In January 2024, the management of Newlands Ltd decided to expand the business. On 1 July 2024,

Question:

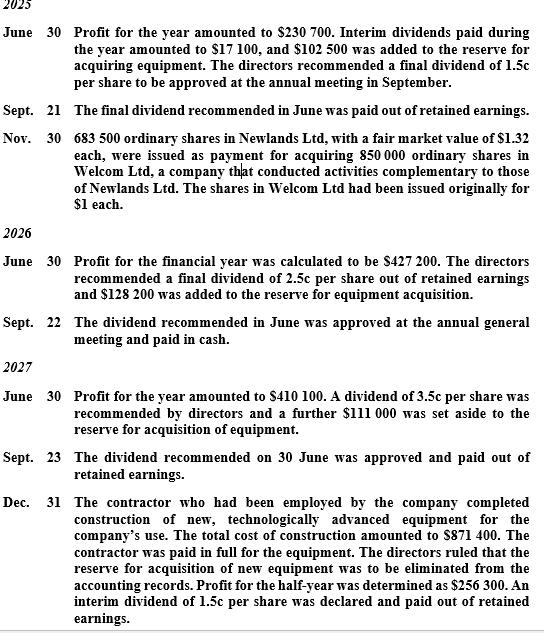

In January 2024, the management of Newlands Ltd decided to expand the business. On 1 July 2024, the company had $768 900 in retained earnings, and another reserve totalling $512 600 had been set aside for the acquisition of equipment out of retained earnings. Share capital consisted of 2 390 000 shares issued for $1 each. The following events occurred in relation to the equity accounts of Newlands Ltd over the next few years.

Required

(a) Prepare journal entries to record all transactions and events across the three year period.

(b) Show the equity section of the balance sheet of Newlands Ltd at 31 December 2027.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Mario Alvarez

I teach Statistics and Probability for students of my university ( Univerisity Centroamerican Jose Simeon Canas) in my free time and when students ask for me, I prepare and teach students that are in courses of Statistics and Probability. Also I teach students of the University Francisco Gavidia and Universidad of El Salvador that need help in some topics about Statistics, Probability, Math, Calculus. I love teaching Statistics and Probability! Why me?

** I have experience in Statistics and Probability topics for middle school, high school and university.

** I always want to share my knowledge with my students and have a great relationship with them.

** I have experience working with students online.

** I am very patient with my students and highly committed with them

1+ Reviews

10+ Question Solved

Related Book For

Accounting

ISBN: 9780730382737

11th Edition

Authors: John Hoggett, John Medlin, Keryn Chalmers, Claire Beattie

Question Posted: