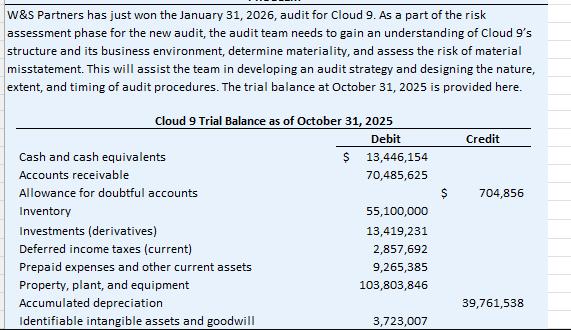

W&S Partners has just won the January 31, 2026, audit for Cloud 9. As a part...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

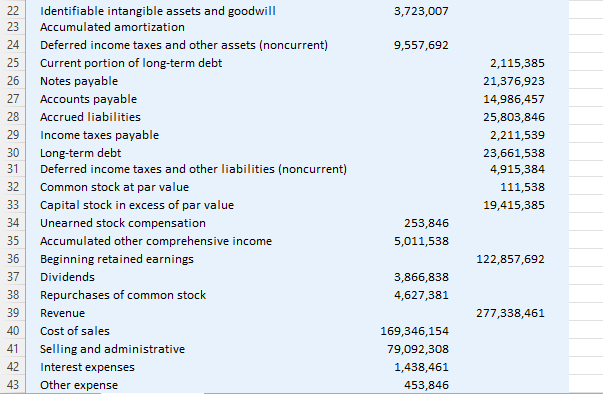

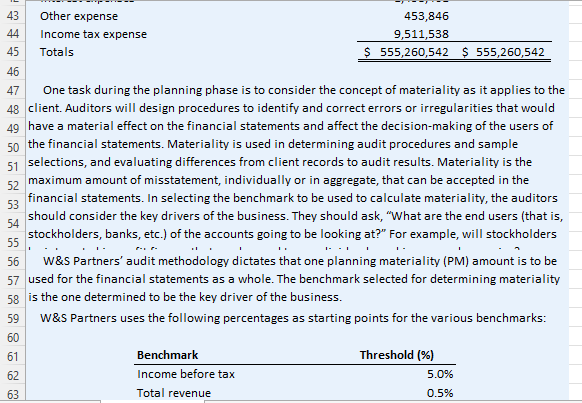

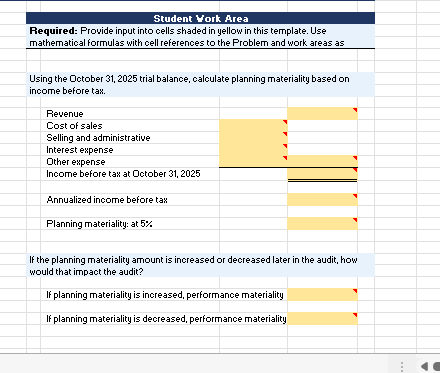

W&S Partners has just won the January 31, 2026, audit for Cloud 9. As a part of the risk assessment phase for the new audit, the audit team needs to gain an understanding of Cloud 9's structure and its business environment, determine materiality, and assess the risk of material misstatement. This will assist the team in developing an audit strategy and designing the nature, extent, and timing of audit procedures. The trial balance at October 31, 2025 is provided here. Cloud 9 Trial Balance as of October 31, 2025 Debit Cash and cash equivalents Accounts receivable Allowance for doubtful accounts Inventory Investments (derivatives) Deferred income taxes (current) Prepaid expenses and other current assets Property, plant, and equipment Accumulated depreciation Identifiable intangible assets and goodwill $ 13,446,154 70,485,625 55,100,000 13,419,231 2,857,692 9,265,385 103,803,846 3,723,007 Credit 704,856 39,761,538 22 Identifiable intangible assets and goodwill 23 Accumulated amortization 24 25 26 27 28 29 30 31 Income taxes payable Long-term debt Deferred income taxes and other liabilities (noncurrent) 32 Common stock at par value 33 Capital stock in excess of par value 34 Unearned stock compensation 35 Accumulated other comprehensive income Beginning retained earnings 36 37 Dividends 38 Repurchases of common stock Deferred income taxes and other assets (noncurrent) Current portion of long-term debt Notes payable Accounts payable Accrued liabilities 39 40 41 42 43 Revenue Cost of sales Selling and administrative Interest expenses Other expense 3,723,007 9,557,692 253,846 5,011,538 3,866,838 4,627,381 169,346,154 79,092,308 1,438,461 453,846 2,115,385 21,376,923 14,986,457 25,803,846 2,211,539 23,661,538 4,915,384 111,538 19,415,385 122,857,692 277,338,461 43 Other expense 44 Income tax expense 45 Totals 46 47 One task during the planning phase is to consider the concept of materiality as it applies to the 48 client. Auditors will design procedures to identify and correct errors or irregularities that would 49 have a material effect on the financial statements and affect the decision-making of the users of 50 the financial statements. Materiality is used in determining audit procedures and sample 51 selections, and evaluating differences from client records to audit results. Materiality is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the benchmark to be used to calculate materiality, the auditors should consider the key drivers of the business. They should ask, "What are the end users (that is, stockholders, banks, etc.) of the accounts going to be looking at?" For example, will stockholders 52 53 54 55 77 I 56 W&S Partners' audit methodology dictates that one planning materiality (PM) amount is to be 57 used for the financial statements as a whole. The benchmark selected for determining materiality 58 is the one determined to be the key driver of the business. 59 W&S Partners uses the following percentages as starting points for the various benchmarks: 60 61 62 63 453,846 9,511,538 $ 555,260,542 $ 555,260,542 · Benchmark Income before tax Total revenue Threshold (%) 5.0% 0.5% 出16234 65 66 印 68 69 70 1 2 73 74 60 67 Benchmark Income before tax Total revenue 75 7 78 79 80 Gross profit Total assets Equity Threshold (%) 74 The knowledge of or high risk of fraud. 5.0% 0.5% 2.0% 0.5% 1.0% These starting points can be increased or decreased by taking into account qualitative client 70. The nature of the client's business and industry (for example, rapidly changing, either 71 through growth or downsizing, or an unstable environment). 72 Whether the client is a public company (or a subsidiary of a public company) subject to regulations. 75 Typically, income before tax is used; however, it cannot be used if reporting a loss for the year or 76 if profitability is not consistent. 77 When calculating PM based on interim figures, it may be necessary to annualize the results. 78 This allows the auditors to plan the audit properly based on an approximate projected year-end balance. Then, at year-end, the figure is adjusted, if necessary, to reflect the actual results. Student Vork Area Required: Provide input into cells shaded in yellow in this template. Use mathematical formulas with cell references to the Problem and work areas as Using the October 31, 2025 trial balance, calculate planning materiality based on income before tax. Revenue Cost of sales Selling and administrative Interest expense Other expense Income before tax at October 31, 2025 Annualized income before tax Planning materiality: at 5% If the planning materiality amount is increased or decreased later in the audit, how would that impact the audit? If planning materiality is increased, performance materiality If planning materiality is decreased, performance materiality W&S Partners has just won the January 31, 2026, audit for Cloud 9. As a part of the risk assessment phase for the new audit, the audit team needs to gain an understanding of Cloud 9's structure and its business environment, determine materiality, and assess the risk of material misstatement. This will assist the team in developing an audit strategy and designing the nature, extent, and timing of audit procedures. The trial balance at October 31, 2025 is provided here. Cloud 9 Trial Balance as of October 31, 2025 Debit Cash and cash equivalents Accounts receivable Allowance for doubtful accounts Inventory Investments (derivatives) Deferred income taxes (current) Prepaid expenses and other current assets Property, plant, and equipment Accumulated depreciation Identifiable intangible assets and goodwill $ 13,446,154 70,485,625 55,100,000 13,419,231 2,857,692 9,265,385 103,803,846 3,723,007 Credit 704,856 39,761,538 22 Identifiable intangible assets and goodwill 23 Accumulated amortization 24 25 26 27 28 29 30 31 Income taxes payable Long-term debt Deferred income taxes and other liabilities (noncurrent) 32 Common stock at par value 33 Capital stock in excess of par value 34 Unearned stock compensation 35 Accumulated other comprehensive income Beginning retained earnings 36 37 Dividends 38 Repurchases of common stock Deferred income taxes and other assets (noncurrent) Current portion of long-term debt Notes payable Accounts payable Accrued liabilities 39 40 41 42 43 Revenue Cost of sales Selling and administrative Interest expenses Other expense 3,723,007 9,557,692 253,846 5,011,538 3,866,838 4,627,381 169,346,154 79,092,308 1,438,461 453,846 2,115,385 21,376,923 14,986,457 25,803,846 2,211,539 23,661,538 4,915,384 111,538 19,415,385 122,857,692 277,338,461 43 Other expense 44 Income tax expense 45 Totals 46 47 One task during the planning phase is to consider the concept of materiality as it applies to the 48 client. Auditors will design procedures to identify and correct errors or irregularities that would 49 have a material effect on the financial statements and affect the decision-making of the users of 50 the financial statements. Materiality is used in determining audit procedures and sample 51 selections, and evaluating differences from client records to audit results. Materiality is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the benchmark to be used to calculate materiality, the auditors should consider the key drivers of the business. They should ask, "What are the end users (that is, stockholders, banks, etc.) of the accounts going to be looking at?" For example, will stockholders 52 53 54 55 77 I 56 W&S Partners' audit methodology dictates that one planning materiality (PM) amount is to be 57 used for the financial statements as a whole. The benchmark selected for determining materiality 58 is the one determined to be the key driver of the business. 59 W&S Partners uses the following percentages as starting points for the various benchmarks: 60 61 62 63 453,846 9,511,538 $ 555,260,542 $ 555,260,542 · Benchmark Income before tax Total revenue Threshold (%) 5.0% 0.5% 出16234 65 66 印 68 69 70 1 2 73 74 60 67 Benchmark Income before tax Total revenue 75 7 78 79 80 Gross profit Total assets Equity Threshold (%) 74 The knowledge of or high risk of fraud. 5.0% 0.5% 2.0% 0.5% 1.0% These starting points can be increased or decreased by taking into account qualitative client 70. The nature of the client's business and industry (for example, rapidly changing, either 71 through growth or downsizing, or an unstable environment). 72 Whether the client is a public company (or a subsidiary of a public company) subject to regulations. 75 Typically, income before tax is used; however, it cannot be used if reporting a loss for the year or 76 if profitability is not consistent. 77 When calculating PM based on interim figures, it may be necessary to annualize the results. 78 This allows the auditors to plan the audit properly based on an approximate projected year-end balance. Then, at year-end, the figure is adjusted, if necessary, to reflect the actual results. Student Vork Area Required: Provide input into cells shaded in yellow in this template. Use mathematical formulas with cell references to the Problem and work areas as Using the October 31, 2025 trial balance, calculate planning materiality based on income before tax. Revenue Cost of sales Selling and administrative Interest expense Other expense Income before tax at October 31, 2025 Annualized income before tax Planning materiality: at 5% If the planning materiality amount is increased or decreased later in the audit, how would that impact the audit? If planning materiality is increased, performance materiality If planning materiality is decreased, performance materiality

Expert Answer:

Related Book For

Auditing A Practical Approach with Data Analytics

ISBN: 978-1119401742

1st edition

Authors: Raymond N. Johnson, Laura Davis Wiley, Robyn Moroney, Fiona Campbell, Jane Hamilton

Posted Date:

Students also viewed these accounting questions

-

In many cases, organizations use teams as a part of their high-performance work systems. Could such systems be useful in organizations that do not use teams? What special concerns might you have to...

-

As a part of their customer-service program, United Airlines randomly selected 10 passengers from todays 9 a.m. ChicagoTampa flight. Each sampled passenger is to be inter-viewed in depth regarding...

-

As a part of an employment interview, you are given the partial income statement and selected financial ratios shown for Sneaky Pete's, a chain of western stores. Sneaky Pete's is organized into two...

-

Prove that, the area of the traverse is equal to the algebraic sum of the products of the total latitude of each point and algebraic sum of the departures of the lines meeting at that point.

-

Indole reacts with electrophile at C3 rather than at C2. Draw resonance forms of the intermediate cations resulting from reaction at C2 and C3, and explain the observed results.

-

A ray of light reflects from a plane mirror with an angle of incidence of 27. If the mirror is rotated by an angle , through what angle is the reflected ray rotated?

-

Does the income statement of Tastykake in Appendix A indicate the net income earned by its business segments? If so, list them.

-

A newly hired staff accountant prepared the pre-audit income statement of Be Fit Recreation Incorporated for the year ending December 31, 2011. The following information was obtained by Be Fits...

-

6. The determinant of a 2x2 matrix a is ad - bc. C d 3 6 Question: Find the determinant of - -1 For more information on this topic, look in your textbook at section 8.3. You might also want to look...

-

Calculate the molar volume of saturated liquid and the molar volume of saturated vapor by the Redlich/Kwong equation for one of the following and compare results with values found by suitable...

-

Ninabea, Inc. has outstanding 200,000 shares of P2 par common stock and 40,000 shares of no-par 8% preferred stock with a stated value of P5. The preferred stock is cumulative. Dividends have been...

-

In its income statement for the year ended December 31, 2022, Shamrock Inc. reported the following condensed data. Operating expenses $812,000 Interest revenue $ 36,960 Cost of goods sold 1,406,720...

-

Peter is a dual citizen of US and Canada residing in Canada. He is single. In 2 0 1 9 he received $ 2 0 K US Social Security and $ 4 0 K distribution from registered retirement plan in Canada. What...

-

Hamilton Boats issued 306,000 shares of its no-par common stock to Sudoku Motors in exchange for 1,800 four-stroke outboard motors that normally sell in quantity for $3,400 each. By what amount...

-

Sheridan Company had the following select transactions. Apr. 1, 2022 July 1, 2022 Dec. 31, 2022 Apr. 1, 2023 Apr. 1, 2023 Accepted Goodwin Company's 12-month, 16% note in settlement of a $53,400...

-

Question: prepare a master budget for local manufacturing bangladeshi store for the year 2 0 2 4

-

Quantitative Problem: At the end of last year, Edwin Inc. reported the following income statement (in millions of dollars): Sales Operating costs (excluding depreciation) EBITDA Depreciation...

-

Refer to the table to answer the following questions. Year Nominal GDP (in billions) Total Federal Spending (in billions) Real GDP (in billions) Real Federal Spending (in billions) 2000 9,817 578...

-

Identify and briefly describe the five steps of performing ADA and place them in the proper order.

-

The AICPA rule on general standards identifies four aspects of professional behavior. Identify each of the four aspects and develop an example illustrating the violation of each aspect.

-

Gather information: Considering both industry and entity factors, what are the major inherent risks in the MSI audit? Mobile Security, Inc. (MSI) has been an audit client of Leo & Lee LLP for the...

-

Of the following four transactions, which carries the most risk: purchase of a call option; sale of a call option; purchase of a put option; sale of a put option; Why?

-

If you hold stock options on the shares in your company, would you be pleased to see the company paying out large dividends? Why?

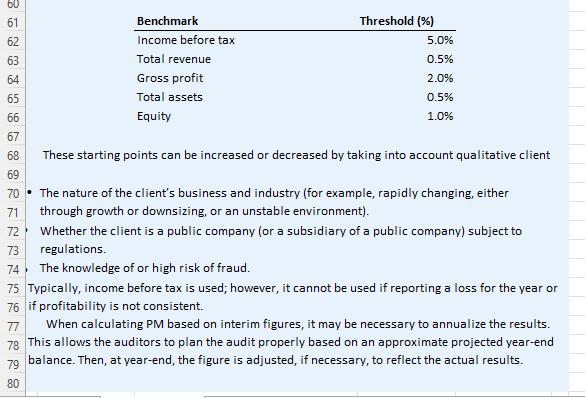

-

Why are options particularly well suited to arbitrage strategies? And speculation?

Study smarter with the SolutionInn App