Consider a derivative that pays off S n T at time T where S T is the

Question:

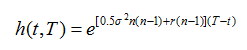

Consider a derivative that pays off SnT at time T where ST is the stock price at that time. When the stock pays no dividends and its price follows geometric Brownian motion, it can be shown that its price at time t (t ≤ T) has the form h(t, T) Sn where S is the stock price at time and is a function only of t and T.

(a) By substituting into the Black–Scholes–Merton partial differential equation derive an ordinary differential equation satisfied by h(t, T). (b) What is the boundary condition for the differential equation for h(t, T)? (c) Show that

where r is the risk-free interest rate and σ is the stock price volatility.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

If then and where Substituting into the BlackScholesMerton differential equation we obtain The de...View the full answer

Answered By

Stacy kosgei

I offer quality, original and timely services; Highly credible and void of plagiarism. Your success is my pleasure.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: