On 1 January 20x1, P Co acquired 70% of S Co by issuing 1,000,000 new shares to

Question:

On 1 January 20x1, P Co acquired 70% of S Co by issuing 1,000,000 new shares to the owners of S Co. The fair value of consideration paid by P Co to acquire S Co was $2,100,000. The fair value of non-controlling interests at acquisition date was $900,000. On 1 January 20x2, P Co acquired a 40% ownership interest in A Co by making a cash payout of $200,000 to the owners of A Co.

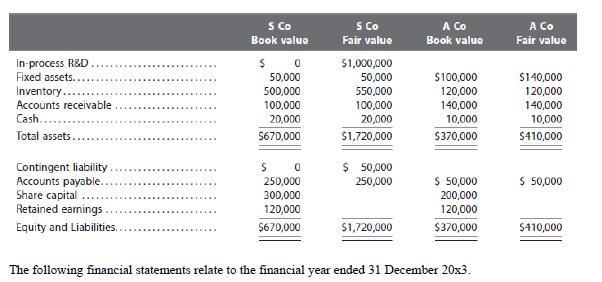

The following information relates to statements of financial position at date of acquisition:

Additional information

(a) Impairment of in-process research and development of $100,000 was expensed off in the consolidated financial statements of P Co in 20x2.

(b) Undervalued inventory as at 1 January 20x1 was sold in 20x1.

(c) The contingent liability of $50,000 in respect of legal claims was paid off by S in 20x3, and recognized as an expense by S Co in 20x3.

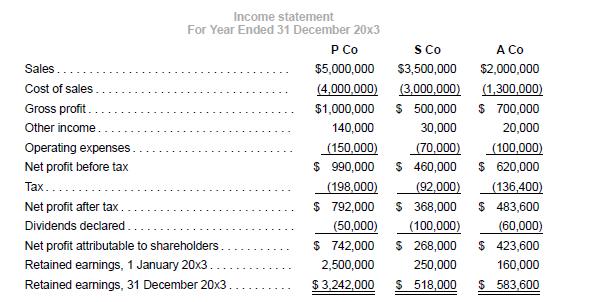

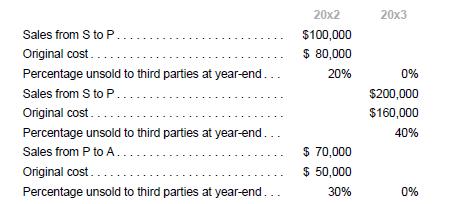

(d) The following sales of inventory were made during 20x2 and 20x3.

(e) Undervalued fixed assets of A Co had a useful life of five years from date of acquisition.

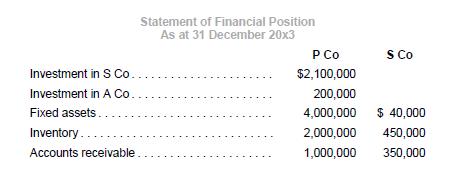

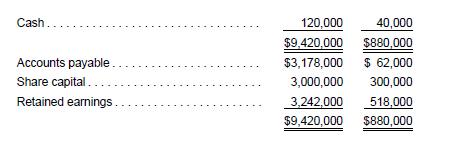

(f) There is no change in the share capital of S Co and A Co from acquisition date.

(g) Assume a tax rate of 20%. Recognize tax on fair value adjustments

Required

1. Prepare the consolidation and equity accounting entries for the year ended 31 December 20x3.

2. Prepare the consolidation worksheet for the year ended 31 December 20x3 to show the consolidated financial statements prepared in accordance with IAS 27 and IAS 28.

3. Perform an analytical check on the balance of non-controlling interests and investment of associate as at 31 December 20x3.

Step by Step Answer:

Advanced Financial Accounting An IFRS Standards Approach

ISBN: 9781285428765

4th Edition

Authors: Pearl Tan, Chu Yeong Lim, Ee Wen Kuah