Your client is PM Limited (PM), whose main business is maintaining commercial aircraft. PM has contracts with

Question:

Your client is PM Limited (PM), whose main business is maintaining commercial aircraft.

PM has contracts with several major airlines to carry out maintenance exclusively on their planes when they are in the UK.

Stock items range from screws and wire to more expensive items such as panelling and electronic components. Due to the value of some of the larger items, PM keeps stock levels to a minimum.

The majority of stock is held at the company’s warehouse near Heathrow airport.

This is the first year your firm has performed the audit of PM. Your review of the predecessor auditor’s working papers revealed that problems with cut-off were experienced regularly.

No other problems were noted in the working papers.

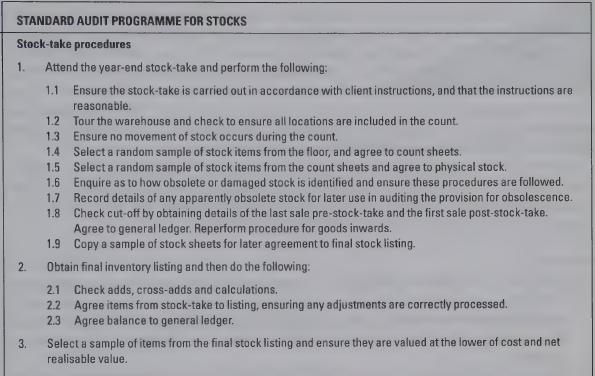

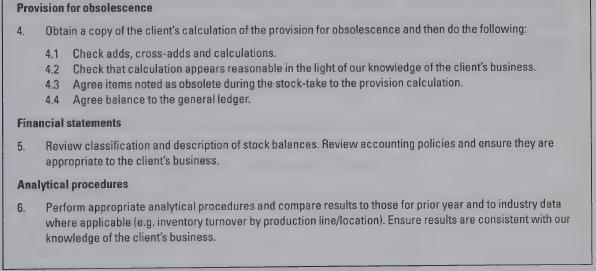

Your firm’s standard audit programme for stock is as described opposite:

Required

(a) For each of the audit steps identified in the audit programme, identify the audit assertion(s) it addresses.

(b) What procedures would you add, amend or delete on your firm’s standard audit programme for this client?

(c) Could analytical review tests replace all of the tests of details of balances and tests of details of transactions for this part of the audit? Why or why not?

Step by Step Answer: