One of the basic methods of audit testing is to select representative samples of transactions and balances

Question:

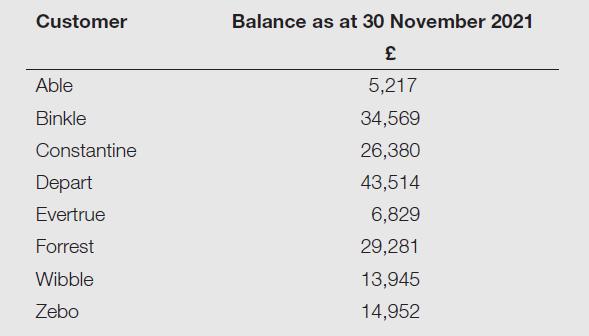

One of the basic methods of audit testing is to select representative samples of transactions and balances for detailed testing, such samples being selected using either statistical or non-statistical methods. Your firm is the external auditor of Polyglot Ltd for the year ended 30 November 2021. Polyglot has sales of £11m and trade receivables were £2.1m as of 30 November 2021. The audit manager has explained that judgement would be used to select receivables which appear to be doubtful and those which would not be selected using monetary unit sampling. The total number of customers to be tested is 50 – this list is simply an extract from the total listing of balances:

Required:

(a) Describe the main factors which influence the size of the sample to be used for audit testing.

(b) Outline three areas where judgement might be exercised when using statistical sampling.

(c) In making the choice between a statistical or non-statistical sampling procedure explain the factors which the auditor must take into account.

(d) Using a Monetary Unit Sampling technique, select the customers from the list of balances above which would be included in a sample of Receivables balances for testing.

Step by Step Answer:

a Factors Influencing Sample Size for Audit Testing Various factors determine the size of the sample for audit testing and auditors take these considerations into account when selecting the proper sam...View the full answer