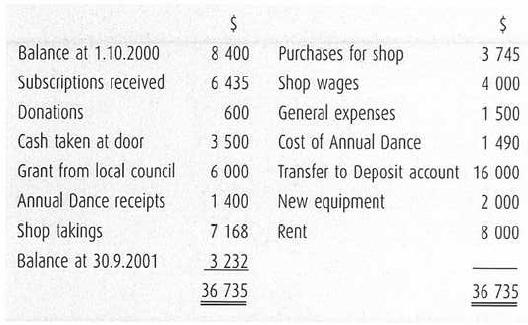

The Abracamagic Club's Bank Current account for the year ended 30 September 2001 was as follows. In

Question:

The Abracamagic Club's Bank Current account for the year ended 30 September 2001 was as follows.

In order to increase funds the club has a shop which sells magic tricks. In addition to an annual membership subscription, members pay $1 each time they visit the club. This is referred to as 'Cash taken at door'.

The annual membership subscription was $40 until 30 September 2001 when it was raised to $45.

There were 150 members at 1 October 2000. At that date 15 of them had not paid their subscriptions for the year ended 30 September 2000, and 12 had already paid their subscriptions for the year ended 30 September 2001.

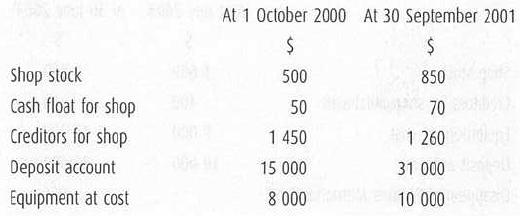

By 30 September 2001, all members had paid their due subscriptions, and some had paid in advance for the year ending 30 September 2002, but the Treasurer had not yet calculated how many. Other balances were as follows.

The equipment at 1 October 2000 had been depreciated by $1600 per annum for five years. The new equipment is to be depreciated at the same annual percentage rate.

The local council's grant was for $10 000 and the remainder of this has yet to be received. This will be treated as revenue income in the final accounts. Interest of $800 is due on the deposit account for the year ended 30 September 2001. At 30 September 2001, general expenses of $65 were due and unpaid.

Required

(a) Calculate the Accumulated fund at 1 October 2000.

(b) Prepare the Club Shop Trading Account for the year ended 30 September 2001.

(c) Prepare the Club Subscriptions account for the year ended 30 September 2001.

(d) Prepare the Club Income and Expenditure Account for the year ended 30 September 2001.

Step by Step Answer:

a Calculate the Accumulated Fund at 1 October 2000 The Accumulated Fund at the start of the year is ...View the full answer