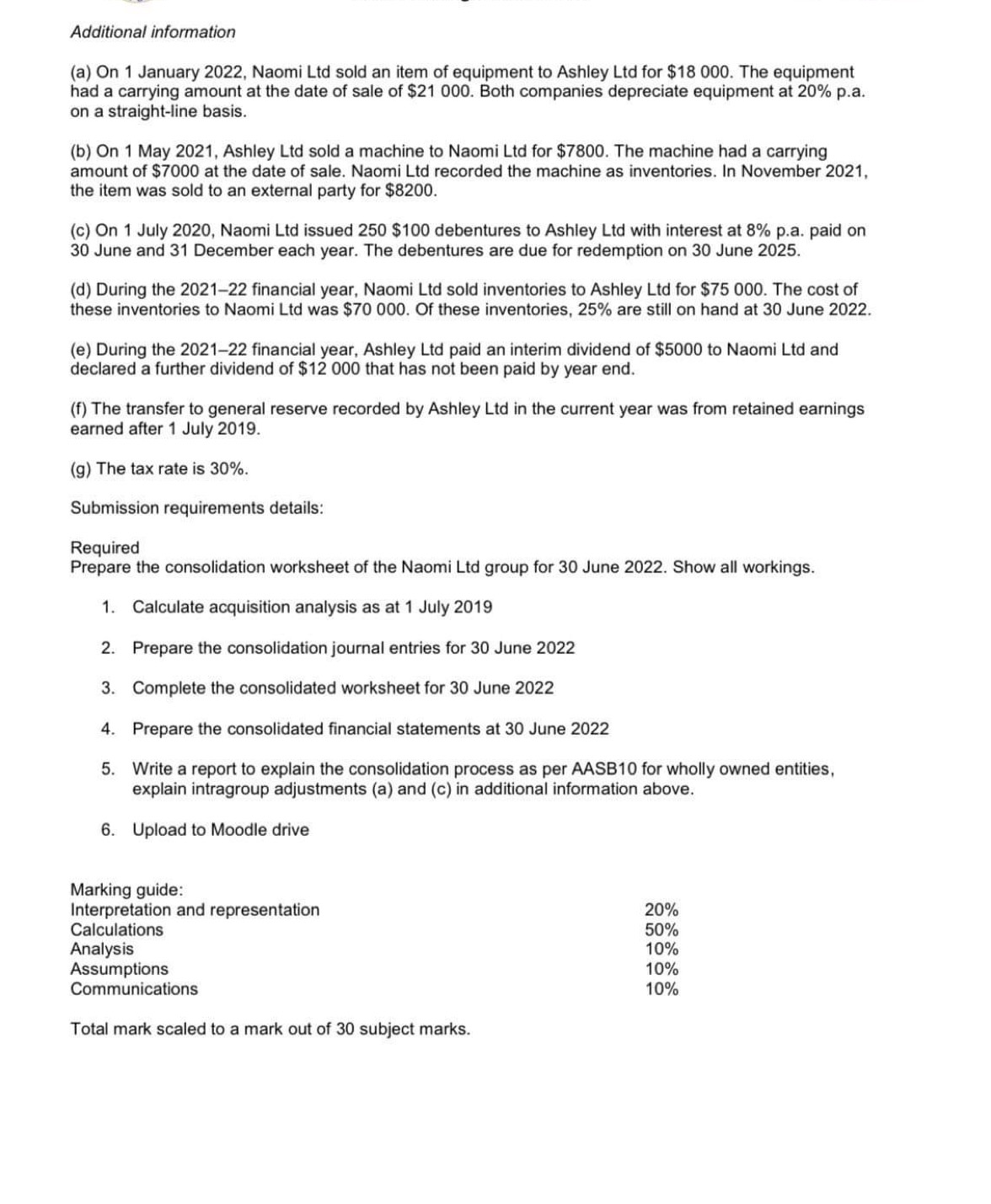

Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other materials are permitted in the exam. The exam will be based on short theory and questions of the type covered in tutorials and lectures. This test will examine topics from weeks 1 - 5. Marking guide: 40% theory and 60% calculation - type questions. Assessment 3 Assessment Type: Short report on Consolidated financial statements and calculations - Individual assessment. Purpose: This assessment is designed to allow students to research and analyse accounting standards and interpret how they apply to various corporate groups. It enables students to identify and solve problems relating to accounting for consolidated groups. This relates to learning outcomes a, b and c. Value: 30% Due Date: Week 10- Friday 8:00 pm. Topic: Consolidation worksheet with adjustment entries for intragroup transactions: inventories, PPE, services Task Details: On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve Retained earnings $ 120 000 25 000 55 000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land Inventories $ 100 000 $ 130 000 78 500 86 100 Machinery (cost $86 000) 52 000 Vehicles (cost $58 000) 47 000 56 000 53 000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Cash Receivables Inventories Other current assets Deferred tax assets Vehicles Equipment Naomi Ltd $ 2500 Ashley Ltd $ 1 250 27 000 13 000 39 700 24 500 15 200 8 200 7 500 3 500 88 000 158 000 42 000 Land 140 000 180 000 Financial assets 68 000 14 800 Intangible assets 28 000 15 000 Shares in Ashley Ltd 250 000 Debentures in Naomi Ltd 25 000 Dividend paid 10 000 5 000 Dividend declared 20 000 12 000 Transfer to general reserve 10 000 5 000 Cost of sales 210 000 192 550 Income tax expense 30 000 32 000 Depreciation and other expenses 39 000 36 000 Carrying amount of machinery sold Carrying amount of equipment sold Credit balances 30 500 21 000 = $ 1 005 900 $ 798 300 Share capital $ 200 000 $ 120 000 General reserve 35 000 30 000 Retained earnings (1/7/21) 51 300 67 500 Accounts payable 69 500 36 000 Loan payable (due 30/6/26) 25 000 15 000 Dividend payable 20 000 12 000 Provisions 12 500 9 300 Current tax liability 43 000 34 000 Deferred tax liability 11 800 5 000 Accumulated depreciation-vehicles 16 400 60 000 Accumulated depreciation-equipment - 34 500 8% Debentures (mature 30/6/25) 25 000 Sales revenue 450 000 320 000 Dividend revenue 17 000 Other income 11 400 17 000 Proceeds on sale of equipment 18 000 Proceeds on sale of machinery 38 000 $ 1.005 900 $798 300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. 6. Upload to Moodle drive Marking guide: Interpretation and representation Calculations Analysis Assumptions Communications Total mark scaled to a mark out of 30 subject marks. 20% 50% 10% 10% 10% Task Details: Invigilated exam of 60 minutes duration. A non-programmable calculator will be required. No other materials are permitted in the exam. The exam will be based on short theory and questions of the type covered in tutorials and lectures. This test will examine topics from weeks 1 - 5. Marking guide: 40% theory and 60% calculation - type questions. Assessment 3 Assessment Type: Short report on Consolidated financial statements and calculations - Individual assessment. Purpose: This assessment is designed to allow students to research and analyse accounting standards and interpret how they apply to various corporate groups. It enables students to identify and solve problems relating to accounting for consolidated groups. This relates to learning outcomes a, b and c. Value: 30% Due Date: Week 10- Friday 8:00 pm. Topic: Consolidation worksheet with adjustment entries for intragroup transactions: inventories, PPE, services Task Details: On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve Retained earnings $ 120 000 25 000 55 000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land Inventories $ 100 000 $ 130 000 78 500 86 100 Machinery (cost $86 000) 52 000 Vehicles (cost $58 000) 47 000 56 000 53 000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Cash Receivables Inventories Other current assets Deferred tax assets Vehicles Equipment Naomi Ltd $ 2500 Ashley Ltd $ 1 250 27 000 13 000 39 700 24 500 15 200 8 200 7 500 3 500 88 000 158 000 42 000 Land 140 000 180 000 Financial assets 68 000 14 800 Intangible assets 28 000 15 000 Shares in Ashley Ltd 250 000 Debentures in Naomi Ltd 25 000 Dividend paid 10 000 5 000 Dividend declared 20 000 12 000 Transfer to general reserve 10 000 5 000 Cost of sales 210 000 192 550 Income tax expense 30 000 32 000 Depreciation and other expenses 39 000 36 000 Carrying amount of machinery sold Carrying amount of equipment sold Credit balances 30 500 21 000 = $ 1 005 900 $ 798 300 Share capital $ 200 000 $ 120 000 General reserve 35 000 30 000 Retained earnings (1/7/21) 51 300 67 500 Accounts payable 69 500 36 000 Loan payable (due 30/6/26) 25 000 15 000 Dividend payable 20 000 12 000 Provisions 12 500 9 300 Current tax liability 43 000 34 000 Deferred tax liability 11 800 5 000 Accumulated depreciation-vehicles 16 400 60 000 Accumulated depreciation-equipment - 34 500 8% Debentures (mature 30/6/25) 25 000 Sales revenue 450 000 320 000 Dividend revenue 17 000 Other income 11 400 17 000 Proceeds on sale of equipment 18 000 Proceeds on sale of machinery 38 000 $ 1.005 900 $798 300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. 6. Upload to Moodle drive Marking guide: Interpretation and representation Calculations Analysis Assumptions Communications Total mark scaled to a mark out of 30 subject marks. 20% 50% 10% 10% 10%

Expert Answer:

Answer rating: 100% (QA)

Assessment Type Short report on Consolidated financial statements and calculations Individual assessment Value 30 Due Date Week 10 Friday 800 pm Topic ... View the full answer

Related Book For

Applied Regression Analysis and Other Multivariable Methods

ISBN: 978-1285051086

5th edition

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

Posted Date:

Students also viewed these accounting questions

-

Question 2 (30 Marks) A space-satellite structure is made of a composite laminate tailored for the following thermal expansion properties: = ax*0.1 x 10-6 m/m/C ; = +10.5 x 10-6 m/m/C A certain...

-

You are the network administration for the small network in Figure 2. It consists of your headquarters location with a LAN with 60 hosts, remote office R1 with 10 hosts, and remote office R2 with 30...

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

Discuss the impact of commissions in organizations growth?

-

The capital retention approach determines the amount of life insurance needed by first determining what level of annual income the insured wishes to provide for the family.

-

The Graham Telephone Company may invest in new switching equipment. There are three possible outcomes, having net present worth of $6570, $8590, and $9730. The probability of each outcome is 0.3,...

-

In a manufacturer's balance sheet, three inventories may be reported: (1) raw materials, (2) work in process, and (3) finished goods. Indicate in what sequence these inventories generally appear on a...

-

Assume Magnificent Modems, Inc. (MMI) is a division of Gilmore Business Products (GBP). GBP uses ROI as the primary measure of managerial performance. GBP has a desired return on investment (ROI) of...

-

As corporate manager for acquisitions, your group is assessing a project that is expected to produce cash flows of $750 at the end of year 1, $1,000 at the end of year 2, $850 at the end of year 3,...

-

You are the executive assistant to the director of sales at B-Trendz, Inc., a trendy retail store that has locations in only ten states. The company is considering branching into the online retail...

-

You are considering the purchase of real estate that will provide perpetual income that should average $66,000 per year. How much will you pay for the property if you believe its market risk is the...

-

With regards to primary care services, what rolde does Walmart or retail clinics propose in the spectrum on the United States healthcare market?

-

A single ratio can be misleading. For example, Walmart has more cash than they need, and yet its current ratio is less than one. You need to know more. Here is a video that makes that point as well.

-

Does the Walmart have an ethics program? If so, what processes are in place to encourage ethical behavior from supervisors and their direct reports? If not, what would your recommendation be to them...

-

If Walmart decides to enter European market, how this decision triggers various decisions at all decision levels of supply chain (strategic level, tactical level and operational level)? Explain and...

-

Olympic Games were important because Jim Thorpe was disqualified for receiving a small amount of money for playing summer baseball. Thus, the controversy between pure amateurism and professionalism...

-

i need requirements 2-5 asap Johnson Associates, a law firm, hires A storney Dina Martin at an annual salary of \( \$ 175,000 \). The law firm expects hor to spend 2,500 hours a year performing legal...

-

Record the following selected transactions for March in a two-column journal, identifying each entry by letter: (a) Received $10,000 from Shirley Knowles, owner. (b) Purchased equipment for $35,000,...

-

A five-year follow-up study was carried out to assess the relationship of diet and weight to the incidence of stomach cancer in 40- to 50-year-old males in a certain metropolitan area. Let K- denote...

-

A random sample of 52 persons attending a certain diet clinic was found to have lost (over a three-week period) an average of 30 pounds, with a sample standard deviation of 11. For these data, a 99%...

-

For the data from Problem 2 in this chapter, address the following questions, using the information provided in the accompanying SAS output. a. State the regression model that incorporates the...

-

A retailer purchases a can of soup for 24 cents and sells it for 36 cents. Calculate the markup as a percentage of cost and as a percentage of selling price.

-

The characteristics of services affect the development of marketing mixes for services. Choose a specific service and explain how each marketing mix element could be affected by these service...

-

Identify a familiar product that recently was modified, categorize the modification (quality, functional, or aesthetic), and describe how you would have modified it differently.

Study smarter with the SolutionInn App