OHanlon Company is an automotive component supplier. OHanlon has been approached by Chryslers Ohio plant to consider

Question:

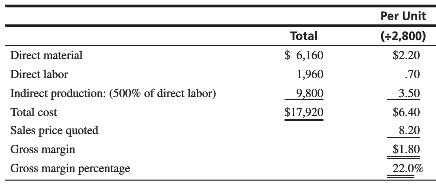

O’Hanlon Company is an automotive component supplier. O’Hanlon has been approached by Chrysler’s Ohio plant to consider expanding its production of part 24Z2 to a total annual quantity of 2,800 units. This part is a low-volume, complex product with a high gross margin that is based on a proposed (quoted) unit sales price of $8.20. O’Hanlon uses a traditional costing system that allocates indirect manufacturing costs based on direct-labor costs. The rate currently used to allocate indirect manufacturing costs is 500% of direct-labor cost. This rate is based on the $4,121,000 annual factory overhead cost divided by $824,200 annual direct-labor cost. To produce 2,800 units of 24Z2 requires $6,160 of direct materials and $1,960 of direct labor. The unit cost and gross margin percentage for part 24Z2 based on the traditional cost system are computed as follows:

The management of O’Hanlon decided to examine the effectiveness of their traditional costing system versus an activity-based costing system. The following data have been collected by a team consisting of accounting and engineering analysts:

Activity Center … Factory Overhead Costs (Annual)

Quality ………………………………… $ 880,000

Production scheduling …………………… 72,000

Setup ……………………………………. 880,000

Shipping ………………………………… 384,000

Shipping administration ………………… 105,000

Production …………………………….. 1,800,000

Total indirect production cost ……….. $4,121,000

Activity Center: Cost Drivers …….. Annual Cost-Driver Quantity

Quality: Number of pieces scrapped ……………….. 16,000

Production scheduling and set up: Number of setups … 800

Shipping: Number of containers shipped …………. 64,000

Shipping administration: Number of shipments …… 1,500

Production: Number of machine hours …………… 12,000

The accounting and engineering team has performed activity analysis and provides the following estimates for the total quantity of cost drivers to be used to produce 2,800 units of part 24Z2:

Cost Driver … Cost-Driver Consumption

Pieces scrapped …………….. 150

Setups ……………………… 5

Containers shipped ……….. 12

Shipments ………………….. 7

Machine hours ……………. 16

1. Prepare a schedule calculating the unit cost and gross margin of part 24Z2 using the activity-based costing approach. Use the cost drivers given as cost-allocation bases.

2. Based on the ABC results, which course of action would you recommend regarding the proposal by Chrysler? List the benefits and costs associated with implementing an ABC system at O’Hanlon.

Step by Step Answer:

1 2 Assuming that the results of the activity analysis are accurate product 24Z2 is much more costly than OHanlons existing costing system estimates T...View the full answer

Introduction to Management Accounting

ISBN: 978-0133058789

16th edition

Authors: Charles Horngren, Gary Sundem, Jeff Schatzberg, Dave Burgsta