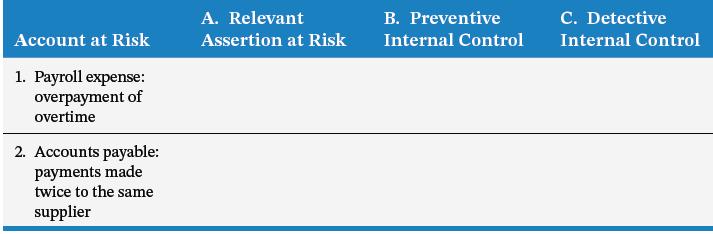

For each of the accounts for Shady Oaks (payroll expense and accounts payable in items 1 and

Question:

For each of the accounts for Shady Oaks (payroll expense and accounts payable in items 1 and 2 above)

identified to be a significant risk:

a. Determine the relevant assertions.

b. Describe a practical preventive internal control that would directly address the risk.

c. Describe a practical detective internal control that Shady Oaks could implement in relation to the risk.

You may wish to present your answer in the form of a table, as follows

Fellowes and Associates Chartered Professional Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. In April 2023, Fellowes and Associates gained a new client, Health Care Holdings Group (HCHG), which owns 100 percent of the following entities:

• Shady Oaks Centre, a private treatment centre • Gardens Nursing Home Ltd., a private nursing home • Total Laser Care Limited, a private clinic that specializes in the laser treatment of skin defects The year end for all HCHG entities is June 30.

You are an audit senior on the Shady Oaks engagement. Your initial review of the business has highlighted the following significant risks. 1. Payroll expense—Shady Oaks employs, in addition to its full-time staff, a significant number of casual nursing, cleaning, and administrative staff. Overtime is often worked on weekends and night shifts due to a shortage of staff. Payment at overtime rates for standard weekend and night shifts has been a common occurrence. 2. Accounts payable—Shady Oaks also has a large number of suppliers for various medical supplies and drugs. Paying the supplier twice for the same purchase has been a continuing problem.

In addition, your business risk assessment procedures indicate there is a risk that payments to suppliers are made prior to goods being received. As part of your evaluation of the potential mitigating internal controls, you note that accounting staff perform the following procedures: 1. A pre-numbered cheque requisition is prepared for all payments. 2. The details on the supplier’s invoice are matched to the appropriate receiving report. 3. The details on the supplier’s invoice and receiving report are matched to an authorized purchase order. 4. The cheque requisition is stapled to the authorized purchase order, receiving report, and supplier’s invoice and forwarded to the appropriate senior staff member for review and authorization. 5. The authorized cheque requisition, together with the supporting documents, is passed to accounts payable for payment.

Step by Step Answer:

Certainly here is how you could present the information in the requested table format filling in the relevant details for each aspect Account at Risk ...View the full answer

Auditing A Practical Approach

ISBN: 9781119709497

4th Canadian Edition

Authors: Robyn Moroney, Fiona Campbell, Jane Hamilton, Valerie Warren