Brown and Collins, a firm of chartered accountants, is auditing the financial statements of Globe Ltd for

Question:

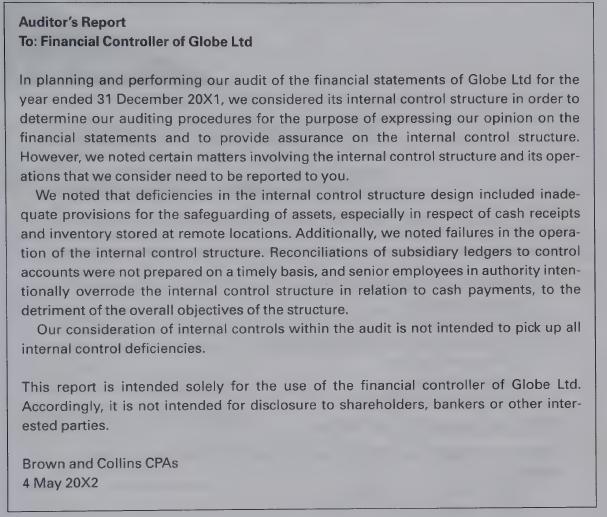

Brown and Collins, a firm of chartered accountants, is auditing the financial statements of Globe Ltd for the year ended 31 December 20X1. Tom Brown, the engagement audit partner, anticipates expressing an unqualified opinion on 20 May 20X2.

Jane Grieves, an audit assistant on the engagement, drafted the auditor’s management letter that Tom Brown plans to send to Globe Ltd along with the 20 May financial statements.

Tom Brown reviewed Jane Grieves’s draft and said there were some deficiencies. The draft was as shown below.

Required

Indicate any deficiencies in the draft management letter prepared by Jane Grieves.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

David Muchemi

I am a professional academic writer with considerable experience in writing business and economic related papers. I have been writing for my clients who reach out to me personally after being recommended to me by satisfied clients.

I have the English language prowess, no grammatical and spelling errors can be found in my work. I double-check for such mistakes before submitting my papers.

I deliver finished work within the stipulated time and without fail. I am a good researcher on any topic especially those perceived to be tough.

I am ready to work on your papers and ensure you receive the highest quality you are looking for. Please hire me to offer my readily available quality service.

Best regards,

27+ Reviews

61+ Question Solved

Related Book For

Question Posted: