Amber Textiles Limited is a small textile processing company based in Burnley in Lancashire. It is one

Question:

Amber Textiles Limited is a small textile processing company based in Burnley in Lancashire. It is one of the few remaining such companies in the United Kingdom but it is also struggling to survive as a result of intense competition from the Far East.

The board of directors has been well aware for some time that if the company is to survive, it must retain its customer base by being extremely competitive. There is little scope to increase selling prices and so costs have to be controlled extremely tightly.

The board has done everything possible to control the company’s costs. For example, it recently introduced an ‘information for management’ (IFM) system. The system involves using budgets for control purposes but it also produces standard costs for each of the company’s main product lines. A firm of management consultants installed the system with the assistance of the company’s small accounting staff.

The new IFM system seemed to involve an awful lot of paperwork and Ted Finch, the managing director, was struggling to cope with the sheer volume of reports that mysteriously appeared on his desk almost every day. By profession, Ted was a textile engineer.

He had little training in numerical analysis and none related to accounting.

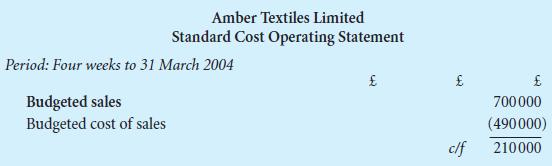

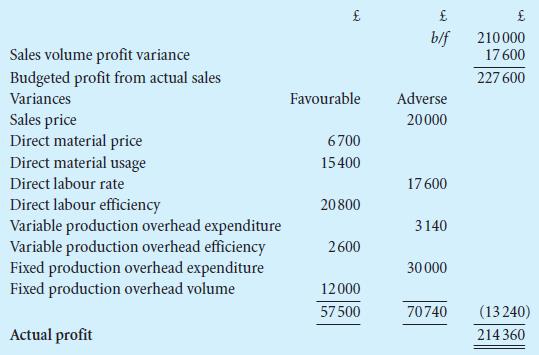

One morning, shortly after the new system was up and running he found the following statement on his desk.

Ted studied the statement carefully.What was it? How had it been produced? What did it mean? What was he supposed to do with it?

He was still somewhat puzzled after studying it for some time so he decided to telephone the management consultants responsible for installing the IFM system. They referred him to a manual that they had prepared, a copy of which lay untouched on Ted’s bookshelf. Sure enough, the manual contained an example and an explanation of a ‘standard costing operating statement’ and what management should do to action it.

After consulting the relevant section, Ted felt a little more confident about what the statement meant and what he was supposed to do with it. Nevertheless, he thought that it might be useful to take some advice. So he contacted his chief accountant and asked him to prepare a written report dealing with the specific standard cost operating statement for the four weeks to 31 March 2004. He stressed that he wanted to know precisely what action management should take (if any) to deal with its contents.

Required:

1 Prepare the section of an ‘Information for Management’ manual dealing with standard cost operating statements. The section should include an outline of the nature and purpose of such a statement, an explanation of its contents, and the action management should take on receiving it.

2 With regard to the specific standard cost operating statement for the four weeks to 31 March 2004, prepare a report explaining what the data means, what interrelationship there may be among the variances, and what specific action Ted Finch might expect his line managers to take in dealing with it.

3 Outline what additional information might be useful to include in a standard cost operating statement.

Step by Step Answer: